Inflation has been the topic of much debate and concern recently, as the economy continues to rebound from the coronavirus pandemic and the Federal Reserve sets its sights on 2% inflation. But some analysts are worried that inflation rates surging past that target could spell trouble for both bond and equity markets.

Since last summer, the Federal Reserve has been discussing 2% inflation as a target. The central bank’s website even enumerates its rationale, addressing the fact that inflation might be problematic for those with low incomes, but could still be beneficial overall.

“The Federal Open Market Committee (FOMC) judges that inflation of 2 percent over the longer run, as measured by the annual change in the price index for personal consumption expenditures, is most consistent with the Federal Reserve’s mandate for maximum employment and price stability. When households and businesses can reasonably expect inflation to remain low and stable, they are able to make sound decisions regarding saving, borrowing, and investment, which contributes to a well-functioning economy.”

Continually low inflation expectations, however, can drag the actual inflation rate lower and lower.

“For many years, inflation in the United States has run below the Federal Reserve’s 2 percent goal. It is understandable that higher prices for essential items, such as food, gasoline, and shelter, add to the burdens faced by many families, especially those struggling with lost jobs and incomes. At the same time, inflation that is too low can weaken the economy. When inflation runs well below its desired level, households and businesses will come to expect this over time, pushing expectations for inflation in the future below the Federal Reserve’s longer-run inflation goal. This can pull actual inflation even lower, resulting in a cycle of ever-lower inflation and inflation expectations.”

Yet, some experts such as Charles Ellis, author of the legendary investing book “Winning the Loser’s Game,” are concerned that a sudden spike beyond the Federal Reserve’s 2% target could wreak havoc on bond and equity markets.

“The cost of money is so low that after you adjust for inflation, bonds don’t pay anything,” said Ellis, the founder and former managing partner of Greenwich Associates, on CNBC’s “ETF Edge.”

“If bonds are a bad bet because of inflation, the inflation is going to affect equities as well and it will reduce the value of equity securities, no doubt about it,” he added.

According to Ellis, the traditional 60-40 stock-bond tilt has become outdated, with investor individualism dominating portfolios. Ellis advocates a more personalized approach instead.

Each investor has a “different amount of wealth, different amount of income, different amount of savings capacity, different attitude towards risk,” Ellis said.

“When you take all of those different things and a different time horizon, … that’s what should be governing your way of investing,” he noted.

As a result, having a large percentage of bonds, in the 30-40% range of a portfolio, may not be appropriate for everyone.

“There may be somebody in the world for whom that is the correct answer, but they’re not very many and they certainly aren’t everybody,” Ellis cautioned.

Dave Nadig on Today’s Approach to Bonds

With interest rates so low, ETF investors should exercise caution around bond decisions, ETF Trends chief investment officer and director of research Dave Nadig said in the same “ETF Edge” interview.

“Bonds in a portfolio have always behaved differently than an individual bond,” he said. “In a portfolio of constantly rebalancing bonds, that’s a very different pattern of returns.”

Part of the problem may be that bond investors aren’t being paid well enough for the risk they’re actually taking on.

“There are multiple things going on there that just make bonds a very difficult asset class to own right now,” Nadig added. “It doesn’t mean that an individual bond can’t still serve a specific purpose for somebody. I know plenty of advisors who are still building individual bond ladders for certain clients with certain needs. But the blanket idea that as an asset class you can just put money in the AGG and it will do a certain thing for you, I just don’t believe it’s true right now.”

AGG is the iShares Core U.S. Aggregate Bond ETF (AGG), and has fallen about 4% from its all-time high made last August.

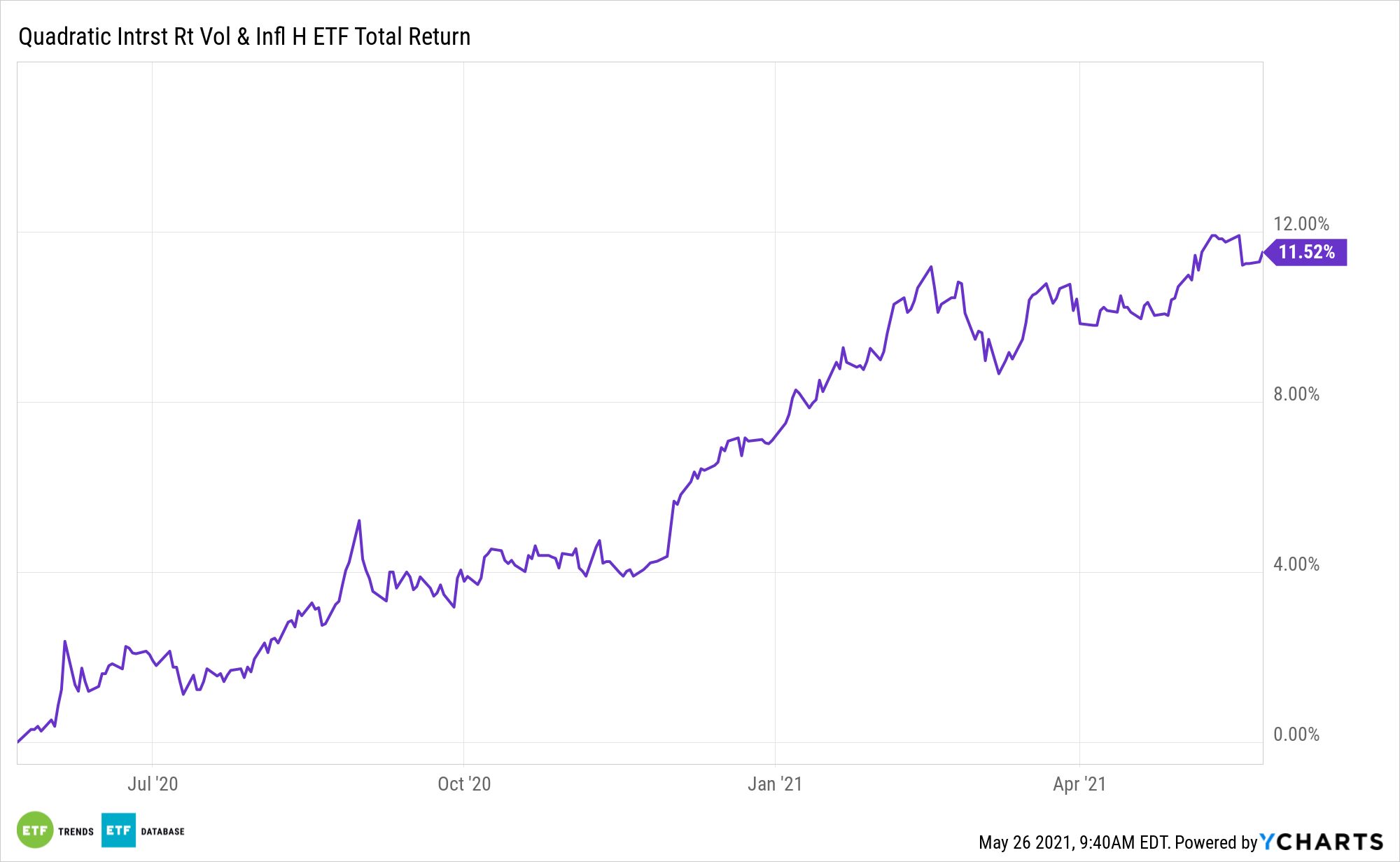

But investors have other options as well. For investors looking for payments from dividends, the KFA Small Cap Quality Dividend Index ETF (KSCD) is one option to consider. Meanwhile, for those looking for a potential hedge against inflation, the Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL) is another possible ETF.

IVOL seeks to hedge the risk of increased fixed income volatility and rising inflation and to profit from rising long-term interest rates or falling short-term interest rates, often referred to as a steepening of the US interest rate curve, while providing inflation-protected income. The fund invests in a mix of TIPS.

For more market trends, visit ETF Trends.