![]() By Rod Smyth, RiverFront Investment Group

By Rod Smyth, RiverFront Investment Group

Non-US stock markets have now outperformed the US for four consecutive quarters. We wrote about this in July, but it is still the case that the following questions dominate those we are being asked:

- Are we due a correction, and if I have cash, should I invest now or wait?

- Is it too late to allocate more money to international?

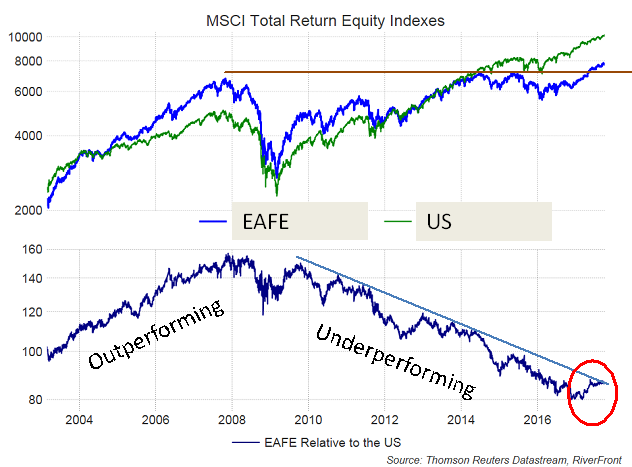

Taking the second question first, let’s look at the relative performance of developed international stock markets to the US. In the top clip of the chart below, we show the performance of the MSCI EAFE (Europe, Australasia and Far East) index (blue line) and the MSCI US index (the green line). You can see that directionally their movements are similar (i.e. closely correlated), but there are times when one does better than the other. In the bottom clip we look at the difference in relative performance. The bottom clip shows that relative performance goes in cycles. EAFE performed materially better than the US in the years leading up to the stock market collapse of 2008. The last seven years have seen the US lead global markets higher, significantly outperforming. It’s worth noting that, over the past half-century, returns between US and non-US stocks have been virtually identical. Past performance is no guarantee of future results.

Past performance is no guarantee of future results. Data from March 2003-October 2017. Total Return includes interest, capital gains, dividends and distributions realized over a given period of time.

We think this chart demonstrates several points:

The red circle in the lower clip shows that the outperformance by EAFE over the last year is modest (historically speaking) so far, and has yet to break above the light blue downtrend line. If

- we are right and international markets are going to outperform the US in the coming years, they have a long way to go to erase some of the underperformance of the last seven years. Thus in our view, as our title says: it’s only early days. For our opinion to be validated, we think the relative performance must break the down-trend line and begin a new up-trend.

- From a technical perspective, we think it is very significant that, when re-invested dividends are included (total return), EAFE has finally broken above its highs from 2007 (its “lost decade”), shown by the brown line in the top clip. Since US stocks broke out from their lost decade, they have continued higher ever since. We think the economic growth cycle in Europe and Japan has many more years to go which we believe will drive earnings and stock prices higher.

- In our opinion, investors who have not diversified their stock portfolios globally are being presented with an attractive opportunity to switch from the US to International. To answer the question of how much international, we think that depends on your holding timeframe and risk tolerance. Our asset allocation portfolios that have a timeframe of five years or more have between 23% and 63% of the portfolio in international stocks. The longer the timeframe and thus the greater tolerance for volatility, the greater the allocation to international stocks, in our view.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities.

After a strong year, are we due a correction? If I have cash, should I invest now or wait?

Oh, if we had a penny for every time this question comes up! Our most consistent answer is that timing is difficult and so we strongly advise investors who want to deploy cash to start the process and add in installments over several months, taking emotion and market timing out of the decision. Today, that is just what we would advise as our timing tools are still projecting above average odds that stocks will be higher over the next three months, despite sentiment in the US being quite stretched to the upside. This is because the primary trend is in a uptrend. New highs on markets are not a danger signal in our view, but rather confirmation of the bull market. A correction is always possible at any time, and an unexpected negative surprise could trigger it, but we believe the odds favor remaining strategically and tactically bullish.

Through September 30th the MSCI World Index is up 17% and 5% for the quarter. The returns have been evenly distributed, with the US a slight laggard and emerging markets doing the best (+28%). While this is above the baseline estimate we made at the beginning of the year, we believe the gains have been justified by earnings growth.

Fear and Greed have always dominated investor emotions, but since the 2008 stock market collapse, fear and caution have been most prevalent in our view. There is an old adage that a bull market climbs a “wall of worry” and this bull market certainly seems to us to be following that pattern. Two things would cause us to be strategically concerned:

- Excess optimism expressed in excessive valuations, which for Riverfront would mean stocks moving significantly above their long-term trends. This is not currently the case for the majority of stock indexes we follow.

- An impending global economic downturn that would cause earnings to fall. We do not foresee this over the next year, rather we believe we will see mildly accelerating economic momentum and no major increase in inflation expectations.

Conclusion: In our asset allocation portfolios, we retain our preference of stocks over bonds. Within our stock allocation we continue to believe global markets have further upside potential, especially those overseas.

Rod Smyth is the Chief Investment Strategist at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information:

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

These materials include general information and have not been tailored for any specific recipient or recipients. Accordingly, these materials are not intended to cause RiverFront Investment Group, LLC or an affiliate to become a fiduciary within the meaning of Section 3(21)(A)(ii) of the Employee Retirement Income Security Act of 1974, as amended or Section 4975(e)(3)(B) of the Internal Revenue Code of 1986, as amended.

Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.