It’s a polycrisis, Charlie Brown! The Ukraine war has entered a new stage, and it looks like it could continue to persist for an alarming amount of time. Coupled with recent protests in China over lockdowns, a pair of thwarted coups, the emergence of new COVID variants, and a brutal flu and cold season, the global health and geopolitical situation is precarious. What impact will all this have on U.S. markets? What steps should investors and advisors take to keep their portfolios safe amid geopolitical chaos and global economic headwinds? We asked our VettaFi Voices to weigh in.

Dave Nadig, financial futurist: This is a multi-polar question, but it’s also a good one because we face a polycrisis. There are a few things I think remain true, no matter what you read in a day-to-day headline.

First, we must acknowledge that the just-in-time global manufacturing system is over. The cracks in that core economic system are manifold. There’s too much manufacturing in a state-led economy (China), too many supply chain and shipping issues, the likely geographic impact of climate change (which is relatively favorable for North America vs. the rest of the world), a battle between central banks trying to control inflation and politicians distributing stimulus — and potentially CapEx spending. All of these are true and real and are what the country is going to deal with for the next decade.

How that manifests? I largely agree with Napier on this. The world re-regionalizes and re-industrializes. The end state ends up looking like 4% long-term inflation in the U.S., with 6% long-term GDP growth. This allows the country to inflate its way out of the debt we’ve accumulated.

This strikes me as the core economic weather for the next while if we assume that geopolitics just takes a middling course — the war drags on into Orwellian East Asia conflict, China slowly reopens but also re-localizes much of its capital flow, etc.

So what does a U.S. investor do about this? The honest truth is that you simply position for that rate/inflation/growth regime. Income, cash flow, and default risk will matter marginally more than they have in the past decade and change. Non-profitable growth in the tech sector becomes harder to support. So what we’ve seen in flows — advisors positioning more defensively in equity, but not out of equity, into true alternatives and being thoughtful about fixed income exposure and inflation plays? That’s the right call.

Todd Rosenbluth, head of research: VettaFi recently asked advisors what their biggest goals over the next six months were, and the majority chose to mitigate their exposure to market volatility and downside risk. Advisors are having more conversations this year about protecting against future losses than normal because both stocks and bonds are both down for the year.

From an ETF perspective, low-volatility ETFs have been popular, gathering more than $10 billion in flows this year after incurring net outflows in 2020 and 2021. ETFs like the Invesco S&P 500 Low Volatility ETF (SPLV) and the iShares MSCI USA Min Vol Factor ETF (USMV) have been the big winners. But demand has accelerated for the defined outcome ETFs that offer downside protection in exchange of an upside cap. ETFs like the Innovator U.S. Equity Buffer ETF – December (BDEC) come to mind. Rather than timing the market, advisors can use these ETFs to keep clients invested for the eventual bullish times without having to sell and hope to get back in later. Time in the market, not timing the market, works best.

Stacey Morris, head of energy research: I think there’s a bull case for energy and midstream in what Dave laid out — not to put words in your mouth, Dave! Energy tends to do well in periods of high inflation, and these companies are generating solid cash flows that return to investors through buybacks and dividends. Energy infrastructure is particularly well positioned for inflation, given that contracts typically include annual inflation adjustments. Of course, midstream/MLPs are providing very attractive income with yields rising, given the recent broad equity weakness. If investors want more defensive energy exposure and income, then energy infrastructure checks those boxes.

Oil prices are likely to remain volatile, but the decline in oil prices hasn’t really detracted from energy stock performance this year. Global oil markets are focused on the timing and magnitude of a rebound in Chinese demand as COVID restrictions ease while also watching Russian oil exports given the embargo and price cap that took effect earlier this week.

Rosenbluth: You can put those words in mine, Stacey, because the current scenario is one well suited for MLP ETFs like the Alerian MLP ETF (AMLP), which has seen net inflows in 2022, while the more sector-diversified Energy Select Sector SPDR ETF (XLE) has seen net outflows. The volatility in oil prices might not have detracted from energy stocks like Exxon (XOM) and Chevron (CVX), but ETF investors have sought something safer.

Morris: True, XLE has seen outflows this year. But if you go back to November 2020, when energy really started to have its run on vaccine news, since then, XLE has had over $6 billion in net inflows.

Another point is that the potential for tax-deferred income typically supports longer holding periods for MLP-focused funds, whereas XLE investors may be more tactical.

Rosenbluth: Fair point. Broadening this back out beyond one sector, risks will remain heading into 2023, even if the Federal Reserve slows its rate hiking program and inflation eases. Advisors will benefit from a defensive posture if they do not feel clients can stomach the volatility.

Nadig: Honestly, I am not sure that trying to be super tactical about integrated oil companies makes sense for most investors. One of the things I feel like investors are just starting to realize is that figuring out how carbon transition impacts traditional players is a lot less obvious than it seems. It seems clear, though, that anything U.S.-based will likely be well positioned.

I also think we don’t really understand — or at least I’ll admit that I don’t — what the impact of forward pricing contracts for refilling the SPR are going to do to markets. It theoretically gives some solace to drillers because they have a price they know they can sell at, but of course, the slow drip of buying is hard to forecast.

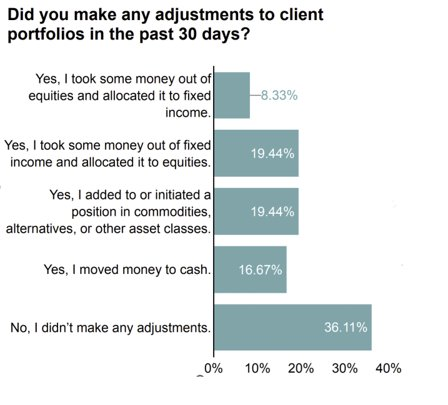

Lara Crigger, editor-in-chief: I want to step back to something that Dave said about ETF flow patterns and how advisors are being more defensive in their equity positioning and being more thoughtful about fixed income.

Over the past few months, we’ve been asking advisors what changes they’re making, if any, to protect their clients against inflation and rising rates. We’ve asked some variation of this question at least four or five times. Consistently, the most popular answers (after “make no changes at all,” which: Gotta respect that long game!) are 1) to move client money into alts, and 2) to move client money out of fixed income and into equity markets. Here’s an example — the numbers change, but the proportions stay roughly the same:

So what this tells me is that most advisors aren’t looking at the current chaos — whether it be the rate/inflation environment in the U.S. or overseas geopolitical kerplosions (that’s my new technical term for it) — and thinking, “Gosh, I need to move my clients out of risk assets pronto.” Instead, as Dave said, they’re being thoughtful about which bond exposures they’re using — and if they can find a better option in equities, then they’ll take it.

While five of the top 10 highest-flows-getting ETFs last month were fixed income ETFs, flows into fixed income ETFs, on the whole, were dwarfed by those into equity ETFs. ($42 billion vs. $23 billion). And the bond ETFs that were popular were the fixed income products that could actually provide income (like the Vanguard Tax-Exempt Bond ETF (VTEB) and the iShares National Muni Bond ETF (MUB) were taking in cash, but so were equity-based income ETFs like the Schwab US Dividend Equity ETF (SCHD) and the JPMorgan Equity Premium Income ETF (JEPI). Honestly, I’m always in favor of a “don’t panic” approach to the markets.

Nadig: Well, they can’t flee the equity markets. Inflation means there’s no hiding. That’s the biggest change, honestly, in the last 20 years. For the first time in ages, the mattress is a guaranteed loser.

Rosenbluth: No need to stick money under the mattress, Dave. Cash-like funds like the JPMorgan Ultra Short Income ETF (JPST) are yielding more than 4% with a duration of three months and investments in high-quality bonds. There’s income to be had with low-risk fixed income ETFs again.

Crigger: Except that folks aren’t taking that option. Apologies to TLC, but investors just aren’t chasing fixed income waterfalls, they’re sticking with the SCHDs and JEPIs that they’re used to. JPST is seeing some flows, yes, but not like those two (JPST is up $339 million over the past 30 days, and JEPI is up $1.5 billion.)

vettafi.com is owned by VettaFi, which also owns the index provider for AMLP. VettaFi is not the sponsor of AMLP, but VettaFi’s affiliate receives an index licensing fee from the ETF sponsor.

Be sure to catch the VettaFi Voices, as well as a host of experts, at Exchange, on February 5–8, 2023, in sunny Miami, Florida. To learn more about the event and register, please visit the Exchange website.

For more news, information, and analysis, visit VettaFi | ETF Trends.