Economic indicators play a pivotal role in understanding the health and performance of the U.S. economy. They are essential tools for policymakers, advisors, investors, and businesses. This is because they enable them to make informed decisions and significantly influence business strategies and financial markets. In the week ending October 26, the SPDR S&P 500 ETF Trust (SPY) fell 3.25%, while the Invesco S&P 500 Equal Weight ETF (RSP) was down 2.54%. In this article, we look at three economic releases from the past week: personal consumption expenditures (PCE), gross domestic product (GDP), and consumer sentiment.

These interconnected indicators provide insight into the nation’s economic climate, with a particular focus on consumption and consumer sentiment. By understanding consumers’ attitudes regarding the economy, we can gauge consumer spending patterns. That is a major driver of overall economic growth.

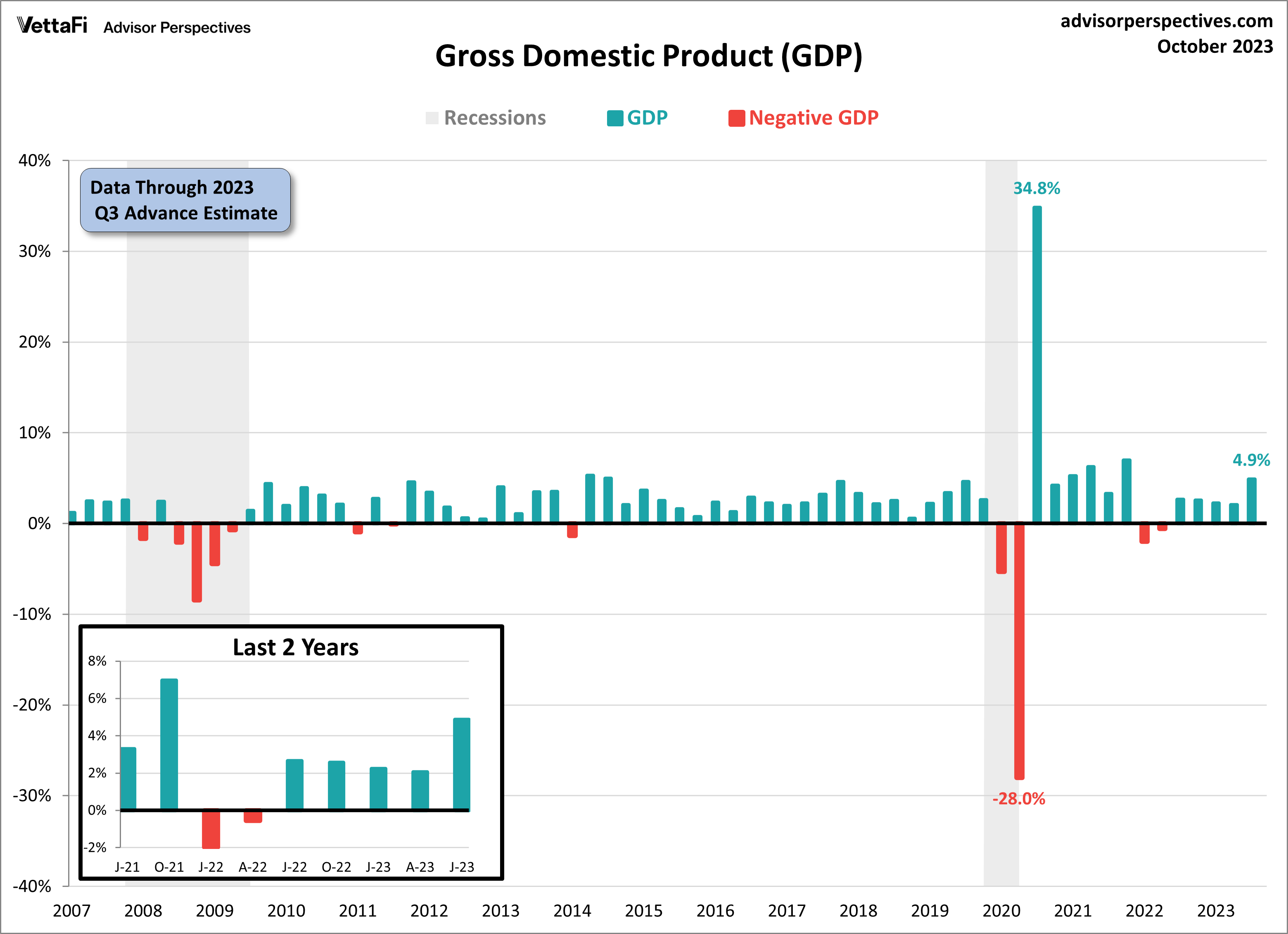

Gross Domestic Product (GDP)

The U.S. economy grew at its fastest pace in almost two years, according to the advance estimate for Q3 2023 GDP. The economy expanded at an annual rate of 4.9%. That was more than double the 2.1% from the second quarter. It was also faster than the expected 4.3% pace. The latest figure marks the fifth consecutive quarter of growth. This is defying the numerous predictions made over the past year of an impending economic slowdown and possible recession.

The resilience of the job market has created a resilient consumer base. This, in turn, has become a catalyst for economic growth. In the third quarter, consumer spending emerged as the largest contributor to real GDP growth out of the four subcomponents. Additionally, business investments and government spending made notable contributions to the third-quarter growth. But these gains were partially offset by an increase in imports.

Despite the impressive growth in Q3, consumers will continue to face various challenges. These include high interest rates, the resumption of student loan payments, dwindling savings, and a mounting sense of uncertainty. While consumers have defied expectations all year, the growing list of challenges raises the question about whether they can maintain the same level of resilience they’ve shown thus far.

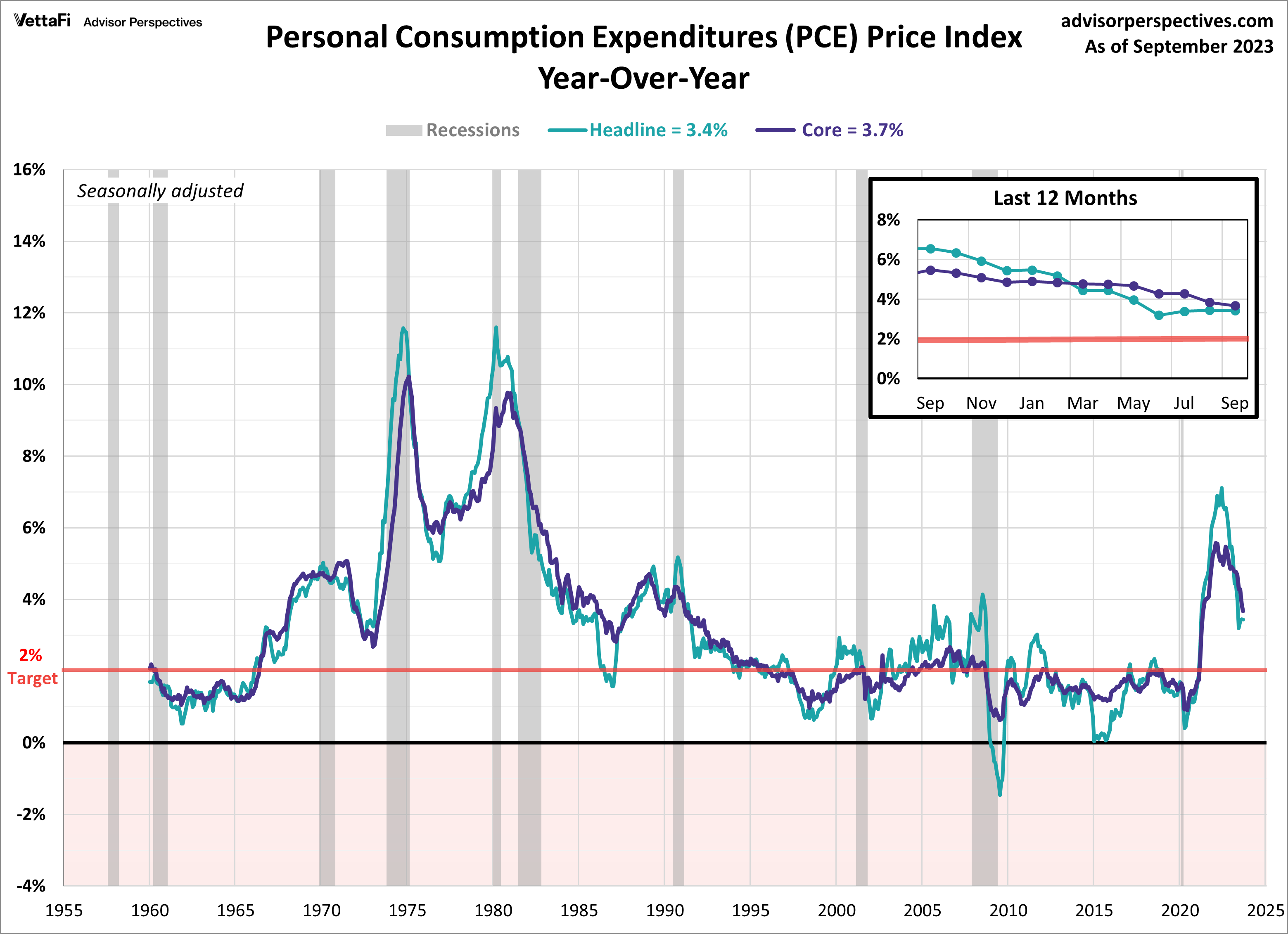

Personal Consumption Expenditures (PCE)

In September, the Fed’s preferred inflation gauge continued to show signs of cooling, as expected. The Core PCE Price Index, which measures inflation excluding volatile food and energy prices, rose by 3.7% compared to the previous year, a slowdown from the 3.8% recorded in August. Core PCE inflation is now at its lowest level in over two years but remains above the Fed’s 2% target rate. While the core measure shifted down this month, headline PCE remained stable, at 3.4% in September. Both annual readings were consistent with their respective forecasts.

On a monthly basis, the core PCE rose 0.3% from August, as expected, representing its largest monthly increase since May. Additionally, headline PCE exceeded expectations, with a 0.4% monthly increase, compared to the 0.3% expected growth.

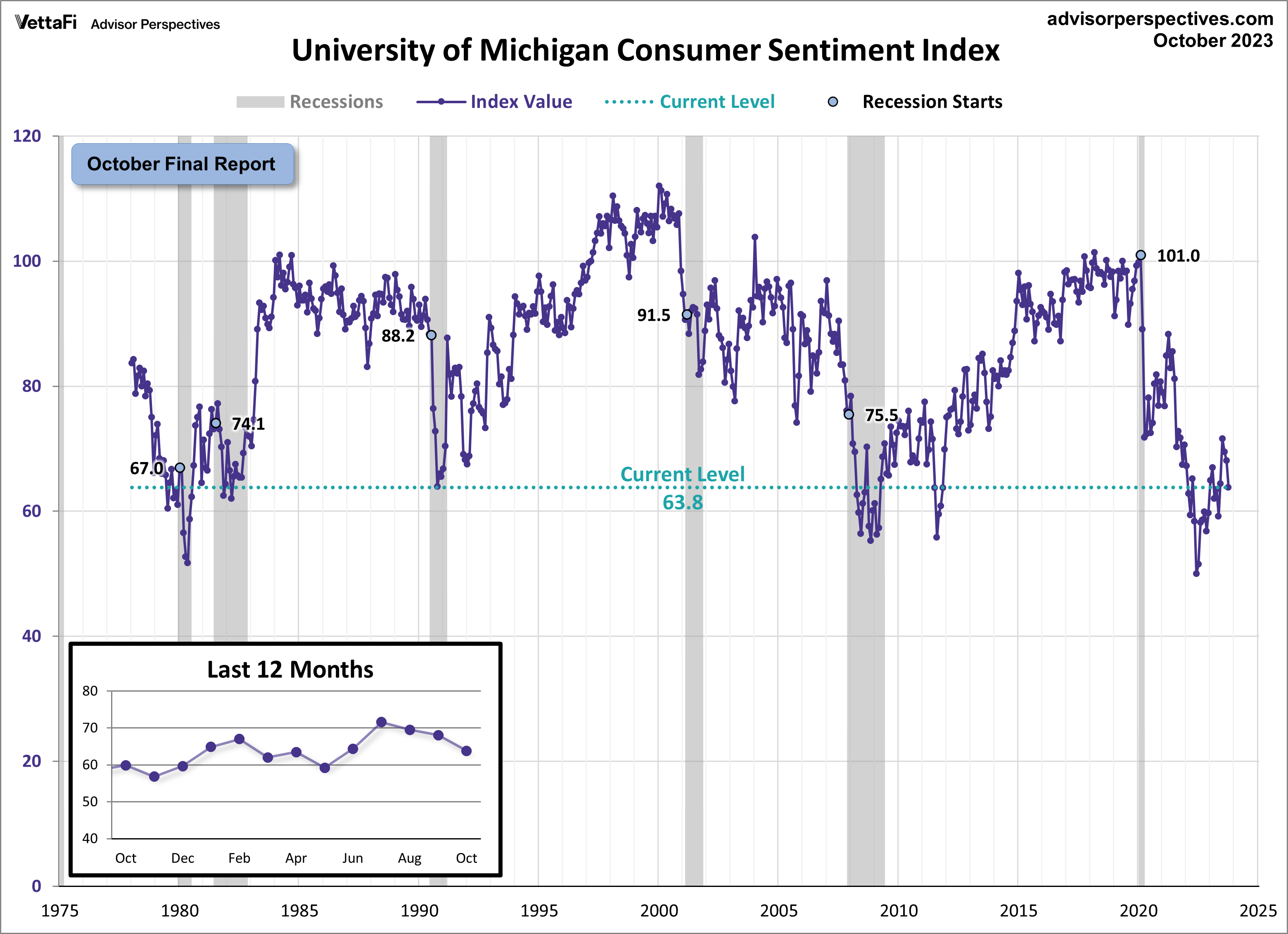

Consumer Sentiment

Consumer sentiment diminished further this month, with higher-income consumers beginning to feel the impact of weakening equity markets. According to the final October report of the Michigan Consumer Sentiment Survey, the index fell for a third consecutive month to 63.8. This represents a 6.3% decrease from September’s final reading and is just above the forecasted value of 63.0. To put the latest figure into a historical context, the current index level is at the 7th percentile of the series, underscoring the persistently subdued sentiment consumers have experienced since the start of the pandemic.

The Michigan Consumer Sentiment Index is a monthly survey measuring consumers’ opinions regarding the economy, personal finances, business conditions, and buying conditions. In the latest report, business conditions and personal finance expectations both fell significantly from September. Additionally, inflation continues to be a top concern for consumers as inflation expectations for both the short term and long term increased.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

Economic Indicators and the Week Ahead

The focus for this week shifts to the labor market as several key job reports will be released. The September JOLTS data and October employment reports will provide insights into the health of the labor market, a vital facet of the overall economy. Last month’s reports signaled a strong and resilient labor market. If the trend continues, the Fed will likely double down on its “higher for longer” stance to help combat their fight against inflation.

On Wednesday, we will learn if job openings continued to rise for a second straight month in September or if the trend resumed its downward path. Also on Wednesday, the ADP employment report will be released, which will set the stage for the more comprehensive BLS employment report released on Friday. Expectations are that 172,000 nonfarm jobs were added in October, down from 336,000 in September, and that the unemployment rate remained at 3.8%.

For more news, information, and analysis, visit the Innovative ETFs Channel.