Economic indicators provide insight into the overall health and performance of an economy. They are essential tools for policymakers, advisors, investors, and businesses. That’s because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending March 14, the SPDR S&P 500 ETF Trust (SPY) rose 0.03%, while the Invesco S&P 500 Equal Weight ETF (RSP) was down 0.58%.

Inflation has been an ongoing topic of conversation for the past few years. That’s because of its role in the Fed’s interest rate policy. It has been cautious about making any changes to monetary policy, emphasizing the need for inflation to continue to move toward its 2% target. The next Fed meeting is scheduled for this Tuesday and Wednesday, where we can expect to see interest rates remain between 5.25% and 5.50%. This article will summarize three important economic indicators from the past week to provide insight into the latest trends in inflation, consumers’ response to it, and its potential implications.

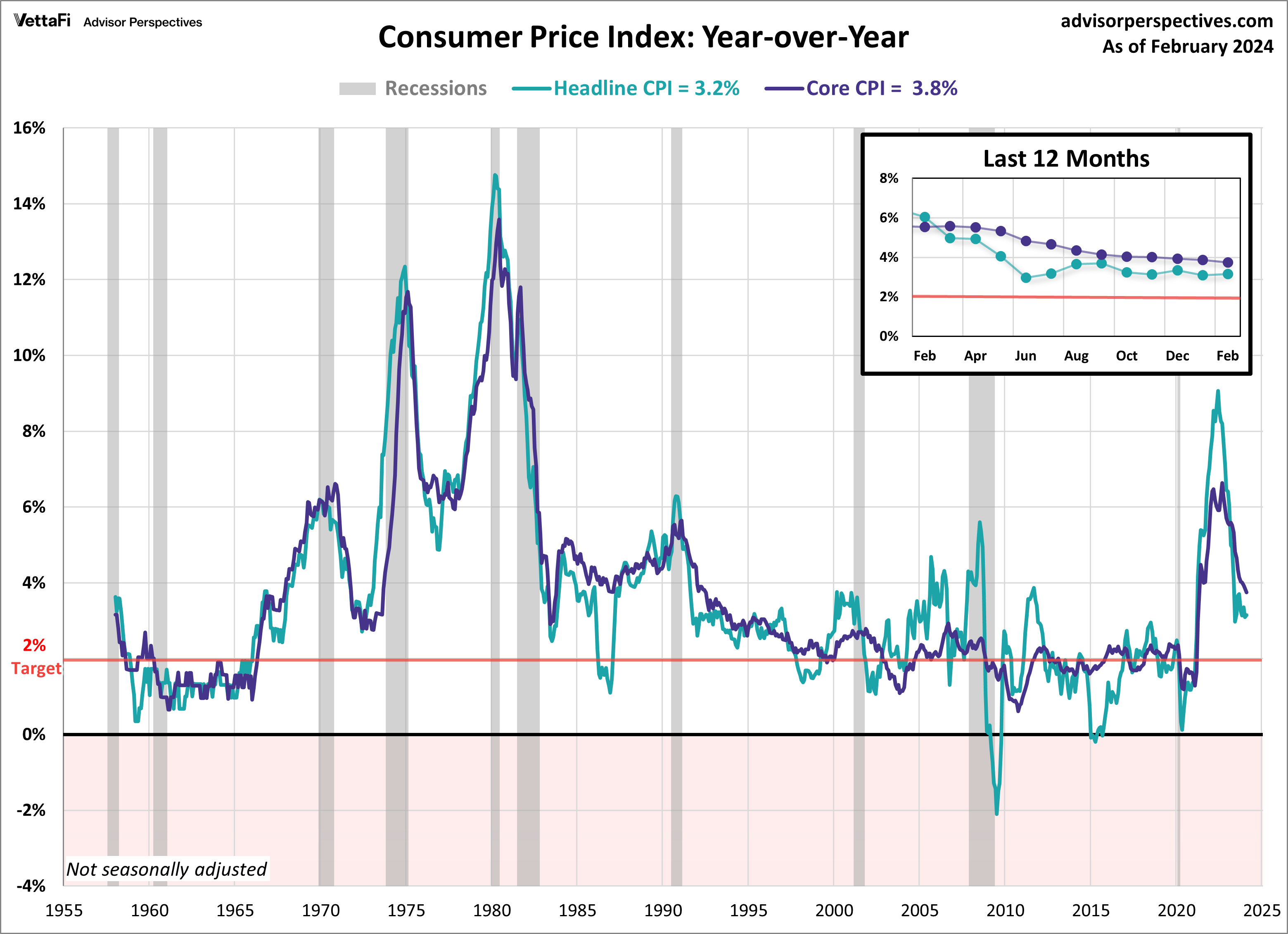

Economic Indicators: Consumer Price Index

Consumer prices rose more than expected last month as inflation continues to prove its stickiness. The Consumer Price Index (CPI) rose 3.2% in February. That’s up from 3.1% in January and more than the expected 3.1% growth. Compared to the previous month, consumer prices rose 0.4%, as expected. The primary driver for the monthly increase was the continued rise in shelter costs as well as an increase in gasoline. When combined, these two aspects contributed to over 60% of the headline increase.

Core inflation, which excludes food and energy prices, slowed to its lowest level since April 2021. Core CPI fell to 3.8% on an annual basis, just above the expected 3.7% growth. Additionally, core prices increased 0.4% from January, more than the anticipated 0.3% growth.

The question remains as to when the Fed will begin to cut rates. The latest CPI numbers give cause for the Fed to hold rates steady over their next few meetings. At the time of writing, the CME Fed Watch Tool indicates a 99% likelihood for rate stability at the March meeting and a 90% probability for the May meeting. The CME Fed Watch Tool is currently showing a 55% probability that the first rate cut will take place in June.

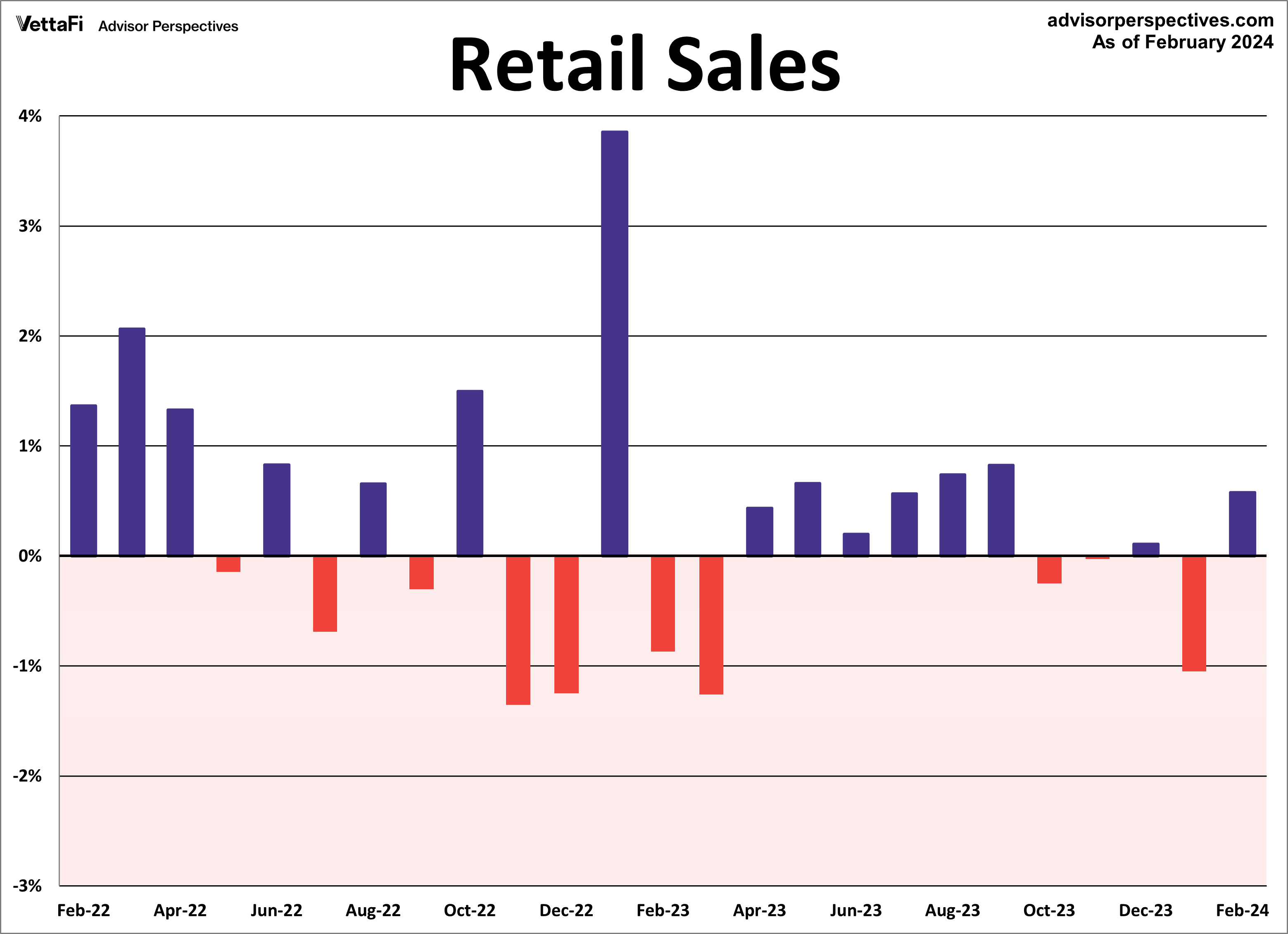

Economic Indicators: Retail Sales

American consumers picked up their spending last month. However, many consumers are growing cautious. Retail sales rebounded 0.6% in February, lower than the anticipated 0.8% growth. Additionally, January’s decline was even larger than initially reported. The latest uptick in spending was seen across most categories. Home improvement stores (2.2%), car sales (1.8%), electronics and appliances (1.5%), and gasoline (0.9%) led the way.

Core retail sales (excluding automobiles) were up 0.3% from January, falling short of the expected 0.5% growth. Lastly, control purchases, which is thought to be an even more “core” view of retail sales, were unchanged from last month. This series typically does not garner as much attention as the headline and core figures. But control purchases are a more consistent and reliable reading of the economy, because that strips out many volatile components.

Overall, consumer spending is off to a slower than expected start for 2024, but still shows signs of resilience. The latest retail sales data is unlikely to cause the Fed to rush to cut rates.

Retail sales will have an impact on the interest in the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

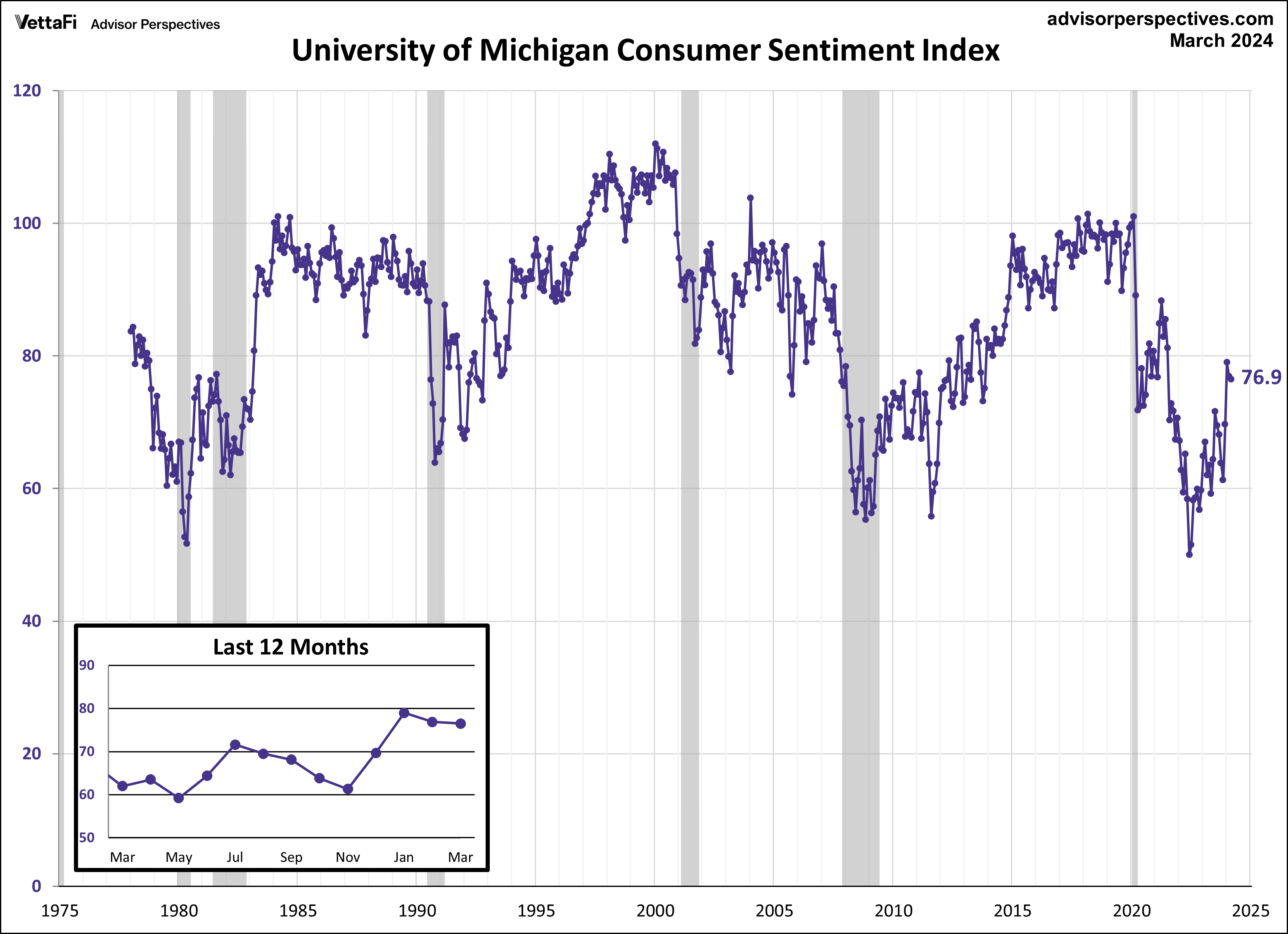

Economic Indicators: Michigan Consumer Sentiment

Consumer attitudes were little changed, according to the preliminary report for the Michigan Consumer Sentiment Index. The March preliminary report came in at 76.5, marking a 0.5% decrease from February’s final reading and just below the forecasted value of 77.1. Sentiment now sits halfway between the historic low reach in 2022 and pre-pandemic levels.

The Michigan Consumer Sentiment Index is a monthly survey measuring consumers’ opinions with regard to the economy, personal finances, business conditions, and buying conditions. In the latest report, consumers expressed increased confidence levels in personal finances, however, decreased levels in expectations for business conditions. More notably, the November presidential election seems to be a significant factor in consumers’ attitudes and future perceptions for the economy’s trajectory.

Consumer attitudes are closely monitored, as their confidence levels tend to impact their spending behavior. Given that consumer spending accounts for approximately 70% of the economy, consumer spending has a major impact on economic growth.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

The Week Ahead

The housing market will be in focus this week as we await the latest data on several key housing indicators. Over the course of the week, we will receive the latest news on builder confidence in home sales, building permits, housing starts, and existing home sales. These housing market indicators will have an impact on homebuilders and residential real estate ETFs such as the iShares U.S. Home Construction ETF (ITB), SPDR S&P Homebuilders ETF (XHB), and iShares Residential and Multisector Real Estate ETF (REZ).

The National Association of Home Builders housing market index will shed light on builders’ confidence levels regarding home sales, which has risen each of the past three months because of moderating mortgage rates, possible Fed rate cuts, and a lack of existing inventory. Building permits are forecast to increase from last month, while housing starts are expected to rebound from January. Finally, existing home sales are projected to continue their downward trend by dropping to a seasonally adjusted annual rate of 3.94 million units.

For more news, information, and strategy, visit the Innovative ETFs Channel.