Policymakers, advisors, and analysts closely monitor economic indicators because they provide information on the health and performance of the U.S. economy. This information enables them to make informed decisions regarding business strategies and financial markets. In the week ending February 29, the SPDR S&P 500 ETF Trust (SPY) rose 0.11%, while the Invesco S&P 500 Equal Weight ETF (RSP) was up 0.76%.

This article takes a deeper look at three important economic releases from the past week: personal consumption expenditures (PCE), gross domestic product (GDP), and consumer confidence. These interconnected indicators provide insights into the country’s economic landscape, with a particular focus on consumption and consumer attitudes. Understanding consumers’ perceptions of the economy enables us to assess consumer spending patterns, a significant driver of overall economic growth.

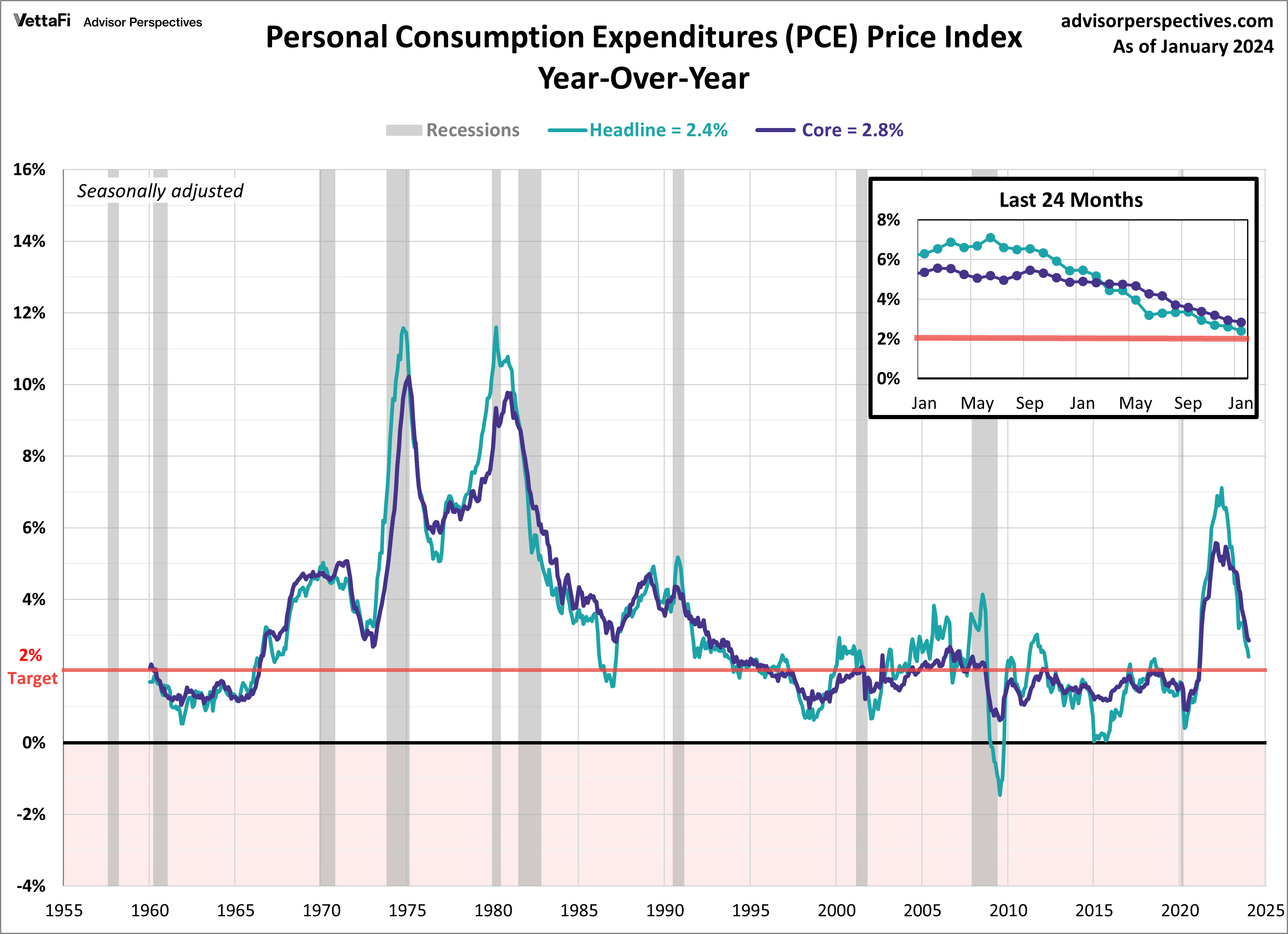

Economic Indicators: Personal Consumption Expenditures (PCE)

The Fed’s preferred inflation gauge cooled further in January, albeit at a sluggish rate. The Core PCE Price Index, which measures inflation excluding volatile food and energy prices, rose by 2.8% compared to the previous year, a slowdown from the 2.9% recorded in December. Core PCE inflation has now slowed for the past 12 straight months and currently sits at its lowest level since March 2021.

With that said, it remains above the Fed’s 2% target rate. Additionally, headline PCE shifted down from 2.6% in December to 2.4% in January, its lowest level since February 2021. On a monthly basis, the core PCE rose 0.4% from December, marking its largest monthly increase in a year. Meanwhile, headline PCE rose 0.3% compared to the previous month. All readings were consistent with their respective forecasts. Overall, the latest PCE numbers were unsurprising. The Fed will have to remain patient with its first rate cut, as inflation continues to slowly trend downward.

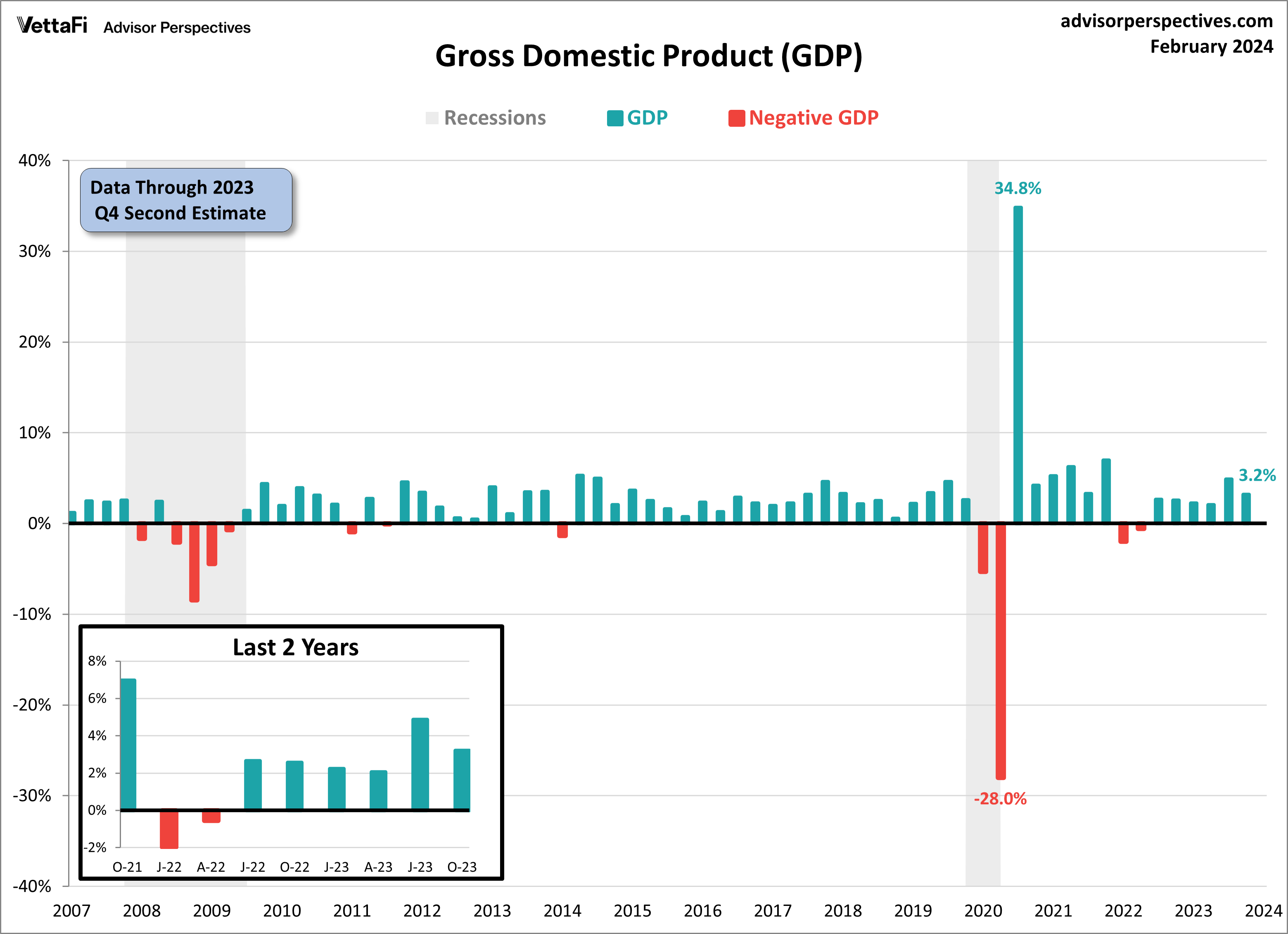

Economic Indicators: Gross Domestic Product (GDP)

In the fourth quarter of 2023, the U.S. economy grew at a slower pace than initially thought, highlighting the economy’s resilience through various challenges. The second estimate for Q4 2023 Gross Domestic Product (GDP) revealed that the economy expanded at an annual rate of 3.2%, a slight adjustment from the initial estimate of 3.3% growth reported last month, and significantly slower than the Q3 final estimate of 4.9%. The latest figure marks the sixth consecutive quarter of growth, defying the numerous predictions made over the past year and a half of an impending economic slowdown and possible recession.

All four subcomponents made positive contributions last quarter to real GDP, but consumer spending remains the catalyst behind last quarter’s economic growth, emerging as the largest contributor. However, business investment and net exports experienced downward revisions from last month, which ultimately led to the overall downward revision in GDP growth this month.

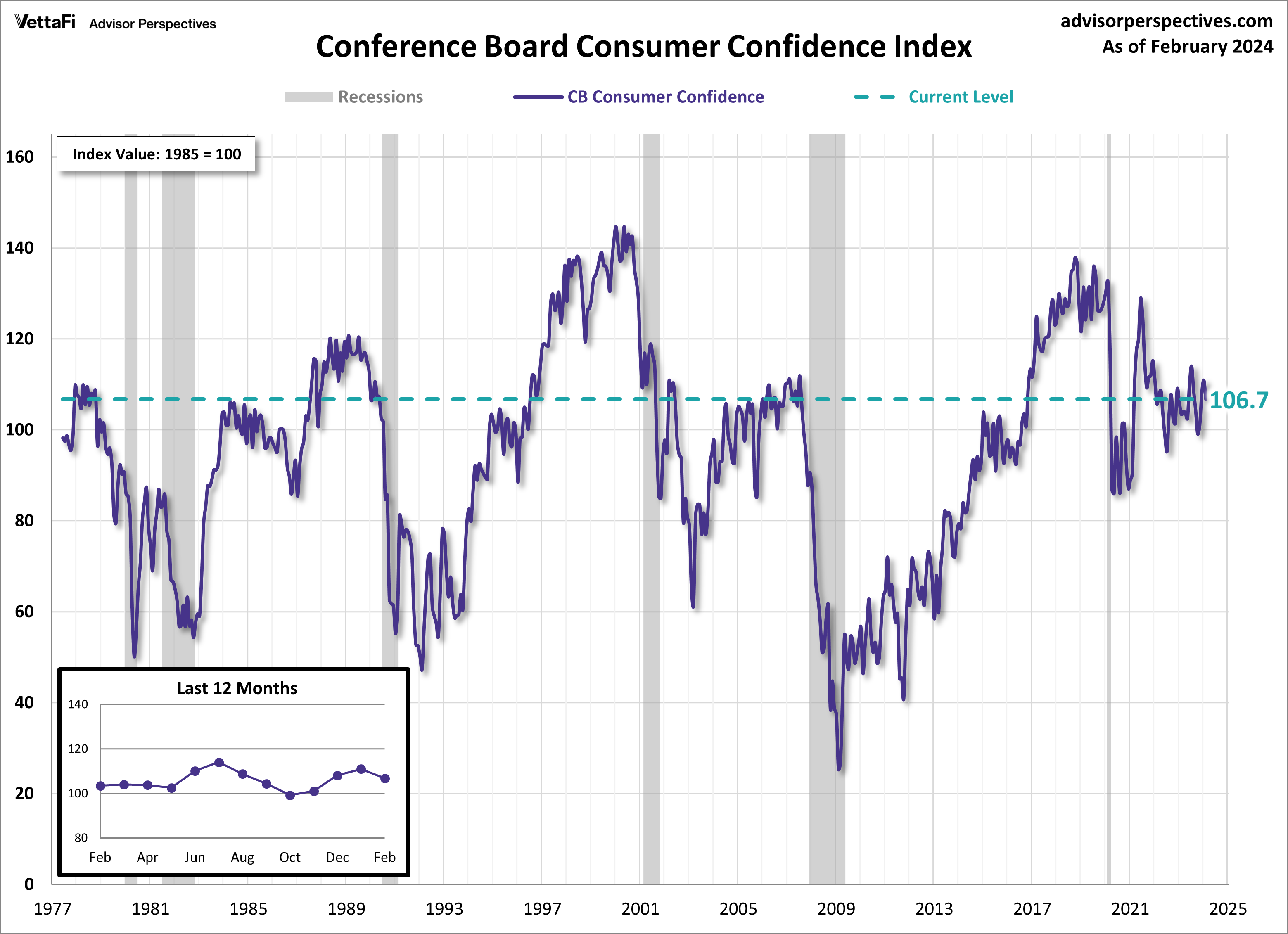

Economic Indicators: Consumer Confidence

American consumer confidence retreated in February following three straight months of improvement. Last month, the Conference Board Consumer Confidence Index dropped to 106.7 from a downwardly revised 110.9 in January. The latest reading came as a surprise, as the forecast projected the index to come in at 114.8. Consumers reported the labor market situation and the U.S. political environment as their top concerns. Additionally, consumers are still expressing concerns regarding inflation, while also acknowledging it has eased recently. Consumer attitudes are closely monitored, as their confidence levels tend to impact their spending behavior. Given that consumer spending accounts for approximately 70% of the economy, consumer spending has a major impact on economic growth.

The index is based on a monthly survey measuring consumer attitudes about current and future economic conditions, with a particular focus on employment and labor market conditions. The overall deterioration this month is reflected by a drop in both the present situation and expectations index. Consumers’ views on business conditions, the employment situation, and their personal finances all weakened in February. Additionally, consumers expressed increased pessimism about future business and labor market conditions. Moreover, the expectations index dipped below the level that is historically associated with signaling a recession within the next year.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

The Week Ahead

This week, attention will shift to the labor market, as several key job reports will be released. The January JOLTS data and February employment reports will provide insights into the health of the labor market. That’s a crucial component of the overall economy. The last few reports have showed a much hotter than expected labor market. That’s because both job growth and job openings have been on the rise.

On Wednesday, we’ll learn if job openings continued to increase for a third straight month or if the trend resumed its downward path. Also on Wednesday, the ADP employment report will be released. That will set the stage for the more comprehensive BLS employment report released on Friday. Expectations are that 188,000 nonfarm jobs were added in February, down from 353,000 in January, and that the unemployment rate remained at 3.7%.

For more news, information, and strategy, visit the Innovative ETFs Channel.