By Eric Snyder, Director, Product Management for New York Life Investments

We’ve seen a remarkable u-turn in interest rate expectations over the past 12 months. In November 2018, the yield on the 10-year U.S. Treasury note was as high as 3.24% and by Labor Day 2019 it had dropped all the way to 1.47%. Investment-grade municipal bond yields tracked a similar decline, peaking at 3.08% last November 1 and declining to 1.65% over nearly the same period.

The intensifying U.S/China trade war, slowing economic growth, and even this summer’s 2-year/10-year Treasury yield curve inversion has sparked fears that a recession could be looming. Now some market experts are predicting that long-term rates in the U.S. will continue to decline, potentially even to zero. Here’s the catch: none of the top prognosticators have been consistently correct in predicting the direction of rates or where the fixed income market is headed. What might happen to municipal bonds if they are wrong?

This question may be causing some investors to second-guess entering the municipal market. It can be easy for investors to stray from long-term goals by attempting to time market fluctuations with short-term investment decisions. We don’t view an allocation to municipal bonds as a tactical trade, but rather as a dedicated part of a complete asset allocation meant to be held for the long-term, regardless of interest rate movements. Let’s consider the key reasons why.

Munis Are Not Highly Correlated To Rates

Price movements in the municipal bond market do not move in lockstep with U.S. Treasuries.

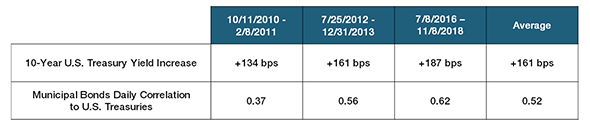

Over the trailing 10-year period from 8/31/2009 to 8/31/2019, there were three periods where the 10-year U.S. Treasury rose by 100 bps or more. As noted in the chart below (Figure 1), investment-grade municipal bond returns during these periods were only moderately correlated to U.S. Treasury rate increases.

Figure 1: Bloomberg Barclays Municipal Bond Index correlations to the Bloomberg Barclays U.S. Treasury Index during rising rate periods of 100 bps or more 8/31/2009 – 8/31/2019

Bloomberg Barclays Municipal Bond Index correlations to the Bloomberg Barclays U.S. Treasury Index during rising rate periods of 100 bps or more 8/31/2009-8/31/2019. Source: Morningstar, FRED, as of 8/31/2019.

The modest correlation between municipal bond prices and U.S. Treasury yields signals that regardless of the interest rate environment, investors receive diversification benefits from holding municipal bonds over time.

Holding Period Matters

The lower correlation between these asset classes also underscores the importance of investors not getting caught up in trying to time the muni market. Attempting to tactically buy or sell municipal bonds doesn’t necessarily protect investors from losses and could potentially limit total returns over time.

To confirm this, we looked at rolling municipal index returns over the same 10-year period, measuring the returns for Investment Grade, High Yield, Taxable, Short-Term, and Insured municipal bonds (Figure 2).

Figure 2: Rolling municipal index total returns 8/31/2009 – 8/31/2019

Source: Morningstar. Measures the performance of the Bloomberg Barclays Municipal Index (Investment Grade), Bloomberg Barclays High Yield Municipal Index (High Yield), Bloomberg Barclays Taxable Municipal Index (Taxable), Bloomberg Barclays Municipal Bond 3-Year (2-4) Index (Short-Term), and Bloomberg Barclays Insured Municipal Index (Insured) during all rolling periods from 8/31/2009 – 8/31/2019. Returns longer than 12-months are annualized. Past performance is no guarantee of future results, which will vary. It is not possible to invest directly in an index.

What we found is that when municipal bonds were held for 24 months or more, none of the major indices produced a negative return over any single rolling period. In fact, holding period mattered, as indicated by the worst-case returns column in figure 2. Total return potential increased incrementally with each step up in holding time. These results are evidence of the benefits of holding municipal bonds for the long-term and demonstrate how attempting to time a tactical allocation in this asset class can lead to poorer outcomes for investors.

Heightened Demand Supports Municipals

It is clear that investors are continuing to see value in municipal bond funds. The demand is, in part, being driven by the fact that for investors seeking tax-exempt income, municipal bonds are the only game in town. Underscoring this is the reality that efforts by lawmakers to remove the State and Local Tax (SALT) income tax deduction cap of $10,000–set into law as part of the 2017 Tax Cuts and Jobs Act–are not expected to advance anytime soon.2 In August alone, the asset class saw $9.1 billion in positive flows, continuing a steady 2019 trend.3

Active Management Matters

Regardless of the interest rate environment, municipal bonds should continue to be an important part of a diversified, long-term asset allocation. Our perspective remains that a strategic allocation to municipal bonds can also be enhanced via the benefits of active management. As uncertainty in the fixed income markets persists, active managers that are able to take advantage of price weaknesses and market dislocations are well-positioned to add significant outperformance over passive approaches.

1. Source: U.S. Department of the Treasury as of 9/12/2019. Investment-grade municipal bonds represented by the Bloomberg Barclays Municipal Bond Index.

2. “State and Local Tax Deduction Caps May Get Another Look,” Forbes, September 11, 2019.