On June 3rd, President Biden signed the Fiscal Responsibility Act of 2023 into law suspending the debt ceiling until 2025 and averting a potential U.S. default. One provision of the law will require student loan repayments to resume for millions of Americans at the end of August[1], reducing discretionary income that can be spent in other parts of the economy. While it’s easy to find data on loan balances, it’s not as straightforward to determine how much money is spent to pay back student loans on an annual basis[2]. Thankfully, the Federal Reserve Board conducts the Survey of Consumer Finances (SCF) every three years asking detailed questions about the finances of U.S. households, including a variety of questions on educational loans[3].

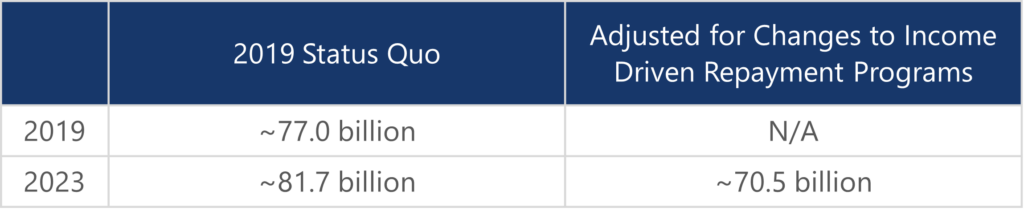

The SCF survey responses indicate that consumers paid roughly $77 billion towards their student loans in 2019. This lines up with reporting[4] that $70.3 billion was paid towards Federal student loans, which make up about 92% of total student loan debt, in that same year. If we assume that growth in loan payments matches growth in loans[5], then we would expect outlays of nearly $82 billion in the twelve months following the resumption of payments.

Estimated Annual Student Loan Payments

Source: Federal Reserve Board Survey of Consumer Finances (SCF), Beaumont Capital Management.

Further complicating the analysis, in addition to the proposed debt cancellation, the Department of Education proposed material changes to their income driven repayment programs[6]. Most notably, those enrolled in income driven repayment programs will now have their maximum payments capped at 5% of discretionary income. Additionally, the threshold for non-discretionary income will be raised as well to 225% of the Federal poverty line. Taking these changes into account, I estimate that student loan payments will be closer to $71 billion, over $10 billion less than payments would have been under the status quo.

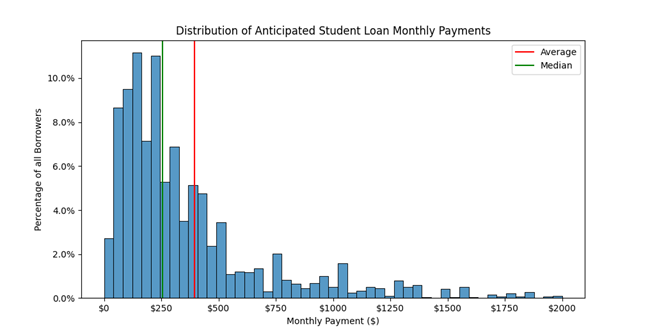

Source: Federal Reserve Board Survey of Consumer Finances (SCF), Beaumont Capital Management. The chart shows the distribution of anticipated monthly payments for all borrowers who will have a nonzero monthly payment under the new income driven repayment programs. The x-axis has been truncated at a $2,000 monthly payment for clarity.

The major impact of the revised income driven repayment programs is that it may double the number of borrowers who don’t pay anything towards their student loans. In 2019, ~12% of borrowers, excluding those in a grace period or forbearance, did not pay anything towards their student loans and once payments restart, we estimate just over 20% of borrowers will not have to make any payments. For those who do have to make payments, an estimated 22 million American households, we estimate a median payment of ~$250 a month and an average payment of ~$390 a month. This would put the annual student loan payments among the top five expenditures for an average household.

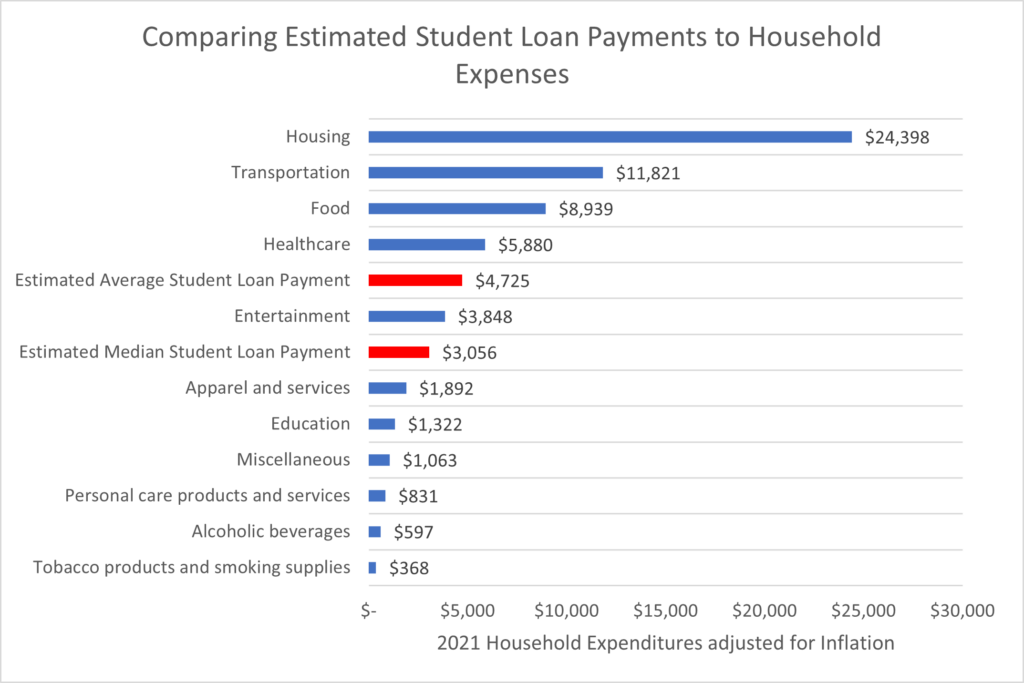

Source: Federal Reserve Board Survey of Consumer Finances (SCF), U.S. Bureau of Labor Statistics (BLS), Beaumont Capital Management. 2021 expenditures were adjusted for inflation using the change in the Consumer Price Index (CPI) between December 2021 and April 2023.

Many of the households that restart student loan payments will clearly face a tradeoff between loan payments and consumption. In the twelve months ending in April 2023, U.S. Consumers spent nearly $18 trillion on personal consumption expenditures[7]. Of course, consumption spending will not decline by the full amount of resumed student loan payments, but if it declined by half of the estimated loan payment amount, then we could see a decrease of ~0.20% in consumer spending equivalent to ~0.13% of Gross Domestic Product (GDP). Such declines may seem inconsequential, but it’s worth noting that spending has rarely fallen on a year-over-year basis outside of a recession. While we don’t believe the resumption of student loan payments will be a large blow to the economy, it seems clear that it will cause spending to decrease and growth to slow down in the short-term.

[1] This timeline is in sync with the President’s previously announced plan to resume payments but prevents the President from issuing any further extensions. Notably, the Fiscal Responsibility Act does not impact the President’s plan to cancel up to $10,000 of student loans for those making up to $125,000, but the legal justification for this executive order is heavily debated and the Supreme Court is expected to rule against it later this month.

[2] The myriad of repayment programs along with limited transparency on cohort level data make it difficult to derive simple estimates.

[3] One caveat is that the survey doesn’t deal with individual consumers but instead deals with an economic unit more akin to a household. This should not impact our analysis materially.

[4] https://slate.com/business/2021/03/student-loan-total-annual-government-payments.html

[5] https://fred.stlouisfed.org/series/SLOAS

[6] https://www.ed.gov/news/press-releases/new-proposed-regulations-would-transform-income-driven-repayment-cutting-undergraduate-loan-payments-half-and-preventing-unpaid-interest-accumulation

[7] https://fred.stlouisfed.org/series/PCE

For more news, information, and analysis, visit the ETF Strategist Channel.

Copyright © 2023 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.