The stock market is not the economy. This is an extremely important concept for investors to keep in mind amidst the constant media drum beat of inflation, rising interest rates, and recession. What gets lost in this cacophony of information overload is the fact that the stock market is a leading economic indicator that is attempting to reflect expected future economic conditions.

Those expectations of future conditions are simply forecasts and reality may turn out to be better or worse than current the markets reflect. The same way that current market conditions reflect future economic challenges, it is important to also note that they also reflect future economic improvement. In many cases, by the time some economic destination or condition is reached, the equity and bond markets have already moved beyond it by having long reflected that eventuality. When the equity market eventually begins a sustained rally, some investors may find themselves surprised that the markets will be reflecting some future recovery phase.

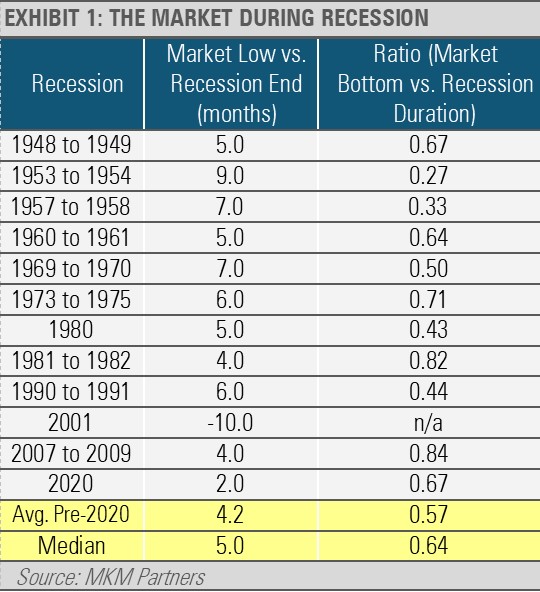

Our base-case scenario calls for a recession in the U.S. in the months ahead. However, it is important to note that the equity market tends to bottom and begin to move higher well ahead of a return to economic growth. For example, of the 12 U.S. recessions since World War II, the longest was the Great Recession from 2008-2009, which lasted 18 months. The shortest recession occurred during the COVID pandemic in March and April of 2020 and lasted two months. Post WWII recessions have lasted 10 months on average.

While the duration and magnitude vary, most recessions have one thing in common. In all post-WWII recessions, except for the Tech Bubble related recession in 2001, the equity market found its bottom and began to rally prior to the end of the recession and beginning of a new business cycle. Although there is a fair amount of variability, the market usually bottoms just over halfway through a recession.

In short, equity market recoveries typically begin months before investors feel better about the economy. In addition, although the magnitude of market declines varies across recessions, they average about a 30% drop from previous highs. Using business cycles and market history as a guide, this leads us to think that most, though perhaps not all, of the risk to the U.S. equity market is already priced in. However, we may be in for a sustained period of volatility with both occasional strong rallies as well as declines.

Therefore, we think that it is important to have an economic and market view that is based on data processed through a time-tested investment discipline. Unbiased discipline can help provide clarity and enable investors to make unemotional decisions in a chaotic and noisy world.

We look at incoming data through the prism of our Three Layers of Risk Management. These layers include our strategic three- to five-year outlook, our tactical six- to eighteen-month view, and the Cash Indicator. Today, we are seeing compelling opportunities both strategically and tactically to protect assets and potentially benefit from this challenging investment environment.

By following a defined process for navigating a risky world, we think investors can feel more confident that they can ride through the turbulence to arrive at their desired financial destination. Recessions and bear markets are part of economic and market cycles, and they do not last forever. Investors can use these turbulent times to find new opportunities so long as they follow a disciplined process. Remember that nothing good comes from panic, and our Three Layers of Risk Management can help manage risks in real time.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.