WHAT CEOS SAY MAY BE MORE IMPORTANT THAN THE NUMBERS

By Riverfront Investment Group

Winston Churchill once said, “Words are the only things that last forever.” In this COVID-19 era of video conferencing and increased written communication, choosing one’s words carefully in order to convey the intended tone, as well as well as to inform, is paramount. As earnings reports from the first quarter unfold, we believe words will matter more than ever for corporate leaders. Recently, the Securities and Exchange Commission (SEC) emphasized the importance for companies to discuss current operations and financial conditions rather than looking backwards, noting that transparency will be important in order to instill confidence.

GUIDANCE COULD BE MORE TELLING THAN DATA

Recent economic data releases are beginning to reflect in more detail the impact of COVID-19 as retail sales, housing, and unemployment have fallen below already lowered expectations. Conversely, we believe that only March, of the three months included in the first quarter, was meaningfully impacted by the virus. So Q1 earnings reports will be less reflective of COVID-19’s true impact, in our opinion. In January, FactSet reported consensus forecasts for earnings growth of about 4% on a year over year basis for the first quarter. Since the onset of the COVID-19 shutdown, estimates have dropped sharply and will likely continue to fall. As growth projections continue to deteriorate, the year over year decline in earnings could be the largest since the third quarter of 2009. Sectors expected to be hit the hardest include energy, consumer discretionary, industrials, and materials.

RIVERFRONT PORTFOLIOS LEANING INTO QUALITY AND GROWTH:

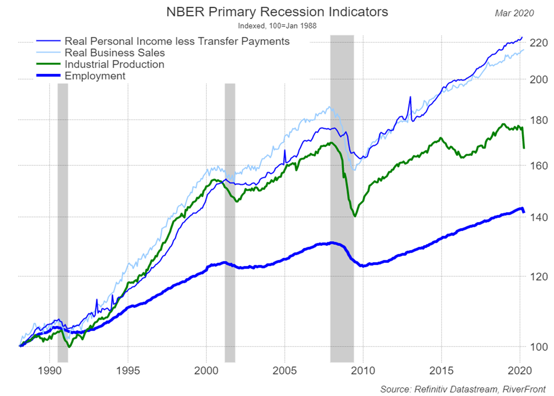

As the COVID-19 shutdown lingers, we believe more cyclical industries could have greater difficulty rebounding quickly. As an example, leaders from The International Monetary Fund (IMF) have expressed concern that we could experience a contraction of as much as -3% to global growth compared to their forecasts from earlier this year of positive growth of 3.3%. In the US, the probability of a recession in 2020 also appears to be increasing as the indicators monitored by the National Bureau of Economics are beginning to decline as can be seen in the above chart.

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Over the past month, we have enacted a series of changes to our strategies to lower the exposure to more cyclical sectors. We have lowered allocations in energy and materials and expect these sectors to continue to be some of the most volatile with uncertainties surrounding the restart of economies around the globe. With expectations that quality and growth will fare better as we navigate this recessionary environment, we have tilted more toward sectors such as technology and health care.

VALUATIONS WILL LIKELY BE BASED ON RECOVERY EXPECTATIONS RATHER THAN 2020 SHORTFALL, IN OUR OPINION

It is not out of the ordinary for investors to look through the current state of deteriorating growth and anticipate better times ahead. The strong performance of US equity markets in 2019 was proof that investors were willing to look through sluggish conditions to assign higher market valuations. Last year, equities generally traded above 5-and 10-year average forward multiples on the basis that 2020 would bring a resumption of double-digit earnings growth. It is likely that the growth investors were expecting will not materialize, and many companies have now suspended earnings guidance for this year.

We believe this setback in the economy will be significant but temporary. We believe corporate leaders will set the tone, as to the magnitude of the impact, with their guidance. Comments from leaders in sectors such as consumer discretionary and industrials could be particularly helpful in gauging tone. A resumption in consumer spending and corporate capital expenditures will be necessary to pull the economy out of this economic slump. Leaders of banks and other financial institutions could shed light on the impacts they are seeing from some of the recently enacted stimulus programs to help small businesses. Senior management teams from healthcare companies will likely give updates on treatments and testing, both of which are fundamental to getting the US workforce back in place. In recent days, markets have rallied on news of fewer cases of the virus and lower number of deaths. There is also optimism around the unprecedented amounts of stimulus both here and abroad. The bold reassurance on the part of the Federal Reserve with the commitment to do whatever it takes to support the US economy has also been met with investor enthusiasm.

FOR RIVERFRONT, IT REALLY ISN’T DIFFERENT THIS TIME

Most folks on Wall Street cringe when they hear the question, “Is it different this time?” As it relates to the magnitude and swiftness of the crisis, we agree that this is different. The degree of the shutdown, the historic levels of stimulus both here and across the globe, and of course the sad reality of the human toll are all unprecedented. There is no model for answering questions such as how much, how long, or when. For the RiverFront Investment Team, however, this time is not different. Our longstanding investment process, framed by strategic asset allocation, a tactical overlay, security selection, and risk management continue to guide our decision making even when it feels as though the world is different.

In conclusion, we continue to believe the S&P 500 will be higher in 12 months but expect volatility to continue as we navigate the rolling peaks of the COVID-19 and rally around the plans to restart the US economy.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

You cannot invest directly in an index

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1158520