By Doug Sandler, Chris Konstantinos & Rod Smyth, RiverFront Investment Group

Volatility is back….and with a vengeance. Recently, few days have gone by that did not involve day-to-day stock market price swings of 1 or 2%, often times within the same day. We anticipated the return of volatility and noted in our 2018 Outlook, that quantitative easing led to less market volatility and fewer 10% and 15% pullbacks than normal. As the QE era draws to a close, equity investors will likely need to prepare for a return to normal market volatility. A return to normal entails more frequent “normal” 10% and 15% market corrections. While volatility may be feared by many investors, there are several good reasons for long-term investors to welcome it back, despite its unruliness.

Volatility is often the Price Investors pay for Higher Returns

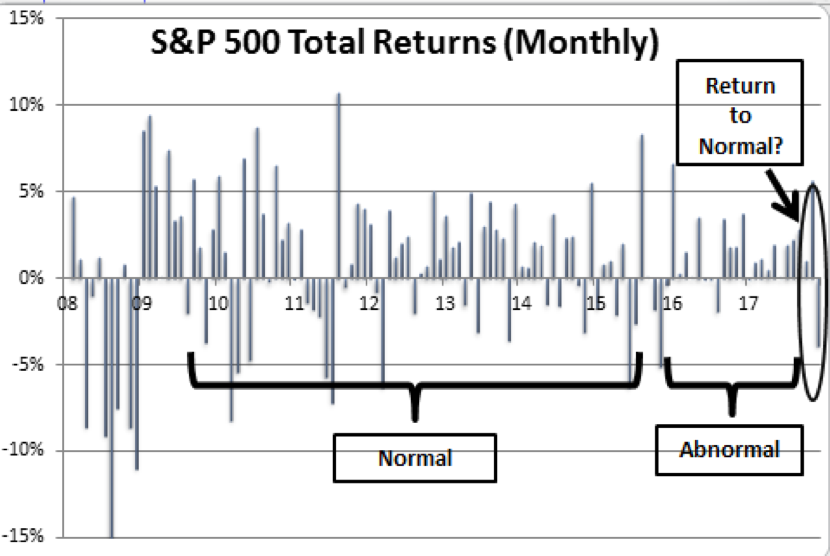

There is no free lunch in investing. According to a recent study published by NYU-Stern, common stocks have offered 3 to 5 percentage points above bonds and cash over the last 50 years. The higher long-term returns for equities come at a cost, which is day-to-day price predictability, i.e.: volatility. ‘Normal’ volatility for the US equity markets has historically equated to regular 10-15% drawdowns. According to Jim Stack of InvesTech Research, who studied market data going back to 1922, a 5% correction occurs about every 7 months and a 10% correction can be expected every 26 months. As can be seen in the monthly drawdown chart on the right, the resurgence of volatility in 2018 appears, thus far, to be a return to ‘normal’ after an ‘abnormal’ period of low volatility.

![]()

Source: Factset, RiverFront. Data from 3/1/08 through 2/28/18. Individual investors cannot directly purchase an index. Shown for illustrative purposes only and is no indication of RiverFront performance. Past performance is no indication of future results.

Volatility Can Reduce bubble risk

Complacency is an enemy of equity markets since it can lead to the building of bubbles that if allowed to grow too large, can violently end a bull market. Volatility can act as a ‘pressure release valve’ for potential bubbles in the making. One of the hallmarks of this bull market that began in 2009, is regular ‘pressure releases’ like those that have occurred in small-caps, industrials and the commodity sensitive sectors over the past few years. We believe that the recent pressure releases in technology and low volatility stocks has the potential to further extend the duration of the current bull market. For example, the forward price/earnings multiple on the S&P 500 has dropped almost 5 multiple points since volatility returned in late-January.

Volatility and Risk are not Synonymous:

- Strategic Objective – Attaining the Long-Term Target:

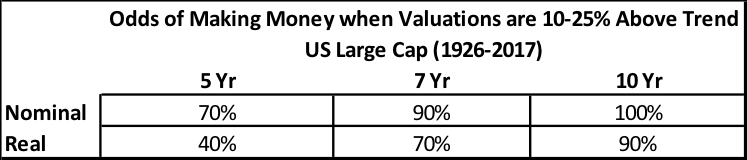

Strategically, we are time-frame oriented investors and therefore view risk as the potential of losing real (inflation-adjusted) money at the conclusion of our investment horizon. From this perspective, for long-term investors, we do not believe risk is represented by day-to-day price volatility since all equity downdrafts since 1926 have been recovered. In other words, we would rather make money in five years and endure temporary market declines than have our money predictably eroded by inflation over that same period by not being invested. For portfolios with time horizons of five years or more, we do not view the market as ‘risky’ per se at current valuations (all investing carries with it the risk of loss). The table below shows the historical odds of making money in US large-caps, according to our proprietary Price Matters® model, when they were purchased 10-25% above their long-term trend-line as they are now. As can be seen, the odds of positive nominal returns (not adjusted for inflation) are tremendously in the investor’s favor over all three time horizons, in our view. According to Price Matters®, the odds of positive real returns are also on the side of investors with time horizons over 7 years. Past performance is no guarantee of future results and the performance shown above is no indication of RiverFront portfolio performance.

- Tactical – Sticking with the Plan:

Our tactical process recognizes that, as John Maynard Keynes once said, “The market can be irrational longer than you can remain solvent”. Therefore, while a ‘just ride it out’ response may be appropriate for those with long-time horizons and the willpower to ignore the news and their monthly account statements, it is an unrealistic demand of the average investor. To navigate these periods, RiverFront has developed proprietary tactical and risk management processes. Investors in our portfolios should know that our tactical and risk management teams are ‘on the case’ and have plans in place for multiple market scenarios; both good and bad. This knowledge should help calm nervous investors who feel like they need to respond to the recent volatility themselves. Part of the reason for outsourcing this decision to us is the fact that volatile markets can be exceptionally challenging to navigate. In our view, successful navigation requires objective, unemotional tactical and risk management processes balanced with subjective oversight to insure those processes are properly calibrated for the environment. While there is no guarantee that our processes will insulate the investor from participating in downside risk or missing out on upside opportunity, we do believe that this balanced approach can help protect portfolios while minimizing the risk of getting whipsawed.

Volatility can send important messages about positioning and highlight monitoring priorities: The saying: ‘a person’s true character is revealed under pressure’ can also be applied to stocks. Amidst the noise of volatility there can be important messages that often provide indications of the market’s future direction. Investments that perform significantly better than would have been expected during periods of volatility reflect underlying strength that will likely persist when the market settles down, in our view. Conversely, those investments that perform significantly worse than expectations can be expected to continue to underperform when the volatility ends. For example:

- Performed Above Expectations: Developed International, US Small-caps and Consumer Discretionary

- Performed Below Expectations: Energy, Staples, and Healthcare

Volatility can send important messages about positioning and highlight monitoring priorities: The saying: ‘a person’s true character is revealed under pressure’ can also be applied to stocks. Amidst the noise of volatility there can be important messages that often provide indications of the market’s future direction. Investments that perform significantly better than would have been expected during periods of volatility reflect underlying strength that will likely persist when the market settles down, in our view. Conversely, those investments that perform significantly worse than expectations can be expected to continue to underperform when the volatility ends. For example:

- Performed Above Expectations: Developed International, US Small-caps and Consumer Discretionary

- Performed Below Expectations: Energy, Staples, and Healthcare

Parting Thought: Volatility is a symptom of the market doing its job. At its core, the stock market’s purpose is to value companies. The market regularly must perform its job under duress amidst changing or incomplete data. When the data is most dynamic it can be expected to be its most volatile as buyers and sellers digest all the new data and uncertainty. Without markets acting as a clearinghouse for investment insight, every investor would need to constantly and accurately assess all new information before buying or selling a stock. While not always pretty or perfect, author James Surowiecki noted in his classic book The Wisdom of Crowds, “the fairest price is the price that results from the combined wisdom of millions of individuals transacting independently.”

Doug Sandler, CFA, is Global Strategist; Chris Konstantinos, CFA, is Chief Investment Strategist; and Rod Smyth is Director of Investments at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

RiverFront’s Price Matters discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation. For more information, please visit our website: www.riverfrontig.com

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

These materials include general information and have not been tailored for any specific recipient or recipients. Accordingly, these materials are not intended to cause RiverFront Investment Group, LLC or an affiliate to become a fiduciary within the meaning of Section 3(21)(A)(ii) of the Employee Retirement Income Security Act of 1974, as amended or Section 4975(e)(3)(B) of the Internal Revenue Code of 1986, as amended.