SUMMARY

- Small-cap stocks are not as ‘cheap’ as they first appear

- Credit and interest rate conditions are a major concern, due to a shorter debt cycle.

- This creates an unfavorable backdrop for investing in small-caps currently, in our view.

Our Framework: ‘Price Matters’… but so does Macro and Earnings Data

With favorable economic and earnings tailwinds, we believe that the S&P 500 is still attractive in the short and medium-term (see Weekly Views from January and March 2024 for more on this topic). However, from a longer-term perspective, we see limits to returns for large-cap US equities as an asset class, opening the door for potential relative outperformance from other market segments.

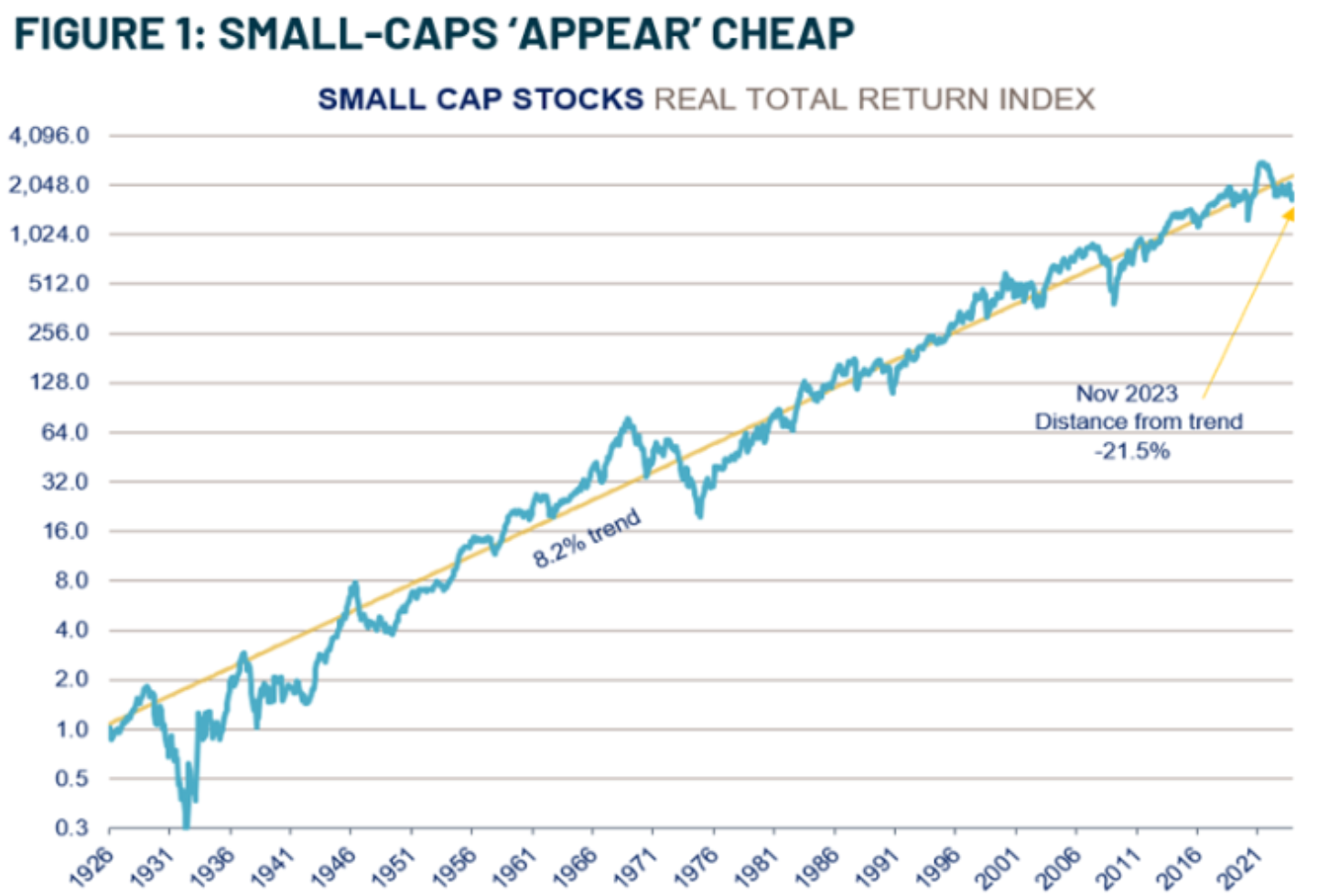

Smaller public companies with a market capitalization below $2 Billion (‘small-cap’) are a candidate for outperformance, given their cheaper valuation and faster historic growth versus large-caps. Based on our Price Matters® framework (Figure 1, right), small-caps have a faster long-term return trend (8.2%, versus 6.4% for large-caps), and currently are trading at 21.5% below that trend. If history is any guide, that below-trend condition suggests higher-than-average long-term total returns for small-cap over the next 10 years. However, we believe that valuation is a ‘condition’ and not necessarily a ‘catalyst’ for better returns, if not supported by growing corporate earnings. Unfortunately, small-cap’s current earnings outlook is less positive than large-cap in our view, with interest rate headwinds being the largest contributor to this dimmed outlook.

Source: RiverFront Investment Group, calculated based on data from CRSP 1925 US Indices Database ©2024 Center for Research in Security Prices (CRSP®), Booth School of Business, The University of Chicago. Data from Jan 1926 through Nov 2023. Past performance is no guarantee of future results. It is not possible to invest directly in an index. RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation. Blue line represents the Small Cap Real Return Index. Yellow line represents the Annualized Real Trend Line of Small Cap Real Total Return Index according to Price Matters®. Shown for illustrative purposes only, not indicative of RiverFront portfolio performance. Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed. The chart above uses a logarithmic scale. Line movements will be dampened/subdued based on the exponential y-axis.

Placing valuation differences into a proper perspective, we believe there are three elements that drive exceptional equity returns over time: 1.) a reasonable starting valuation, 2.) a macroeconomic environment that produces a tailwind, and 3.) earnings growth that is capturing that economic tailwind. Using this framework, our position on small-cap equities becomes clearer. While valuations seem attractive, we think higher interest rates have created a macro headwind that will continue to negatively impact small-cap earnings to a greater extent than large-cap.

Top-Down Assessment: Small-Caps Impacted More by Higher Rates

From a macro perspective, we believe the US economy is the strongest in the world, based on both leading activity and historic resilience (see Weekly View on US Economic Exceptionalism). While this economic strength should theoretically provide a tailwind to small-cap revenue, rising interest rates have created a significant headwind for smaller companies as they work to convert revenue into earnings. While higher rates impact all indebted companies to some degree, higher interest rates tend to affect small-cap companies more acutely than large-cap companies.

- Small-caps tend to use more debt than large-caps: Small-caps tend to have higher debt as a percentage of assets and lower coverage of debt payments as a multiple of their earnings, meaning they are more susceptible to credit issues.

- Small-caps tend to borrow at higher rates: The average credit quality of large cap companies in the S&P 500 is BBB+, which is considered ‘investment grade’. However, the average credit rating for all companies in the US is BB, which is considered to be ‘speculative grade’ or high-yield. This suggests that small-caps are typically forced to borrow at higher rates than large.

- Small-caps tend to borrow for shorter periods than large-caps: High yield bonds tend to have shorter maturities, and a larger proportion of debt for smaller companies is in floating rate loan products. This means that small-caps are more susceptible to rising rates and refinancing risk.

An additional wrinkle has been in the small-cap banking system. Faced with a backdrop of higher rates, small-cap banks face challenges due to many of their listed assets being “underwater” – whether they are treasury bonds or commercial real estate. This provides both a direct headwind for small-cap banks, and an indirect headwind for all smaller companies that rely on these banks to fuel growth – they are restricting lending when it is needed the most.

This matters because, while we do not expect a recession or widespread defaults, we also do not believe rates will fall back to 2020 levels. Thus, the current interest rate environment creates near-term headwinds for small-cap earnings, as existing debt is refinanced at current rates. There are also a number of sectors where we view the inter-sector dynamics of small-caps unfavorably compared to their large cap counterparts (we will have a follow-on piece outlining these differences in more detail shortly). The key takeaway is that profitability and earnings growth are very consistent with our negative macro assessment of small-cap, making the small-cap undervaluation seem justified to us.

Conclusion: Small-Cap isn’t all it’s Cracked up to be Yet… Unless Interest Rates Stabilize at Lower Levels Than We Expect

Revisiting our intrinsic value framework, here is a summary of our thinking on small-caps:

- Small-Cap Economic Environment: While we believe that the US economy will remain strong, the headwinds of higher rates impact smaller companies to a much higher degree.

- Small-Cap Earnings: Earnings growth has lagged in several key sectors versus large-cap brethren, consistent with our view of headwinds due to higher rates.

- Small-Cap Valuations: Given our concerns about earnings, small-cap companies might be a ‘value trap’ in the near term. That said, given our favorable view of the US economy, we can see small-cap companies becoming attractive if interest rates stabilize at a level lower than they are at present.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Small-, mid- and micro-cap companies may be hindered as a result of limited resources or less diverse products or services and have therefore historically been more volatile than the stocks of larger, more established companies. Please see the end of this publication for more disclosures.

For more news, information, and strategy, visit the ETF Strategist Channel.