Markets Inch Higher in April

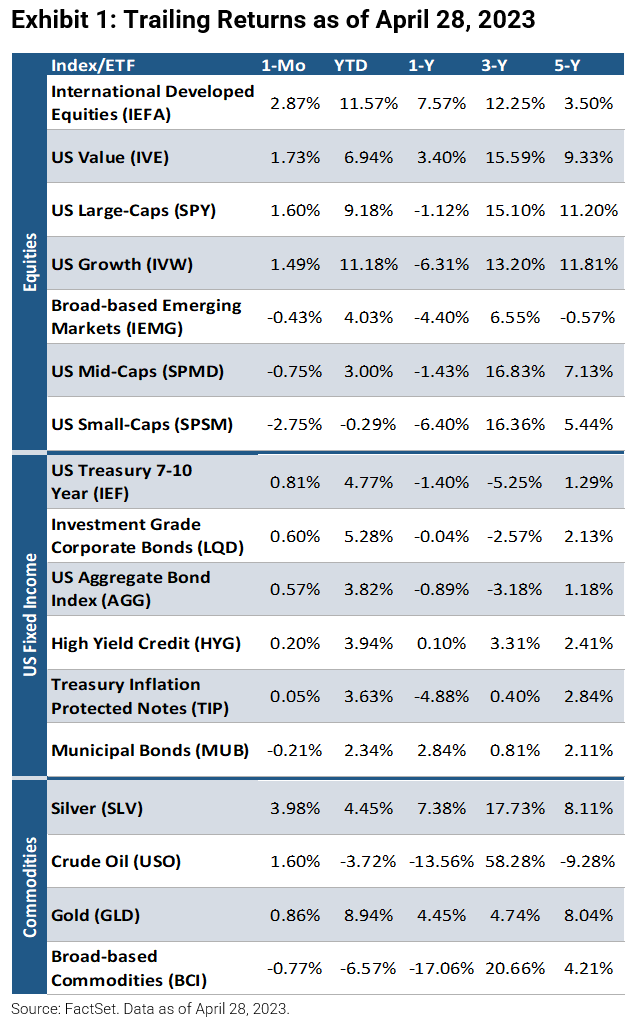

Despite a slowing economy, lingering inflation concerns, and further banking turmoil, all three major US indices posted gains in April likely on the back of better than expected earnings. International developed equities (+2.9%) and US value stocks (+1.7%) were among the best performers while US small-caps (-2.8%) and US mid-caps (-0.8%) were among the worst. Bonds were mostly higher as 7-10 year US Treasuries increased 0.8%, investment grade corporates rose 0.6%, and the US Aggregate Bond Index gained 0.6%. Commodities produced mixed returns as silver, crude oil, and gold were up (+4.0%, +1.6%, and +0.9%, respectively), while broad-based commodities were down (-0.8%).

Fed to Hike and Possibly Pause Thereafter

At the upcoming May FOMC meeting, the Federal Reserve is expected to raise interest rates by 25 bps, following an increase of the same magnitude at the March meeting. The hike would leave the federal funds rate at the 5.00–5.25% range, its highest level in 16 years. The modest rate increase would come after easing but still elevated inflation prints via CPI (Consumer Price Index) and PPI (Producer Price Index) released earlier this month. The high level of interest rates has started to slow the economy according to Q1 GDP, cooling factory activity and consumer spending, and declining leading economic indicators. Additionally, the recent failure of First Republic Bank, which comes after two mid-sized banks collapsed in March, reveals the stresses that high interest rates are putting on the banking system, and may be a warning sign for policymakers on how high they can take rates. After the May meeting, many anticipate the Fed to pause as long as inflation and economic data continue to weaken. Regardless, “We are much closer to the end of the tightening journey than the beginning,” as Cleveland Fed President Loretta Mester recently stated.

Small Businesses Pull Back

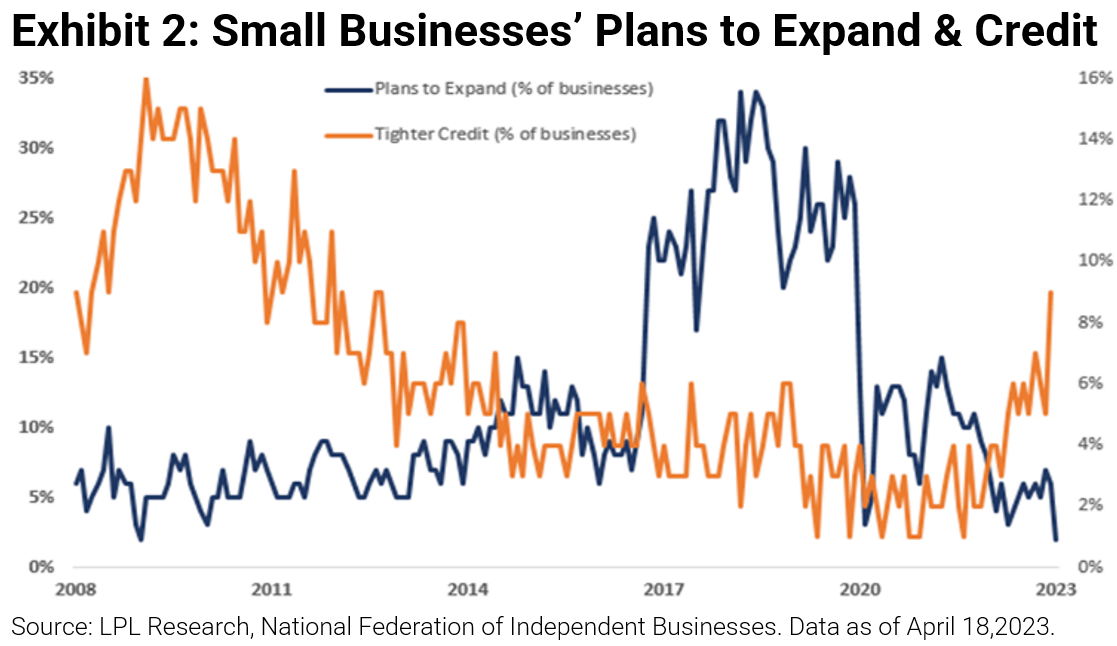

After multiple bank failures, lending standards have tightened, leading to record declines of loans and leases. Consequently, small businesses, which are often referred to as the backbone of the economy, may not fare well in coming months. According to LPL, the fewest small businesses since 2009 have plans to expand.

Forecasts are Down, But Earnings are Holding Up

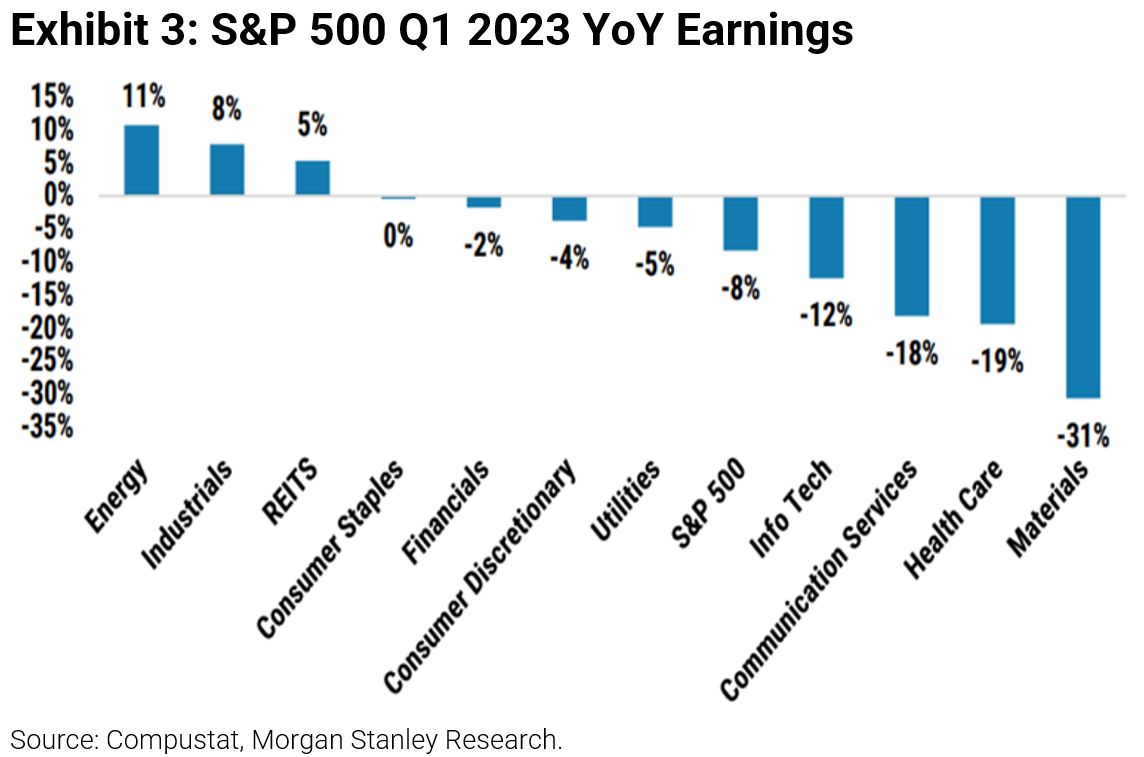

Earnings estimates have been downgraded. Year over year, only the energy, industrials, and real estate sectors are expected to see an increase in Q1 2023 EPS. Moreover, the S&P 500 is forecasted to see an 8% drop in EPS. However, this quarter’s earnings season has been better than expected so far. Through Friday, April 28th, 53% of the index has reported and 79% of these companies have posted a positive EPS surprise per FactSet’s Earnings Insights. Will this trend last?

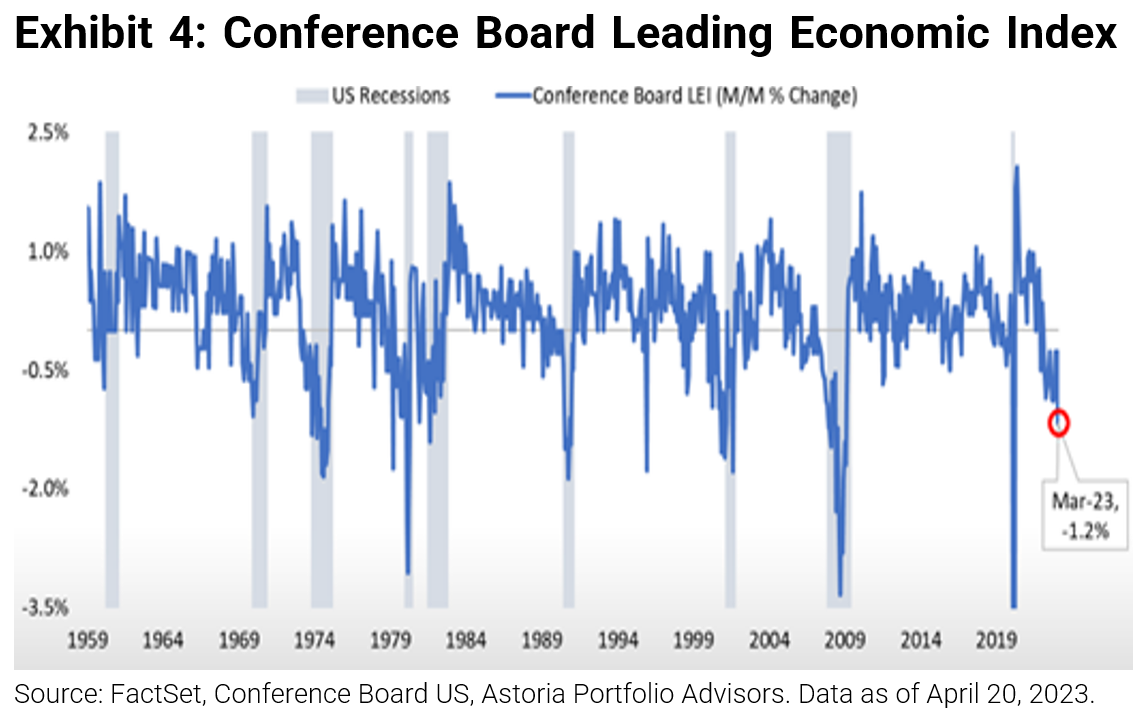

Leading Indicators Say Recession

In March, the Conference Board Leading Economic Index declined for its 12th straight month and continues to signal a contraction of the US economy ahead. The most recent print also notches the lowest level for the index since November 2020.

The Economy is Contracting and Recession Risks are Raised. How to Shift Your Portfolio

Amid a downward repricing in rate expectations and indicators that suggest the US is getting closer to a recession (re-steepening of the 2s10s yield curve, weak earnings forecasts, poor manufacturing data, slowing labor market, etc.), we believe decreasing value exposures and shifting more towards quality/growth at a reasonable price may be beneficial as such companies tend to produce stronger, more resilient cash flows and earnings. Moreover, three key points: 1) Market internals are awful; market breadth is the weakest in nearly 20 years. This is due to concentration of technology stocks and a flight to quality in Q1. 2) Markets are entering peak earnings season in the next few weeks, which will likely dictate trading for the near future. 3) Earnings estimates have been falling steadily and earning revisions are in negative territory–neither of these are constructive in our view. So what should advisors do? Go global, which has better risk/reward as the rest of the world has outperformed the US for 2 consecutive quarters now, get back into bonds, and use a healthy amount of alternatives to hedge portfolio risk. Remember, investing can be turbulent, but it is important to stay in the game. Those who have stayed fully invested have historically been rewarded.

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in IEMG, IVE, SPMD, SPY, SPSM, IVW, IEFA, MUB, TIP, AGG, IEF, HYG, LQD, BCI, GLD, USO, and SLV on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.