By Nicholas Porter, Portfolio Manager, VP – Research

Fixed income had been deemed a dull affair for much of the past four decades. It was considered by many as something of an afterthought compared to the time many spent on the minute handcrafting and tweaking of equity allocations. Bonds were to be the residual portion of a portfolio, assumed to give steady but unexciting returns, with fixed-income assets left in a broad index with little thought given to duration, credit, or even allocation percentages. Indeed, to the extent fixed income was considered at all, it was mentioned in the same breath as “ballast”; bonds were relied upon to have a negative correlation to equities in turbulent environments.

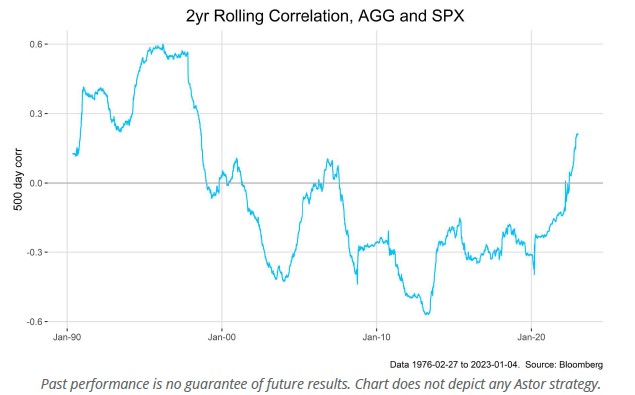

Investors who subscribed to the above have been badly disabused of that concept over the past 12 months. 2022 was a deluge for fixed income allocations that tracked the Bloomberg U.S. Agg Index or indeed most any fixed income with any sort of duration exposure at all, and the 60/40 portfolio (of 60% S&P 500 and 40% AGG) had its worst year in three decades, due in part to this side of the allocation ledger.

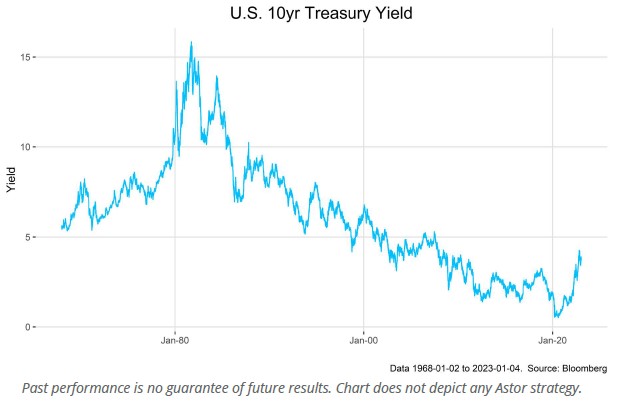

The post-Volcker era has seen a remarkable secular downturn in rates for almost 40 years. As a result, bond investors had been lulled into a false sense of security. Academic papers since the Global Financial Crisis are full of the challenges of managing policy at the zero lower bound, secular stagnation, Japanification of global financial markets, permanent disinflation from demographics, the savings glut, and so forth.

Quantitative easing and other measures installed to depress rate levels across the complex in an environment where prices for goods and labor posed no threat. Inflation of the type seen today, and the global monetary policy response, was almost unimaginable just two short years ago.

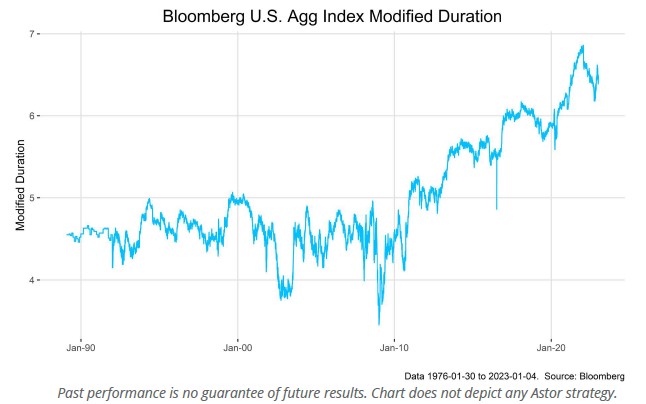

The post-pandemic era ushered in both supply and demand side pressures that set goods and services prices on a path not seen for decades. In response, duration across fixed income has increased across global bond markets as lower rates and demand for yield have allowed issuers to go further out of the curve. As a result, many investors were highly exposed to changes in monetary policy, but few worried about the potential for rising rates given the experiences of the past four decades.

In addition to juicing bonds’ total returns through capital gains, the decline in rates since the 1980s led to a belief that the negative correlation between stocks and bonds in times of economic stress is immutable. The reasoning was simple and correct so far: in an economic downturn, equities will sell off as future cash flows are revised downwards, and bonds will rally as central banks lower rates. Similarly, in an economic expansion, stocks will rise, and bonds will fall. Not considered, of course, was the spectre of inflation. In a scenario where central banks are raising rates because of high inflation rather than just high growth, or policymakers are forced to produce hawkish surprises, both stocks and bonds are likely to sell off.

The experiences of 2022 have thus made clear the need for active management in both fixed-income specific portfolios, as well as, in a multi-asset (asset allocation) framework. An investor approach to fixed income cannot be as simple as gaining exposure to a broad index and then forgetting about it – exposure to duration and credit need to be considered and closely managed. As evidenced by 2022, where you are exposed in duration and credit can have a dramatic effect on the returns of your fixed income portfolio. Having an approach that helps make those shifts can make all the difference.

DISCLOSURES: There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.