Author: Kimberly Woody

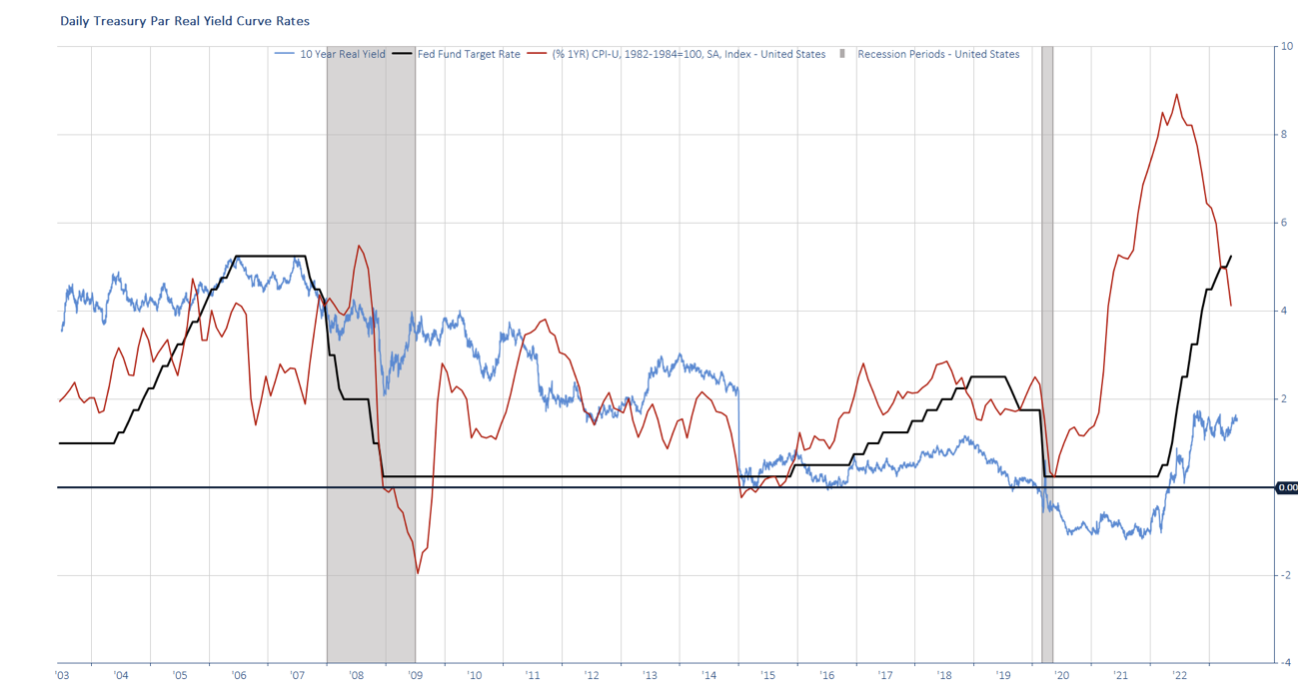

A real yield is an interest rate that has been adjusted to remove the effects of inflation. For example, in the chart below (blue line) the nominal ten-year interest rate has been decremented by the interest rate on a Treasury Inflation Protected Security (TIP) of the same maturity. The real rate offers a more realistic understanding of the true costs of borrowing as well as compensation for lending. As with a zero-interest rate policy, an environment in which one can borrow at rates lower than inflation should encourage investors to take on debt thereby invigorating demand and the economy. And borrow they did. But as we know, Corporate America opted to borrow and plow the proceeds in to share buybacks rather than invest in working capital. For consumers, it was the era of free money driving hard asset prices higher. The result of this appears to be debt and mountains of it.

Source: FactSet

Real rates have spiked resulting in a higher cost of credit for consumers and capital investment for corporations. The chart above also shows the Consumer Price Index (CPI), a commonly used measure of inflation from the Bureau of Labor Statistics. CPI is falling but still positive while higher frequency measures of inflation such as Truflation and the Adobe Digital Price Index are signaling deflation. As inflation subsides, higher real rates become even more restrictive and the impact of Fed policy balloons. Just as the Fed is understanding the lagged impact of its policy, the mallet becomes a sledgehammer. While higher yields mean investors have more money in their pockets from interest bearing investments, the cost of debt service just increased meaningfully. And who in this country is most in debt? Not baby boomers with real-time cost of living increases applied to social security payments and reliable IRA yields. For household formation, it is prohibitive. Not only are home prices inflated but the costs associated with financing that home have ballooned. The average rate for a loan on a used car is a whopping 11.5% if you have good credit (>750). For those in the lowest credit rung (<600 or 15% of the population) the rate is ≈22%. Average credit scores have improved over the years with sub 600 FICO scores representing 25% of the population in 2009 and 20% in 2017 but given the rise in revolving debt and with government payouts on the wane, the trajectory is not likely higher.

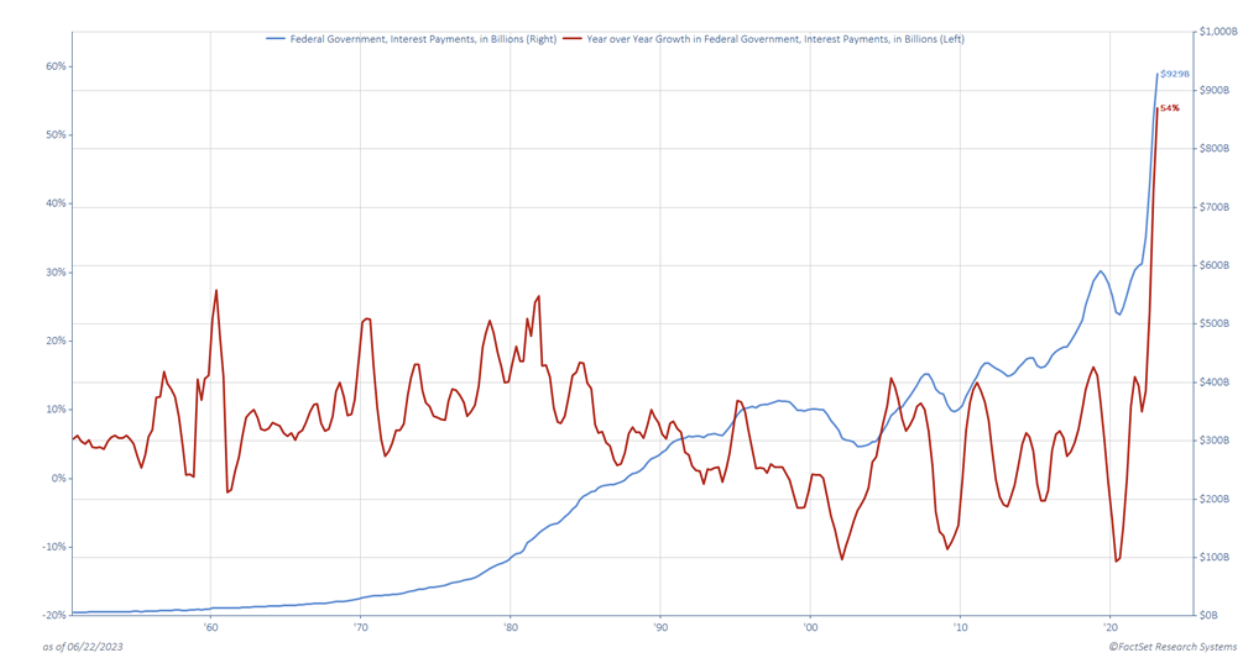

Ultimately, the global effect is unclear at this point. While persistent excess money in the system and ongoing fiscal spending is a tailwind for the economy, we are seeing pockets of weakness and they are worsened by higher rates. Used car prices are off -9.4% in the latest Manheim survey. Home prices leveled off but appear to be ticking back up. Housing starts are higher but remain below historical levels and are unlikely to improve the projected 4-6 million (depending on who you ask) new home shortage. And higher rates appear to be stifling sales of existing home as the 1.4 million homes on the market in May marked the lowest number since 2012 when Redfin began collecting data. Revolving debt is spiking while the savings rate remains low following records highs (and probably significant household wealth accumulation) during COVID. And just as the federal government is issuing more debt to fund budget imbalances, higher rates have driven interest payments more than 50% higher.

Source: FactSet

And now for the bright side of things. Federal Reserve Chair Jerome Powell and other central bank constituencies are hiking into a worldwide debt bubble. As described in the previous paragraph, most economies, the US included, do not appear to be able to sustain higher rates given their debt levels. Just like a household with unmanageable debt and ballooning debt service burdens, there are two ways out of this economic quandary. The first is worldwide currency devaluation to normalize asset prices relative to debt levels. This is neither a desired nor anticipated outcome, but the bears will roar. Bulls will point to Artificial Intelligence. Much is being forecasted regarding the magnitude of productivity and leverage AI will offer. And while we can’t be sure in terms of exact magnitude, the impact will likely be more transformative than the internet. Major modern advances have emerged faster and with greater impact with each successive development and AI appears to be the most revolutionary. Most importantly AI is likely demonstrably deflationary and extremely accretive to productivity. This new technological development should exert downward pressure on rates thereby reducing both debt and the interest burden associated with that debt. Quite simply we look to growing our way out of this and AI has the potential to do so in the not-so-distant future.

When all you have is a Hammer, everything looks like a Nail – Abraham Maslow

Sources: Adobe, CNN, FactSet, Federal Reserve, Manheim, NPR, Truflation, US News, Zillow

For more news, information, and analysis, visit the ETF Strategist Channel.

GLOBALT is an SEC Registered Investment Adviser since 1991 and, effective July 10, 2013, remains a Registered Investment Adviser through a separately identifiable division of Synovus Trust N.A., a nationally chartered trust company. This information has been prepared for educational purposes only, as general information and should not be considered a solicitation for the purchase or sale of any security. This does not constitute legal or professional advice and is not tailored to the investment needs of any specific investor. Registration of an investment adviser does not imply any certain level of skill or training. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information may be required to make informed investment decisions, based on your individual investment objectives and suitability specifications. Investors should seek tailored advice and should understand that statements regarding future prospects of the financial market may not be realized, as past performance does not guarantee and/or is not indicative of future results. Content may not be reproduced, distributed, or transmitted in whole or in part by any means without written permission from GLOBALT. Regarding permission, as well as to receive a copy of GLOBALT’s Form ADV Part 2 and Part 3, contact GLOBALT’s Chief Compliance Officer, 3400 Overton Park Drive, Suite 200, Atlanta GA 30339. You can obtain more information about GLOBALT Investments and its advisers via the Internet at adviserinfo.sec.gov, sponsored by the U.S. Securities and Exchange Commission. The opinions and some comments contained herein reflect the judgment of the author, as of the date noted. Investment products and services provided are offered through Synovus Securities, Inc. (SSI), a registered Broker-Dealer, member FINRA/SIPC and SEC Registered Investment Adviser, Synovus Trust Company, N.A. (STC), Creative Financial Group, a division of SSI. Trust services for Synovus are provided by STC. Regarding the products and services provided by GLOBALT: NOT A DEPOSIT. NOT FDIC INSURED. NOT GUARANTEED BY THE BANK. MAY LOSE VALUE. NOT INSURED BY ANY FEDERAL AGENCY