- Investors’ love affair with past winners is insatiable. The ‘conventional wisdom’ on Wall Street is that Artificial Intelligence, Bitcoin, US ultra mega-cap stocks, and market cap weighted strategies will continue to be the ‘big winners’ in 2024. Unfortunately, yesterday’s darlings seldom outperform in the future with the same risk-adjusted returns per unit of liquidity risk (this is important) as they did in the past. Paradigm shifts typically happen slowly and quietly, with most investors realizing after the fact.

- Many firms put out their 2024 reports with forecasts and predictions, but we find very few of them are actionable. We wish the authors would attach a link to their prior-year forecasts so we can judge how well they did. The goal of this piece is to not only provide unique thought leadership but to provide investors with actionable investment ideas. Here are our 10 ETFs for 2023 (click here) so you can evaluate our calls.

2024: Dawn of a New Cycle, There Will be New Winners

-

Content continues below advertisement

- The market is transitioning from an environment of interest rate hikes to an environment of interest rate cuts. There is a specific portfolio to own when rates are rising and an entirely distinct portfolio when rates are declining. The market is currently pricing in approximately five rate cuts as of December 7, 2023. This inherently translates into a new market cycle and hence a different portfolio construct.

- We are more constructive for 2024 than we were for 2023. The biggest risk we see is that lower rates shift back demand curves and re-ignite inflation, leading to rate hikes being priced back into the market. We argued in 2020 that inflation would be a sticky problem lasting for many years. This is a key reason why we are saying investors should always carry inflation protection. The irony of this call is that inflation-linked assets have low correlation to US index beta, carry well in a multi-asset portfolio, and trade at a 40-45% discount to the S&P 500 Index.

- While the profits recession may be over, corporates are not out of the woodwork. With wage growth expected to decline and hiring to be sluggish, earnings and fundamentals may be of focus when it comes to selecting stocks. Stock-specific has increased in 2023, and we believe it should rise further in 2024 as macro variables become of less importance while corporate earnings take center stage.

- We’ve had the fastest rate hiking cycle in nearly half a century, but we’ve had an economic expansion in 2023. Sure, it’s possible that tightening effects materialize in 2024 and the US experiences worse than expected growth, or even negative growth. But what’s going to happen to growth if the Fed cuts rates in the mid to later part of next year? Stocks are forward looking, and after two years of subdued returns for the average stock globally, it seems risks would be skewed towards the upside in this scenario.

- At the end of the day, market performance in 2023 was primarily driven by rates. Generally speaking, when rates went up, stocks went down. When rates went down, stocks went up. This relationship will be crucial to watch in 2023. Our view is that idiosyncratic and stock specific risk (corporate earnings, margins, etc.) will return in 2024 and macro factors will wane (the Fed, inflation). Back-to-back years of macro driven markets present hardships for any fundamental investor.

- Remember, we’ve been in a bear market for 2 years now. We highly doubt we will get five rate cuts next year, but the important point we want to deliver is that your portfolio should evolve in 2024 and look different from the past one to two years.

How Should Investors Position Their Portfolios in 2024?

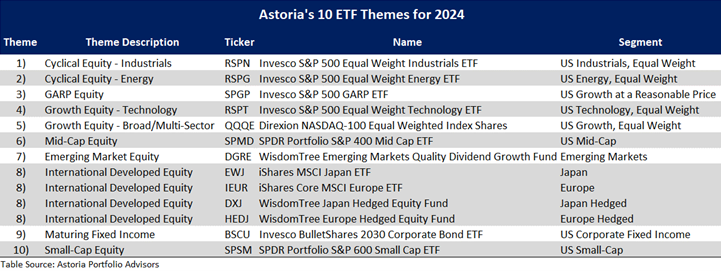

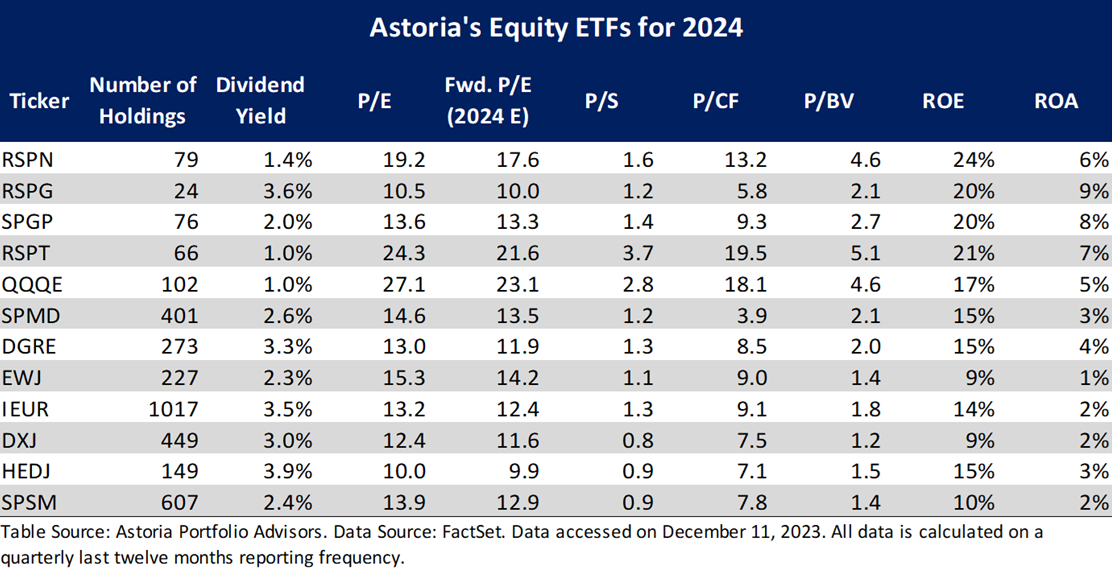

- Increase your equity beta and be overweight equities. Barbell your portfolio risk by owning cyclical growth (RSPN, RSPG, RSPT, and QQQE), transition from market cap weighted to equal weighted strategies, overweight inflation sensitive assets, allocate to international developed markets (EWJ, IEUR, DXJ, and HEDJ), and diversify away from US large-cap index beta. Astoria believes GARP (SPGP), broad market multi-cap quality, and US SMID (SPMD and SPSM) can help diversify portfolios away from US large-cap beta. A new cycle usually signals a change in market leadership.

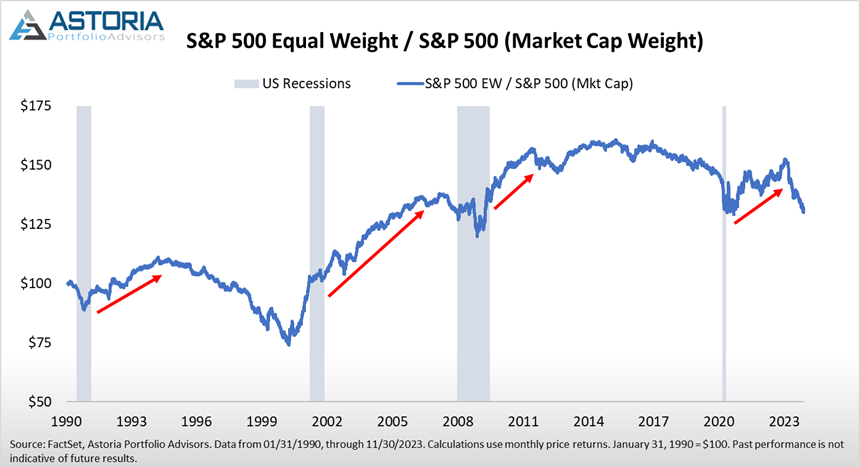

- Diversify away from the magnificent seven and equal weight over market cap weight. It’s okay to own the “magnificent seven” stocks, but we advocate reducing one’s exposure. As seen in the chart below, new market cycles have historically corresponded with equal weight outperforming market cap weight. If you were underweight growth or technology, close the gap by using equal weighted growth (QQQE) or equal weighted technology (RSPT).

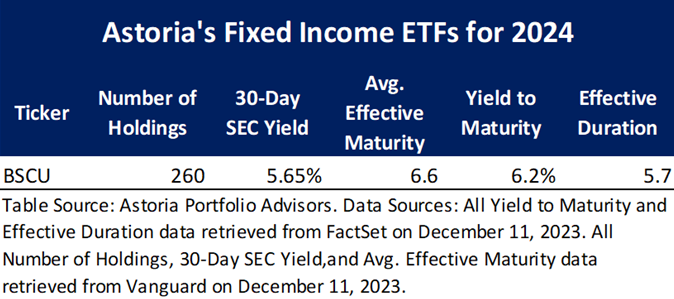

- Say sayonara to those T-Bills. One of our best ideas for 2024 is to use fixed income strategies that benefit from declining rates at the intermediate and back end of the curve (BSCU). If the underlying macro improves in 2024 and market leadership broadens, the opportunity cost of sitting in money market/T-Bills as yields decline could cause one to miss out on larger potential equity gains/fixed income price appreciation. Deploy that cash in the above equity cohorts or in fixed income via extending duration and increasing exposure to investment grade, high quality corporates and municipal bonds. Why? Given the level of starting yields, hypothetical forward returns for bonds look appealing. For instance, an LPL report dated November 20th, 2023, estimates that a 50bps decrease in interest rates would cause the Bloomberg US Treasury Index to gain over 8% in the next twelve months. Some may refer to this as a possibility to earn equity-like returns without equity-like risks.

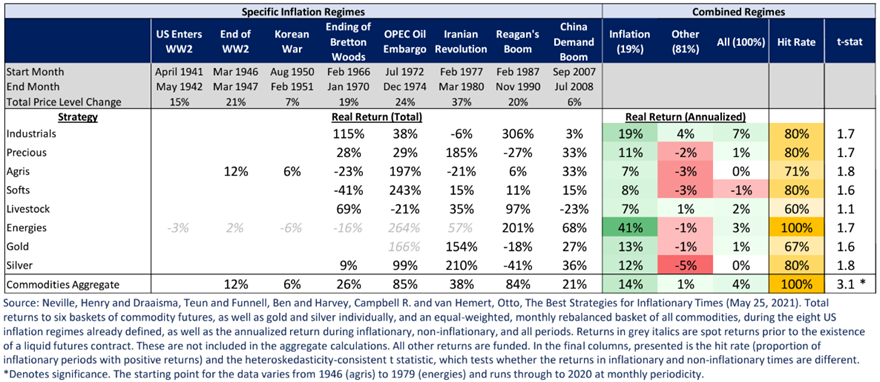

- Overweight inflation-linked assets such as energy, industrials, commodity equities, and physical commodities. As the table below shows, various commodities have produced positive returns with a high hit rate during prior inflationary regimes. When the profit cycle recovers, value centric stocks have historically performed well and many currently trade at a discount to the S&P 500 Index.

- We believe there’s north of 75% probability inflation will stay above 2% throughout 2024. We’ve had nearly 500bps of tightening and October annualized Core PCE is still at 3.5%, 1.75x the Fed’s 2% target. With 2024 being an election year, it is our view that the Fed backs off on aggressive monetary policy to let the political cycle run its course.

- Our bottom line is that the inflation problem is now more anchored on the supply side, which is tricky and takes years to shift. As mentioned in numerous posts, Apple is not going to shift its supply chains from Asia to the United States anytime soon.

- We are entering into a world of deglobalization, onshoring, and reshoring. In this new environment, investors should own real assets and stocks in sectors such as industrials, materials, energy, etc. From the thousands of portfolios we oversee, we still see remnants of the prior decade that are present in most advisors’ portfolios. Our view is that portfolios should be readjusted to reflect structurally higher real rates.

- Equity risk premiums may not be attractive for US large-cap index beta stocks, but they look relatively attractive elsewhere. Our big view is that investors really need to look at Europe and Japan, US SMID, and cyclically oriented sectors which will likely be the new leaders in a new market cycle that consists of structurally higher real rates and stubborn inflation. The earnings yield for developed Europe is currently hovering around 9-10%.

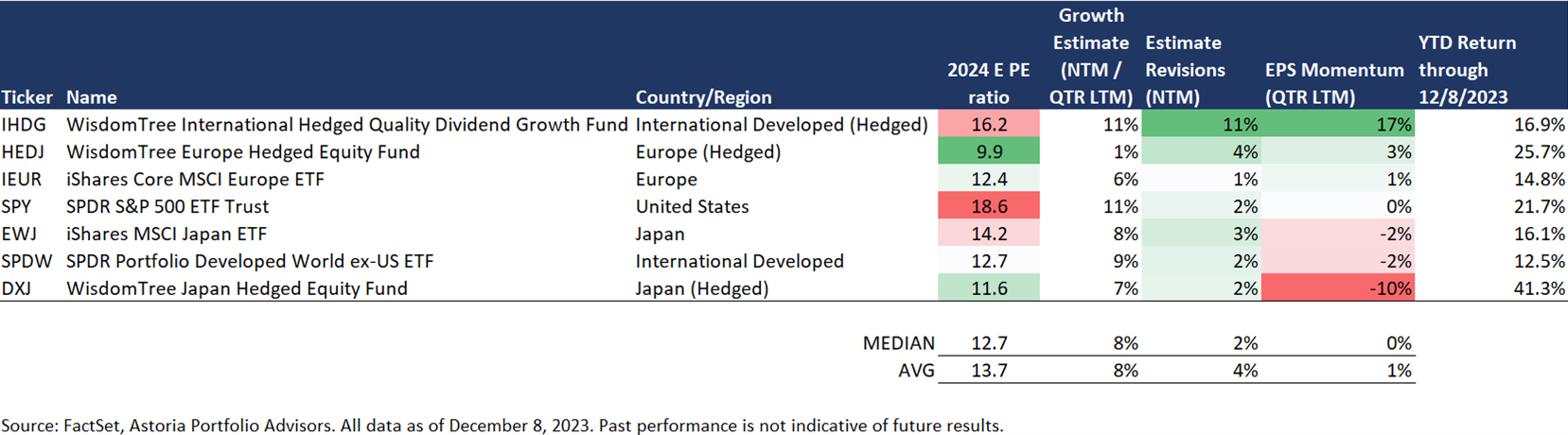

- Investors typically have a home country bias, but we encourage advisors to look at international developed markets (EWJ, IEUR, DXJ, and HEDJ). Europe and Japan, specifically, have appealing growth prospects. For clarity our firm diversifies our international equity allocations across hedged and non-hedged solutions. Depending on the risk tolerance and tracking error of our mandate, our portfolios consist of a combination of IHDG, SPDW, HEDJ, DXJ, IEUR, and EWJ.

- Use active managers for emerging markets as the region is highly nuanced (DGRE). High US interest rates have always been an impediment to emerging market investing; 2023 was no different. However, emerging markets are trading at substantial discount to the US and can aid in portfolio diversification.

Background Information on 10 ETFs for 2024

- Our team has been producing a dedicated year-ahead ETF outlook for over a decade. We were the first group to publish a dedicated ETF outlook with actionable ideas and we like that our peers are starting to throw their hats into the ring. We try not to repeat our ETFs from one year to the next, as our goal is to communicate unique and actionable thematic ideas for the investment community.

- Astoria runs various ETF managed portfolios with different risk tolerance bands and with different holdings. The commentary in this report is generally centered around our Dynamic and Risk Managed ETF Portfolios. We offer strategic ETF Portfolios with lower tracking error vs. their benchmark in which case will have different holdings then what’s included in this report.

- The ETFs highlighted in this report are solutions that Astoria finds attractive on a per unit of risk basis. However, this list is not meant to be an asset allocation strategy, a trading idea, or an ETF managed portfolio. As such, this list does not constitute a recommendation of any ETF. There are other ETFs that Astoria currently owns which are not highlighted in this report. Contact us for a list of all of Astoria’s ETF holdings.

- Any ETF holdings discussed are for illustrative purposes only and are subject to change at any time. Readers are welcome to follow Astoria’s research, blogs, and social media updates to see how our portfolios may shift throughout the year. Refer to www.astoriaadvisors.com or @AstoriaAdvisors on Twitter.

- Past performance is not indicative of future results. Investors should understand that Astoria’s 10 ETF Themes for 2023 is not indicative of how Astoria manages money or risk for its investors. Note that Astoria shifts portfolios depending on market conditions, risk tolerance bands, and risk budgeting. As of the time this article was written, Astoria held positions in RSPG, SPGP, RSPT, QQQE, SPMD, DGRE, EWJ, IEUR, DXJ, HEDJ, SPSM, SPY, IHDG, and SPDW on behalf of its clients.

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

There are no warranties implied. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements. Astoria Portfolio Advisors LLC’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links. Accordingly, the publication of Astoria Portfolio Advisors LLC’s website on the Internet should not be construed by any consumer and/or prospective client as Astoria Portfolio Advisors LLC’s solicitation to effect, or attempt to effect transactions in securities, or the rendering of personalized investment advice for compensation, over the Internet. Any subsequent, direct communication by Astoria Portfolio Advisors LLC with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

A copy of Astoria Portfolio Advisors LLC’s current written disclosure statement discussing Astoria Portfolio Advisors LLC’s business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov or from Astoria Portfolio Advisors LLC upon written request. Astoria Portfolio Advisors LLC does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to Astoria Portfolio Advisors LLC’s website or incorporated herein and takes no responsibility therefor. All such information is provided solely for convenience purposes only, and all users thereof should be guided accordingly. This website and information presented are for educational purposes only and do not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy. This website and information are not intended to provide investment, tax, or legal advice.

Past performance is not indicative of future performance. Indices are typically not available for direct investment, are unmanaged, and do not incur fees or expenses. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. All opinions and views constitute judgments as of the date of writing without regard to the date on which the reader may receive or access the information and are subject to change at any time without notice and with no obligation to update. Any ETF Holdings shown are for illustrative purposes only and are subject to change at any time. This material is for informational and illustrative purposes only and is intended solely for the information of those to whom it is distributed by Astoria Portfolio Advisors LLC. No part of this material may be reproduced or retransmitted in any manner without the prior written permission of Astoria Portfolio Advisors LLC. Investing entails risks, including the possible loss of some or all the investor’s principal. The investment views and market opinions/analyses expressed herein may not reflect those of Astoria Portfolio Advisors LLC as a whole, and different views may be expressed based on different investment styles, objectives, views, or philosophies. To the extent that these materials contain statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties.