By Denis Rezendes, Beaumont Capital

For the past two years I’ve attended the Berkshire Hathaway shareholder meeting in Omaha, Nebraska, known by many as the “Woodstock of Capitalism.” During the 2017 meeting’s question and answer section, a shareholder asked a seemingly simple question: at what rate can Berkshire Hathaway compound its book value per share over the long term?

For those who are unaware, Warren Buffett has long maintained that this measure, growth in book value per share, will equate to the stock’s long term performance. The old sage took a second to think and then responded, if my memory serves, somewhere just north of 5%, closer to 10% if interest rates move materially higher. This answer satisfied the investor in question and also contains the foundation for this piece which is – how do we set return expectations?

Real Interest Rates and Return Expectations

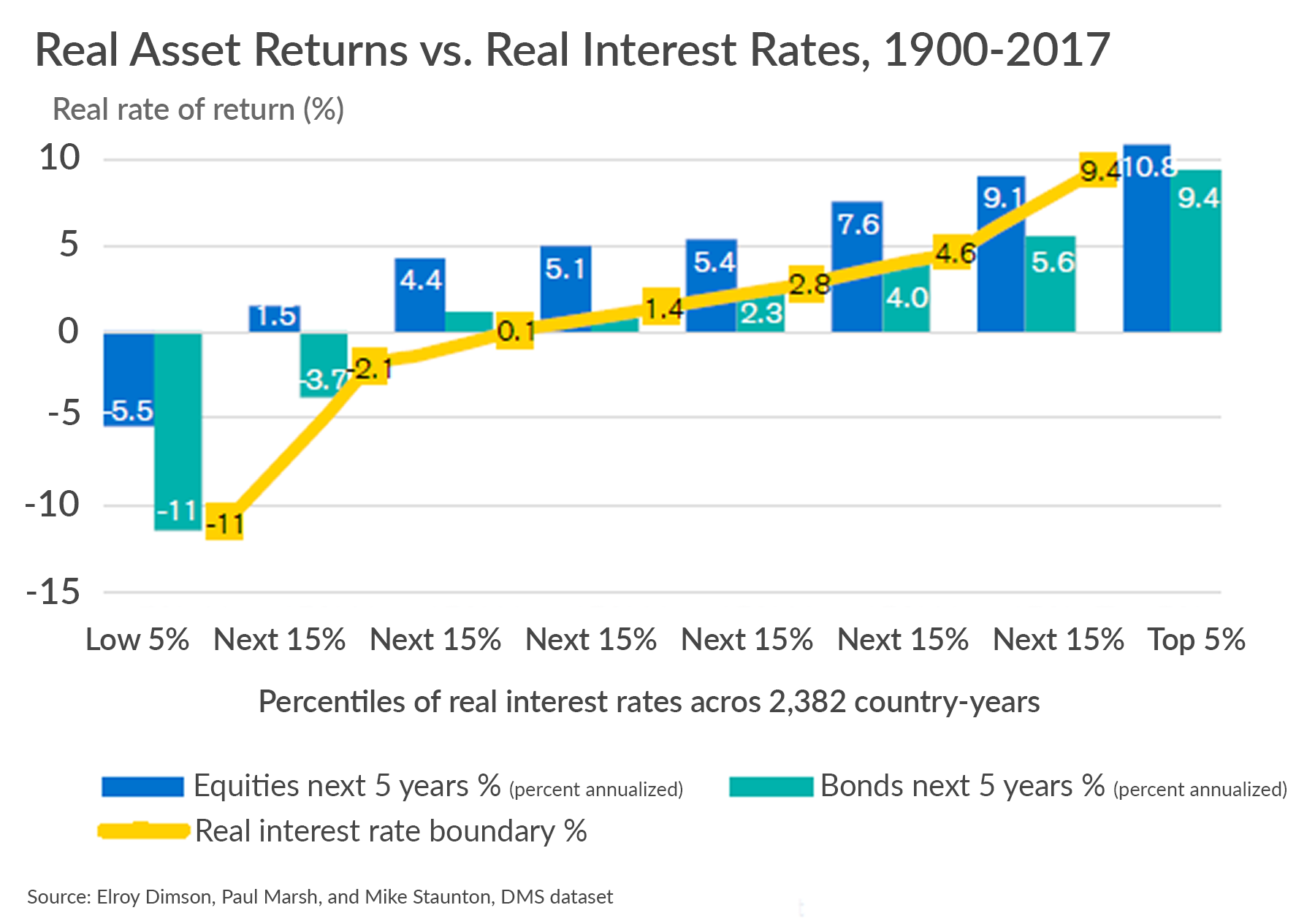

The key to setting investment return expectations is interest rates. More specifically the real interest rate, which is the quoted interest rate minus inflation. The chart below from the Credit Suisse Global Investment Returns Yearbook 2018 illustrates this in a compelling fashion.

The chart shows the five year forward real return for equities and bonds bucketed by the real interest rate at the beginning of the period. The sample includes 2,382 five-year periods, across 21 countries, taken between 1900 and 2017. In each percentile bucket, forward real returns for bonds were nearly identical to the real interest rate at the start of the period.

Building on top of this, forward real returns for equities are consistently 3-4% higher¹; this is the additional return that investors require to bear the greater risk present in equities, also known as the equity risk premium.

![]()

So what does this mean for us?

The base case is certainly below historical averages but doesn’t otherwise paint a gruesome picture. Applying the above analysis to our current investment landscape yields a forward real return for bonds of around 1% annualized and, adding the equity risk premium, a forward real return for equities of 4-5%². Taking these numbers and adding the market’s expectation for forward inflation, around 2%, suggests forward nominal returns of 3% for bonds and 5-7% for equities. While this relationship may hold true on average, a variety of factors will influence the actual results in any given time period. Even if this relationship holds true, we certainly won’t realize the returns in a straight line. Therefore, we’d caution against interpreting the results of this analysis as fact, and instead suggest using it as a base case to help set expectations.

If you’re satisfied with what we’ve provided above, feel free to stop reading. If not, please stay tuned for a follow-up piece on this subject. To subscribe to our blog for instant notifications, click here.

This article was contributed by Denis Rezendes, Research Analyst at Beaumont Capital Management, a participant in the ETF Strategist Channel.