By: BCM Investment Team

February’s retail sales losses were more severe than expected—with sectors following a familiar pattern—but have still managed to grow year-over-year. Manufacturing also felt the effects of last month’s freezing temperatures and underperformed expectations by over 3%. Housing prices meanwhile continue to soar in a trend that looks primed to continue as supply runs worryingly short. A $1,400 stimulus check may not make much of a dent in a down payment, but is it doing much good in a savings account? The 10-year UST yield hit a fresh 13-month high ahead of the Fed decision—which Bank of America called “one of the most critical events for the Fed in some time”—this week, inching closer to the 2% yield many fund managers believe could spark a 10%+ correction in equities. And what lies ahead on the international stage as commodities, EM exports, and new waves of Covid all climb higher?

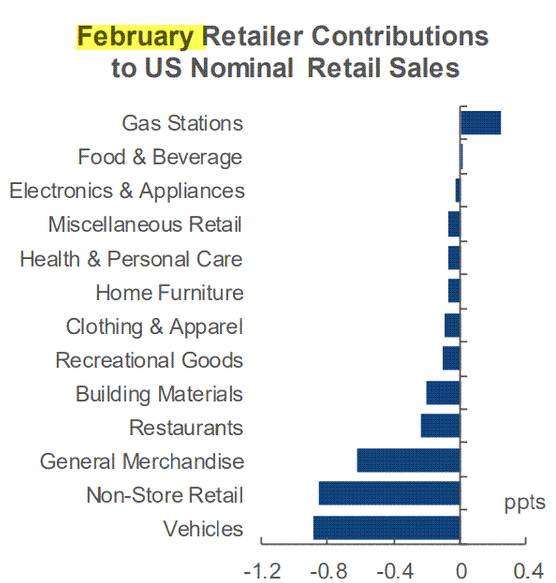

1. February’s deep freeze, together with the Covid hangover, caused U.S. retail sales to decline by 3% last month. Here’s the breakout:

Source: The Daily Shot, from 3/17/21

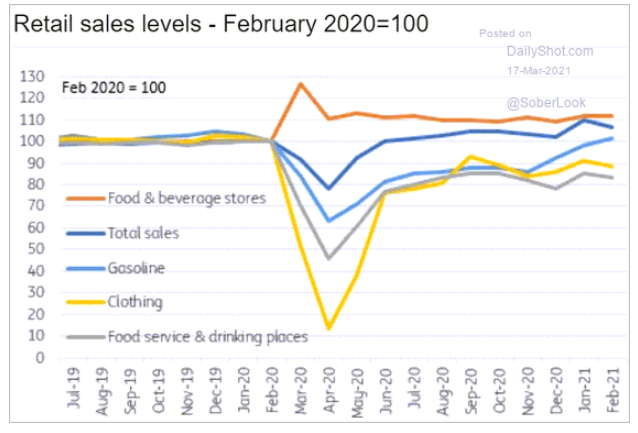

2. But overall, retail sales are still higher than in 2020. The Covid factor shows up again in clothing and restaurant/bar sales:

Source: The Daily Shot, from 3/17/21

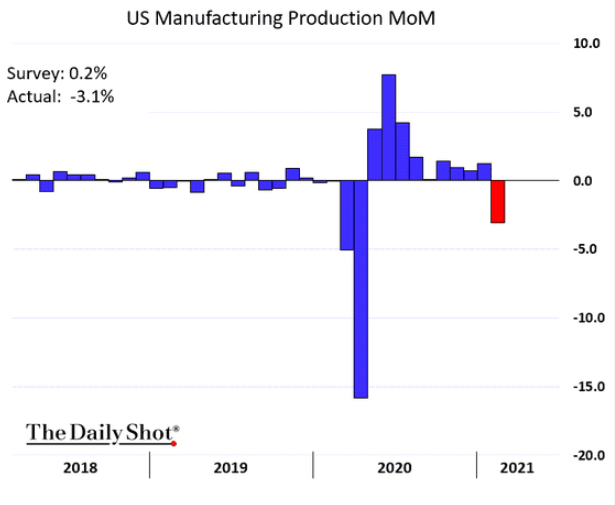

3. The same weather took its toll on manufacturing as well:

Source: The Daily Shot, from 3/17/21

4. New homes, after a decade of lackluster housing starts/completions, has caused the U.S. to be woefully short of housing stock.

Source: Census Bureau, from 3/17/21

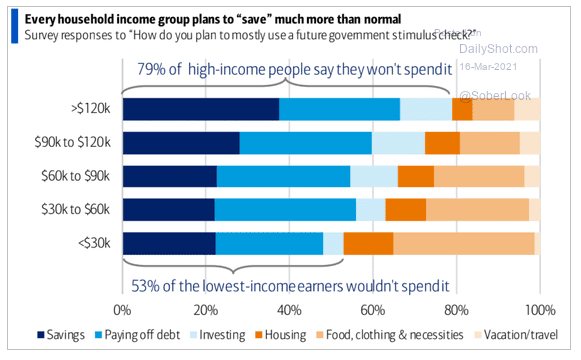

5. Stimu-less? 53-79% of recipients don’t plan to spend their new checks.

Source: BofA Global Research, from 3/16/21

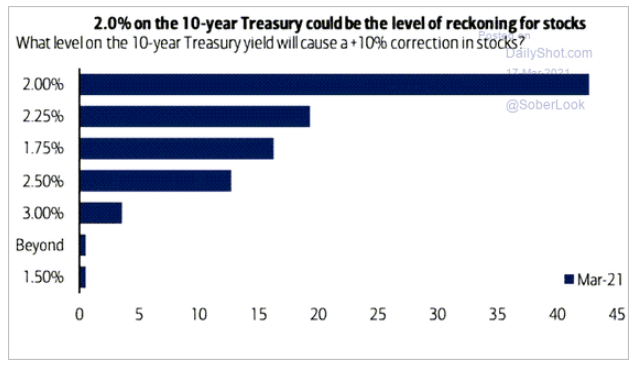

6. A survey of fund managers confirms “Rising yields don’t matter until they do.” With the 10-year UST yield around 1.65%, we might see who is right soon enough…

Source: BofA Global Fun Manager Survey, from 3/17/21

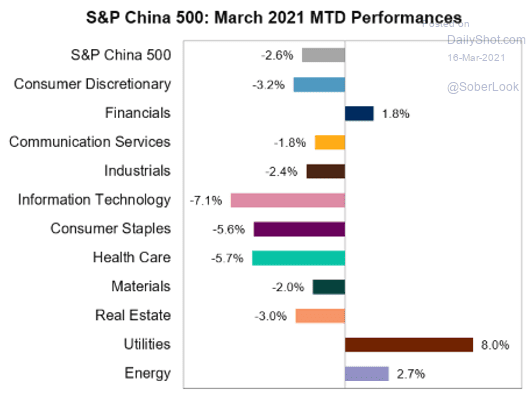

7. So far in March, China’s stock market is also looking at a possible leadership change:

Source: S&P Dow Jones Indices, as of 3/12/21

8. Boosted by rising commodity prices, EM exports are soaring:

Source: The Daily Shot, from 3/16/21

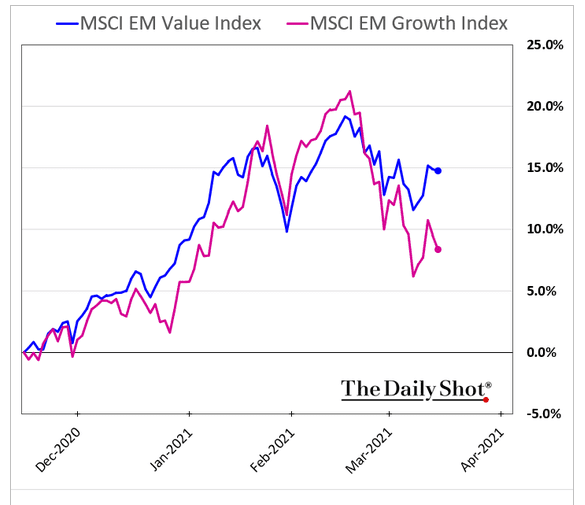

9. Yet EM stock prices aren’t following suit. Opportunity ahead?

Source: The Daily Shot, from 3/16/21

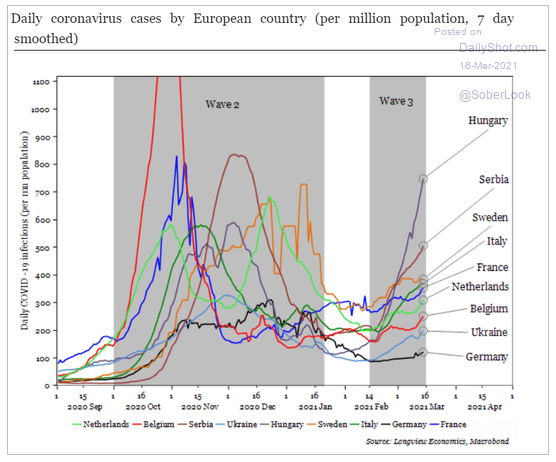

10. Europeans, who generally are way behind in vaccinations, are getting hit with a third wave of Covid. Will this delay their recovery further? It certainly won’t help travel…

Source: The Daily Shot, from 3/16/21

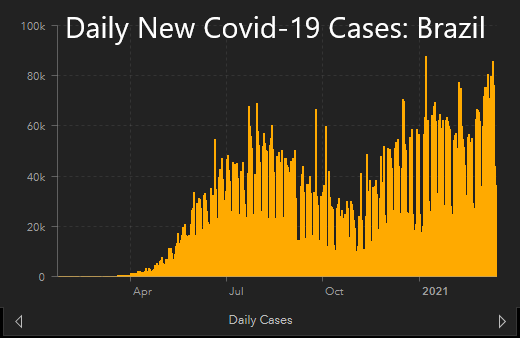

11. Brazil is also in a fierce battle with Covid as their second wave shows no signs of waning:

Source: JHU CSSE , from 3/16/21

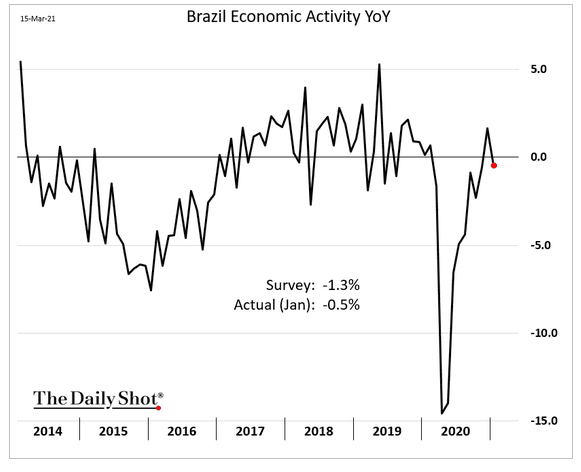

12. While better than expected, their economy felt the effects:

Source: The Daily Shot, from 3/16/21

This article was contributed by Beaumont Capital Management Investment Team, a participant in the ETF Strategist Channel.

For more insights like these, visit BCM’s blog at blog.investbcm.com.

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.