Bear markets signal leadership change

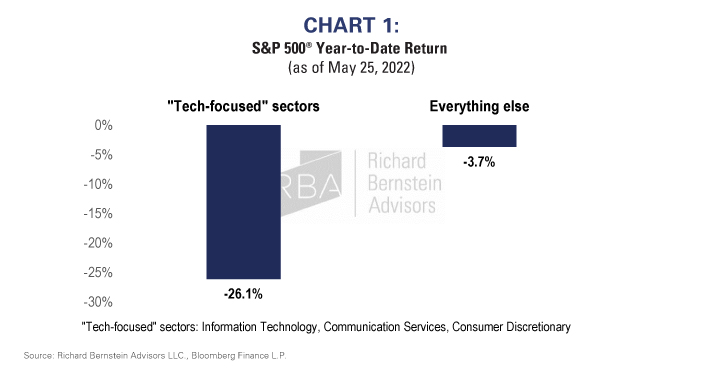

Bear markets always signal a leadership change within the overall equity market. The leadership going into a bear market is rarely, if ever, the leadership coming out. Because of this rule of thumb, we view bear markets as periods of extreme opportunity. In our view, this cycle has so far been no different: leadership seem to be changing as the current bear market progresses. (See Chart 1)

Bear markets occur when the economy structurally changes. Leadership before a bear market is typically geared to the economy in place, but leadership shifts as the economy shifts. Volatility occurs when a prior leadership suited to a pre-existing economy surrenders to a new leadership better matched to a new economic backdrop.

The economy is constantly changing, and markets adapt to those changes. History clearly shows it is unrealistic to expect one segment of the equity market to be appropriate for every economic scenario.

However, despite historical precedent, investors are typically hesitant to reposition portfolios when the economy changes. They tend to cling to the old leadership hoping those stocks’ underperformance is only temporary, and the economy and the markets will soon revert.

The current market volatility is not unique. Rather, it seems to reflect a significant shift in the economy which is being mirrored in sector returns. The global economy is going through major structural changes that seem likely to alter the secular trend in inflation and interest rates. It makes sense new leadership better suited for new secular trends are emerging.

The old leadership, which is now significantly underperforming, was geared to secular disinflation and lower long-term interest rates. The performance of so-called long duration equity themes like technology, innovation, disruption, and the like were predicated on lower long-term interest rates. Their outperformance reached true extremes when the Fed’s quantitative easing program (QE) further lowered long-term interest rates.

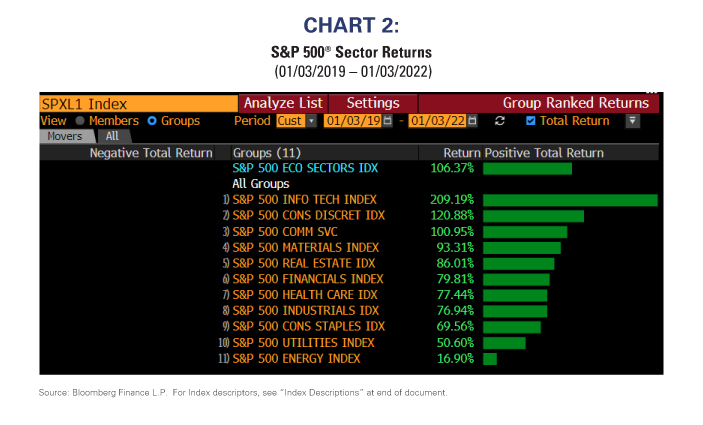

Charts 2 and 3 highlight the leadership changes. Chart 2 shows sector performance for the 3 years leading up to the market peak, whereas Chart 3 shows sector performance from the peak.

US inflation has hit 40-year highs and sector performance has been highlighting pro-inflation sectors such as Energy and Materials. Defensive sectors, which tend to follow later-cycle inflation-oriented sectors in a normal cyclical rotation, have also been among the leaders (See Chart 2).

However, the sectors that benefitted the most from secular disinflation and falling interest rates (Technology, Communications, and Consumer Discretionary) are the worst performing sectors since the volatility began.

Two recent past examples

Two recent past examples

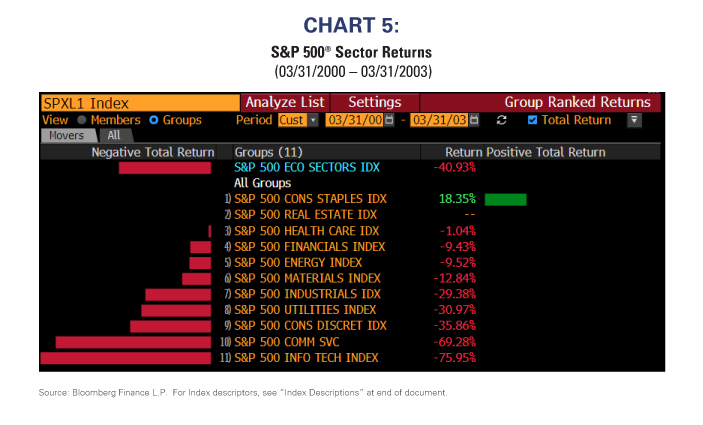

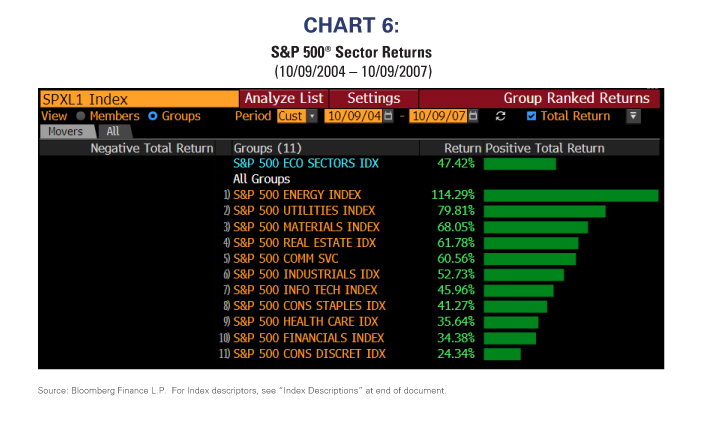

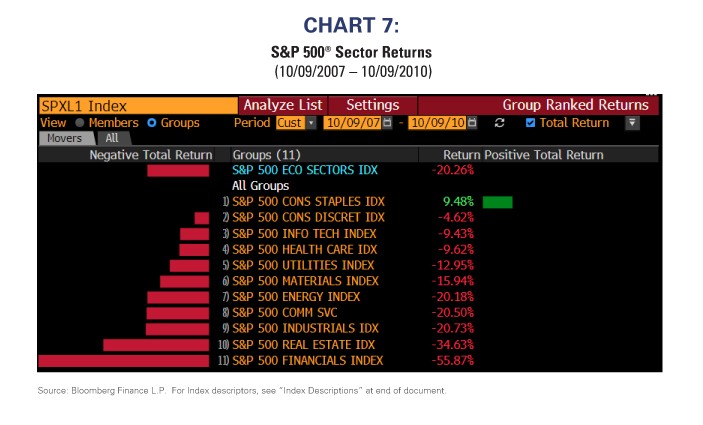

Some believe the current period of market volatility and changes in sector leadership are unique or temporary. Recent history shows neither to be true. Charts 4 and 5 look at sector performance during the 3 years prior to the peak in the Technology bubble and the 3 years subsequent. Charts 6 and 7 examine sector performance around the bursting of the financial bubble.

Don’t cling to the past. The economy is constantly changing and evolving.

Don’t cling to the past. The economy is constantly changing and evolving.

It’s natural for investors to fear the unknown, however, how much of an insurance policy should one pay for uncertainty and fear? So far in this cycle, it appears comfort costs about 25%, i.e., investors have given up about 25% return to hold on to old stories.

The US and global economies have always changed through time and continue to do so. It seems very unrealistic to assume one sector or market segment is appropriate for every economic environment. Long-duration equity segments such as Technology, innovation, disruption, and venture capital were the right themes for secular disinflation and falling interest rates, but other sectors seem better suited to the evolving global economy.

For more news, information, and strategy, visit the ETF Strategist Channel.