![]() By Michael Jones, RiverFront Investment Group

By Michael Jones, RiverFront Investment Group

In recent weeks President Trump rejected China’s package of trade concessions as inadequate. The president also pressed forward with proposed tariffs on China in addition to previous tariffs imposed upon Canada, Mexico and the European Union (EU). These actions increased the risk of a trade war and prompted a deterioration in market momentum and sentiment, in our view. As a result, we have further reduced portfolio risk levels despite strong earnings and an otherwise favorable investment environment (please see the July 3rd Weekly View for more details).

RiverFront portfolio risk levels are now roughly in line with our market benchmarks. We did not make more dramatic risk reductions because our tactical models suggest slightly better than 50/50 odds that the market will be higher over the next few months. This quantitative assessment confirms our judgment that the increased risk of trade war is partially counterbalanced by the still greater probability that we will see a successful conclusion to the current trade disputes, as shown in the scenario table below.

President Trump’s Negotiating Style Means Big Opportunities and Big Risks

President Trump’s negotiating approach with our trading partners has defied normal conventions of international diplomacy and negotiation strategy, just as his political campaign defied similar conventions in the political arena. When offered concessions without any strings attached, normal negotiating tactics call for taking what is offered. Taking a unilateral concession costs nothing and does not preclude pushing for further concessions in future negotiations. This typical approach to negotiations is why we, and most other observers, expected President Trump to accept the unilateral concessions China had offered. Accepting China’s concessions would have created an automatic “win” President Trump could tout and would not have precluded pushing for still more market opening moves.

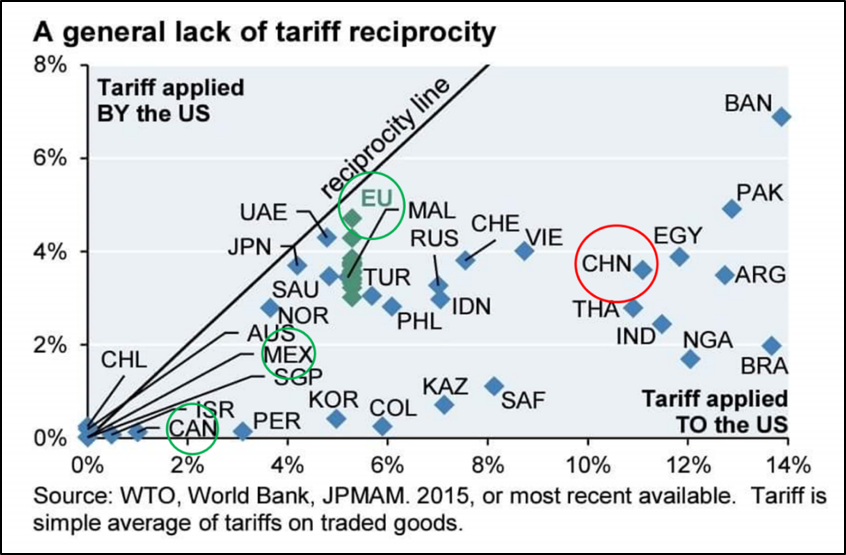

Similarly, traditional negotiating strategy would call for focusing on the biggest problems first and gathering allies in a unified effort to solve those problems. The adjacent chart from JP Morgan Asset Management shows relative tariff rates between our different trading counterparties prior to the recent round of “tit for tat” tariff increases. The chart shows that China (red circle) has historically applied much higher tariffs on US goods than the US applies to Chinese goods, and the extent of this disparity is shown by China’s distance from the “reciprocity line” (countries on or near the reciprocity line have tariffs roughly comparable to those of the US). By contrast, our NAFTA and EU trading partners (green circles) are relatively close to the reciprocity line and therefore have similar tariff rates as the US. Traditional negotiating tactics would suggest gathering these allies into a unified coalition to jointly attack China’s one-sided approach to trade. Instead, by imposing tariffs on our EU and NAFTA trading partners, President Trump has placed them in the opposition camp rather than a part of a unified coalition against China’s trade practices.

The Bull Case

The bullish scenario for President Trump’s unorthodox negotiating tactics is that this aggressive approach could be a necessary component of a successful negotiating strategy. From the time President Trump was elected, most market analysts, trade experts and diplomats have dismissed President Trump’s tough trade talk as “Art of the Deal” posturing. Accepting concessions that fall well short of his objectives or failing to move forward with threatened tariffs could reinforce the consensus view that he is not serious about his threatened trade war. President Trump cannot achieve sweeping changes in the global trading system unless he convinces his negotiating counterparties that he is not bluffing. The fact that foreign leaders and financial markets are starting to worry that he might be willing to ignite a trade war could be a necessary precondition to getting a positive resolution to these trade disputes.

An additional bullish consideration is that President Trump is seeking far more sweeping changes in the global trading system than was originally expected. With China, he is pushing for previously unthinkable changes in their “Made in China” initiative designed to assure Chinese dominance of high tech industries. He is demanding concrete and measurable improvements in US ability to access Chinese markets and greater protection from intellectual property theft. With Europe, he has proposed eliminating all tariffs between the US and the EU. This dramatic proposal was enthusiastically endorsed by the European auto industry. The current uncertainty and volatility gripping financial markets may be a necessary period of pain required to get the gain of a much-improved global trading system and a renewed bull market in global equities.

The Bear Case

President Trump’s political success depended upon defying conventional tactics and methods but his negotiation style, developed in a business career full of one on one negotiations, may not translate well to the more complex multi-lateral world of trade policy. By not accepting China’s offered concessions, President Trump missed an opportunity to secure concrete concessions and create goodwill and positive momentum that could lead to further negotiating breakthroughs. By attacking our traditional allies along with China, President Trump has allowed China to split the Western democracies and seek separate negotiated settlements rather than confront all their major export markets simultaneously. For example, during the week of July 1st, China dropped tariffs on EU and Japanese automobiles to 15% as a part of their package of unilateral concessions. Tariffs on US automobile exports, by contrast, were increased to 40%. China has gone so far as to approach the EU about a unified negotiating alliance against the US. Although the EU rejected this proposal, the fact that China felt such an alliance would even be possible illustrates how thoroughly Chinese leadership believes they have divided the interests of the US from the other Western democracies. Divided opposition could reduce the pressure on China to reach an agreement with the US and increase the odds of a trade war.

An additional concern is that President Trump seems indifferent to the political pressures faced by democratically elected officials in the EU, Mexico and Canada. His abrasive style and undiplomatic statements endear him to his supporters, but might force his overseas counterparts to take a harder line to avoid appearing “soft” to their own supporters in the face of US pressure.

The US economy is far less dependent upon trade than most of our trading partners, with only 12% of the US economy devoted to exports as compared to more than twice that level for China and the EU. However, the relative protection of the US economy may not extend to US equities. According to Ned Davis Research, about 50% of S&P 500 profits comes from overseas and these profits could be endangered in any trade war scenario. China’s large trade surplus means they will likely lose a “tit for tat” tariff war with the Trump administration, but the China operations of US companies may be more vulnerable to Chinese retaliation. Regulatory crackdowns and bureaucratic obstacles forced Yum Brands and Uber to sell their China operations to domestic competitors, and similar tactics could be deployed as weapons in a trade war with the US.

What We Think

President Trump’s unique communication and negotiating style are intended to create uncertainty about his ultimate goals. However, we believe his historic pattern has been to create maximum uncertainty and stress just prior to offering unexpected conciliatory gestures, such as accepting a face to face meeting with North Korean leader Kim Jung Un. We believe this pattern of behavior could be repeated in the current trade disputes, and his willingness to push things so hard and so far could result in more sweeping improvements to the global trading system than we originally expected.

If this view is correct, President Trump may still have work to do to convince his negotiating counterparts that they must make further concessions to avoid an all-out trade war. Assuming President Trump wants these issues resolved in time to benefit Republican candidates in the November elections, investors should prepare for more volatility and stress in the coming weeks as we enter the final innings of this process. So long as the S&P 500 holds above about 2600 and our tactical models remain in positive territory, we will see this volatility as an opportunity to get back to a more aggressive portfolio positioning with a higher equity weighting. Resolution of these disputes and improved access to the China market could catalyze another big upward movement in global equity markets, in our view.

Despite our cautious optimism, we acknowledge that President Trump’s negotiating style may prove ill-suited to complex, multi-party trade negotiations. His strongly worded tweets and public statements could backfire among our major trading partners and stoke political opposition to meeting US trade demands. We also worry that China is determined not to repeat what they see as Japan’s disastrous trade concessions in the 1980s. Chinese leadership believes that the series of market opening moves demanded by the Reagan administration to address Japan’s large trade surplus contributed to Japan’s long period of stagnation. There is a line China will not cross and if the Trump negotiating team pushes too hard a trade war could ensue. If the S&P 500 cannot hold 2600 or our tactical indicators deteriorate sharply, we will have to acknowledge our mistake and take further risk reduction actions in our portfolios.