Still defensive, for now

- Our Equity Model’s 6-month outlook for the S&P 500 has improved from Negative to Neutral.

- However, the Short-Term Risk model still gives a Sell signal, which dictates defensive positioning.

- Election uncertainty, lack of a stimulus package, and COVID all continue to weigh on the market.

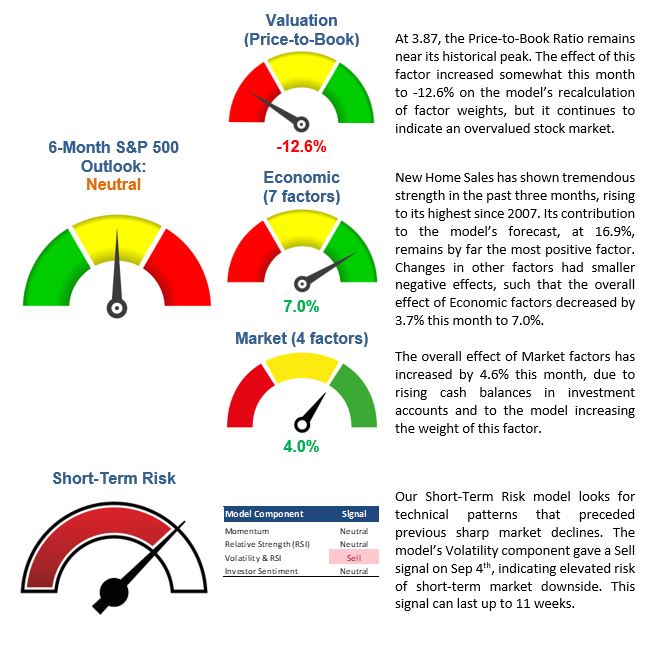

The significant positive shift in our fundamental Equity Model that I described in my previous article continues into October. The model’s 6-month outlook for the S&P 500 rose further, from Negative to now Neutral. The Economic component of the model has improved tremendously over the past two months and is now positive at 7% on strengthening in consumer sentiment and home sales. In addition, this month’s increase is explained by rising cash balances in investment accounts (see Market Outlook for details).

With the forecast moving to a range between -5% and 3%, the Equity Model has now shifted from Negative Fundamentals to Neutral Fundamentals (the middle vertical on the chart). This would dictate balanced positioning of our tactical portfolios – 60% stocks and 40% fixed income. However, our Short-Term Risk model continues to give a Sell signal. The two models work in concert: if the Risk model gives a Sell signal, we de-risk the portfolio completely. This is designed to reduce exposure to short-term market corrections. So, the Risk model must turn positive in order for us to get back into the market.

Here’s how I interpret the latest signals from our models. The fundamental Equity Model is suggesting a near-zero stock market return in six months. But a lot can happen in six months. The Short-Term Risk model indicates an elevated chance of short-term downside. The two models are not inconsistent: we could witness a short-term market correction in a matter of weeks, and then positive – even very strong – performance in six months.

Investors have focused recently only on stimulus negotiations. But a resurgence in COVID, flagging economic metrics, or shifts in the election chances could also trigger short-term volatility.

“We Want Stimulus!”

The Fed and Congress enacted three trillion dollars of stimulus earlier this year. Some of the money helped the unemployed and struggling businesses, and some went into stock trading and home buying, boosting those markets tremendously. Since the $600 weekly checks ended on Aug 31st, the S&P 500 has been flat. No wonder they all want more stimulus – the unemployed and wealthy investors alike. Negotiations between the Democrats and the GOP had been on-and-off but are now finally stalled. Treasury Secretary Mnuchin said yesterday that it will be “difficult” to agree before the election. As a result, the stimulus factor converged with the election factor.

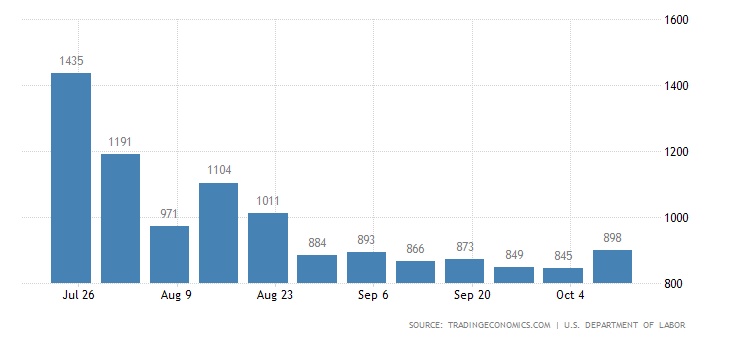

It’s not clear how well the economy can “walk on its own” without stimulus. Some metrics suggest that the stimulus effect is wearing off – for example, weekly jobless claims jumped unexpectedly to 898,000:

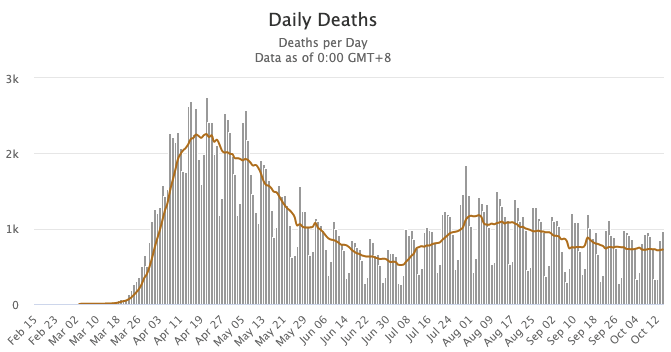

Then, there’s the fear that COVID will rise this fall. While US deaths have been falling gradually since their August peak (see chart below), infections have risen in some areas. Of course, more testing in part drives the rise in cases, many of which have mild or no symptoms – but fear is still running high. Deaths lag cases by 2-3 weeks, and if they begin to rise, it could prompt renewed lockdown measures. Renewed restrictions were announced yesterday in Paris and other parts of Europe.

Will the Election Cause Volatility?

The elephant in the room is the upcoming presidential election. The two sides’ approaches to tax and economic policy might be the most diametrically opposite in decades. While we’re not political experts, let me outline the expected effect of each candidate on the market the way I see it.

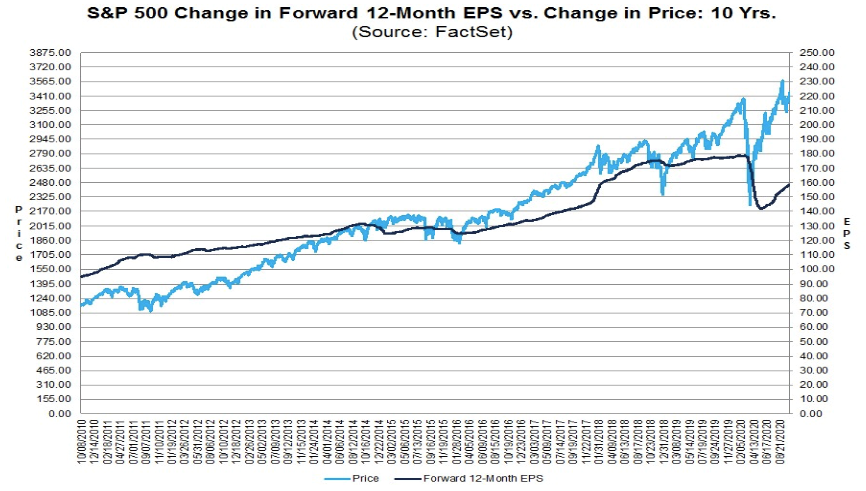

Historical market performance shows that the S&P 500 rose by around 30% from Nov-2016 to Dec-2017 – first reflecting the effect of Donald Trump’s unexpected win, then his pro-growth policies, and finally his tax cut. Also, earnings are an important long-term market driver. Most of the S&P’s earnings rise in recent years occurred in 2018 due to the corporate tax cut (see chart above) – absent that, earnings rose only slightly from 2017.

On the other hand, the Democratic side has fiercely criticized the president’s drive to reopen the country, which suggests that they would likely reimpose some COVID-related restrictions. Regarding taxes, Joe Biden indicated that he would reverse President Trump’s tax cuts, and separately indicated that he would raise taxes on those earning over $400,000 a year. It’s not clear if the two are overlapping or separate. It suggests to me that they would reverse the 2017 corporate and individual tax cuts and in addition, would raise taxes on high earners. This is important for the stock market because high earners are investors. The Democratic side would also likely reverse the short-term capital gains tax from 21% back to the filer’s income-tax rate (the highest would be 39.6%) – also important to the market.

Clearly, President Trump has been a positive “factor” for the stock market, and Biden would be very negative.

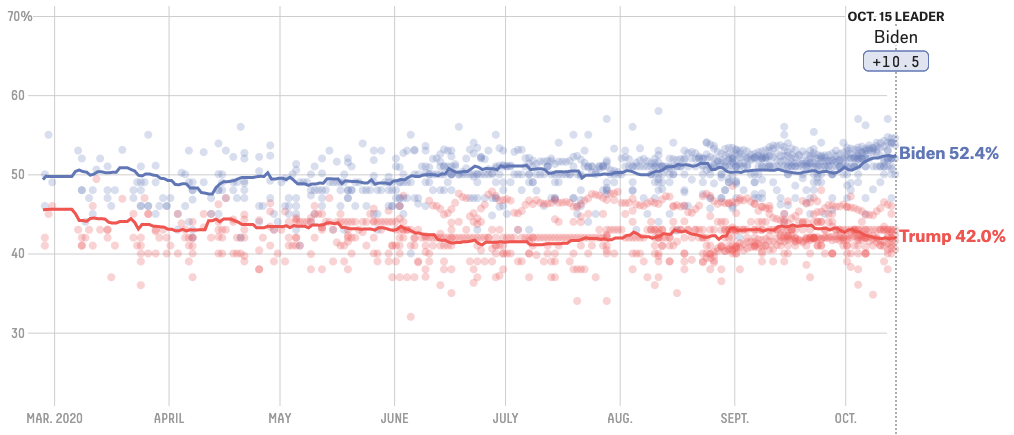

General Election Poll Averages

Poll averages show Joe Biden leading President Trump by over 10%. So, we have an apparent contradiction between the market near its all-time high and a high chance of a Biden win. One explanation is that investors are completely ignoring polls because they are wrong. Most polls have inherent biases, depend heavily on sampling, and were very wrong in 2016. The Democracy Institute, which correctly predicted both the 2016 general election and Brexit, shows Trump slightly ahead.

But given the size of the gap, it still shocks me that the market has not reflected this high chance of Biden’s win. If such a wide gap persists as we approach November 3rd, investors might reflect it by selling stocks. If it narrows somewhat, investors might get more concerned about an undecided or “unprocessed” election. Both circumstances could cause short-term market downside leading into the election.

Market Outlook

The outlook for the S&P 500 by our fundamentals-based statistical model improved again this month. On the back of economic Improvements over the past two months, the positive change this month was driven by rising cash balances in investment accounts. The outlook has now shifted to a Neutral range between -5% and 3%. However, our Short-Term Risk model remains in a Sell position, indicating elevated risk of short-term market downside, which dictates continued defensive allocation.

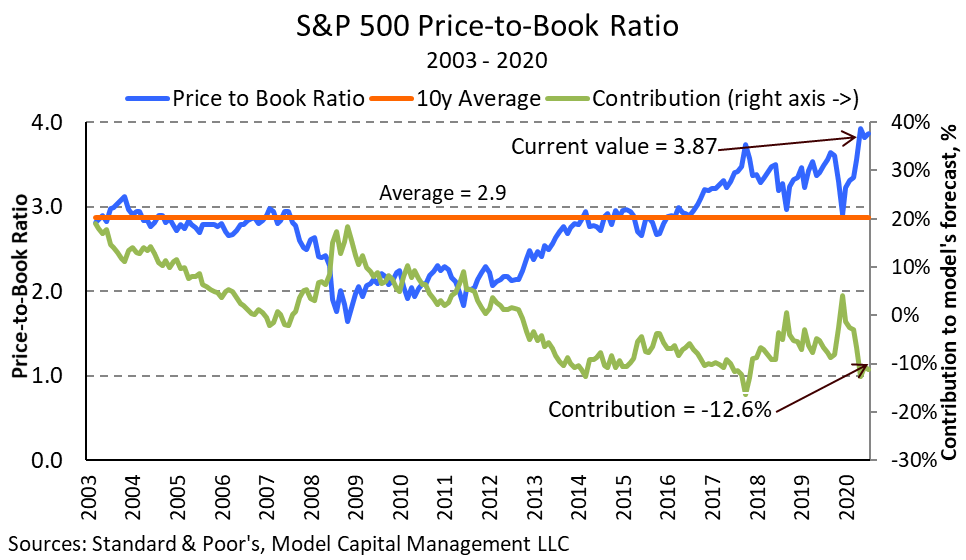

Some of the Equity Model’s most negative and positive factors are shown below in historical context (assuming their current weights). The S&P 500 Price-to-Book Ratio decreased to 3.87 but remains near its highest level since January 2001. The contribution of this factor rose to -12.6% on the model’s adjustments in factor weights, but still points to an overvalued market.

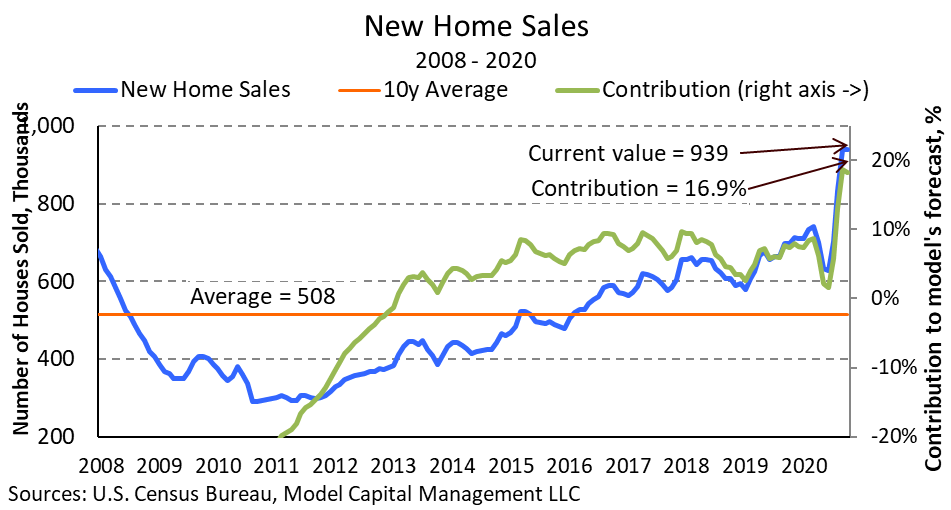

New Home Sales has shown tremendous strength over the past three months on historically low mortgage rates. The effect of this factor, at 16.9%, continues to be the most positive in the model.

About Model Capital Management LLC

Model Capital Management LLC (“MCM”) is an independent SEC-registered investment advisor, and is based in Wellesley, Massachusetts. Utilizing its fundamental, forward-looking approach to asset allocation, MCM provides asset management services that help other advisors implement its dynamic investment strategies designed to reduce significant downside risk. MCM is available to advisors on AssetMark, Envestnet, and other SMA/UMA platforms, but is not affiliated with those firms.

Notices and Disclosures

- This research document and all of the information contained in it (“MCM Research”) is the property of MCM. The Information set out in this communication is subject to copyright and may not be reproduced or disseminated, in whole or in part, without the express written permission of MCM. The trademarks and service marks contained in this document are the property of their respective owners. Third-party data providers make no warranties or representations relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damages relating to such data.

- MCM does not provide individually tailored investment advice. MCM Research has been prepared without regard to the circumstances and objectives of those who receive it. MCM recommends that investors independently evaluate particular investments and strategies, and encourages investors to seek the advice of an investment adviser. The appropriateness of an investment or strategy will depend on an investor’s circumstances and objectives. The securities, instruments, or strategies discussed in MCM Research may not be suitable for all investors, and certain investors may not be eligible to purchase or participate in some or all of them. The value of and income from your investments may vary because of changes in securities/instruments prices, market indexes, or other factors. Past performance is not a guarantee of future performance, and not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized.

- MCM Research is not an offer to buy or sell or the solicitation of an offer to buy or sell any security/instrument or to participate in any particular trading strategy. MCM does not analyze, follow, research or recommend individual companies or their securities. Employees of MCM may have investments in securities/instruments or derivatives of securities/instruments based on broad market indices included in MCM Research.

- MCM is not acting as a municipal advisor and the opinions or views contained in MCM Research are not intended to be, and do not constitute, advice within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

- MCM Research is based on public information. MCM makes every effort to use reliable, comprehensive information, but we make no representation that it is accurate or complete. We have no obligation to tell you when opinions or information in MCM Research change.

- MCM DOES NOT MAKE ANY EXPRESS OR IMPLIED WARRANTIES OR REPRESENTATIONS WITH RESPECT TO THIS MCM RESEARCH (OR THE RESULTS TO BE OBTAINED BY THE USE THEREOF), AND TO THE MAXIMUM EXTENT PERMITTED BY LAW, MCM HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES (INCLUDING, WITHOUT LIMITATION, ANY IMPLIED WARRANTIES OF ORIGINALITY, ACCURACY, TIMELINESS, NON-INFRINGEMENT, COMPLETENESS, MERCHANTABILITY AND/OR FITNESS FOR A PARTICULAR PURPOSE).

- “Model Return Forecast” for 6-month S&P 500 return is MCM’s measure of attractiveness of the U.S. equity market obtained by applying MCM’s proprietary statistical algorithm and historical data, but is not promissory, and, by itself, does not constitute an investment recommendation. Model Return Forecasts were calculated and applied by MCM to its research and investment process in real time beginning from 2012. For periods prior to Jan 2012, the results are “back-tested,” i.e., obtained by retroactively applying MCM’s algorithm and historical data available in Jan 2012 or thereafter. Source for the S&P 500 actual returns: S&P Dow Jones.

- Index returns referenced in MCM Research, if any, are gross of any advisory fees, fund management fees, and trading expenses. Fund or ETF returns referenced, if any, are gross of advisory fees and trading expenses. Returns will be reduced by fees and expenses incurred.