Previously, our biggest concern for the outlook of the economy had been that the U.S. Federal Reserve (Fed) would keep short-term interest rates too high for too long. With Chairman Powell’s recent press conference and the release of the Fed’s “dot plot” at the conclusion of the latest Fed meeting, the Fed appears to have shifted to a more dovish stance. Though uncertainties and risks remain, we think the Powell Pivot is good news for the economy and increases the likelihood of continued economic growth.

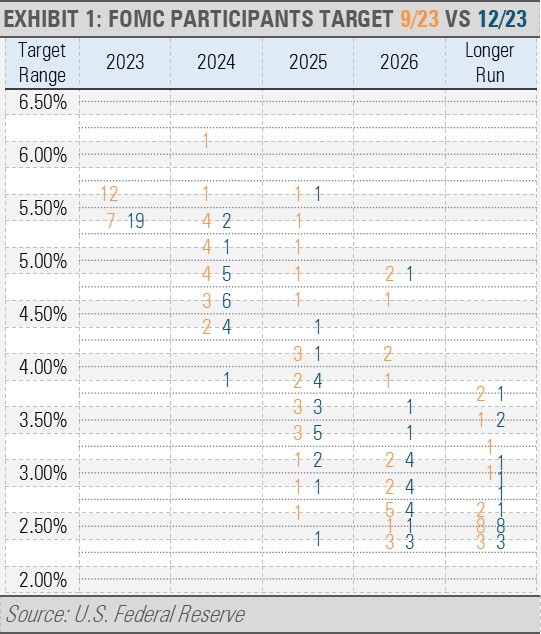

While Fed policy remains firmly in restrictive territory, we applaud this more dovish stance. The Fed’s latest “dot plot” shows a shift from “higher for longer” to opening the door to more significant rate cuts in 2024. The Fed now predicts rate cuts totaling 75bps (0.75%) while the market is pricing in a faster reduction.

We now shift the focus to what caused this change in the Fed’s outlook. According to Powell, the biggest change impacting the Fed’s forecast is the reduction in inflationary pressures over the last few months. In addition, Powell noted the more balanced labor market conditions as well as slowing economic growth in the current quarter. Furthermore, Powell said that the Fed wants to begin cutting rates before inflation declines to their 2% target. Reducing interest rates before inflation falls to the Fed’s 2% target can help reduce the risk of keeping rates too high for too long and causing unnecessary economic damage.

In addition, Powell affirmed that the future for economic growth and inflation are uncertain, and that the Fed would act on the incoming data. This gives the Fed flexibility to adjust policy in real time. However, it seems that the Fed has pivoted to a more dovish stance with a clear bias towards rate cuts.

We think that is good news for the economy. The financial markets clearly like this pivot with stocks and bonds rallying on lower interest rate expectations. While our economic outlook remains cautious, the path to a soft landing has become broader with the reduced risk of the Fed remaining too tight for too long.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.