By Rod Smyth, Chairman of the Board of Directors

SUMMARY

- Interest rates are at historic lows…

- In our view, this presents tough choices, which are best handled by an active manager than a passive index.

Few Good Choices in Fixed Income Make Active Management Imperative, in Our View

When playing cards, you have the excitement of opening your hand to see what kind of cards you have been dealt. Sometimes you have Aces and Kings, and sometimes you realize quickly that you have a tough hand, but that is the hand you must play. The great card players know how to make the best of a bad hand.

Today’s bond investor has a ‘tough hand’ with few good choices, in our view:

Government Bonds: Yields on Government bonds are low, and below the rate of inflation.

Source: US Treasury. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

The table above shows the yield investors receive for lending money to the US Treasury from one month all the way out to 30 years. So, if you write a check to Uncle Sam for a 10-year bond, you will get your money back in 10 years at a 1.66% rate of interest, hardly an attractive choice when the Federal Reserve’s target for inflation is around 2%. As the chart below shows, this is very low relative to the last 20 years, illustrating what a tough hand investors must play.

10-year Yields at Very Low Levels

Source: Refinitiv Datastream, RiverFront. Data as of 10.21.2021. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Playing a tough hand requires extra work, unlike a good hand where the hand essentially plays itself, in our view. An active manager builds a portfolio that deviates slightly (or significantly) from the broad market as represented by the most popular index like the Bloomberg aggregate bond index (defined below). In the current environment, for RiverFront, active management describes the ‘extra work’ a tough hand requires. The alternative to an active strategy is passively investing in an index.

Index Construction: If investors knew how bond indexes are constructed; they might be surprised. The way bond indexes are constructed, seems arbitrary, in our view. A bond index such as the Bloomberg US Aggregate Bond is based on the amount of bonds outstanding from different issuers. The current weightings are approximately 40% Government-Related, 29% Corporates, and 31% Mortgages. In our view, the amount of debt issued is not a reflection of how attractive the entity is to own. We would argue that entities with the most debt are often riskier and because they are the biggest part of an index, this risk should be managed. There is a time for owning more risky issuers and indexes, but we think it should be an active decision.

In our view, there are many ways an active manager can play a tough hand, which fall into two broad categories: 1. Selection and 2. Maturities (longer and shorter).

Selection:

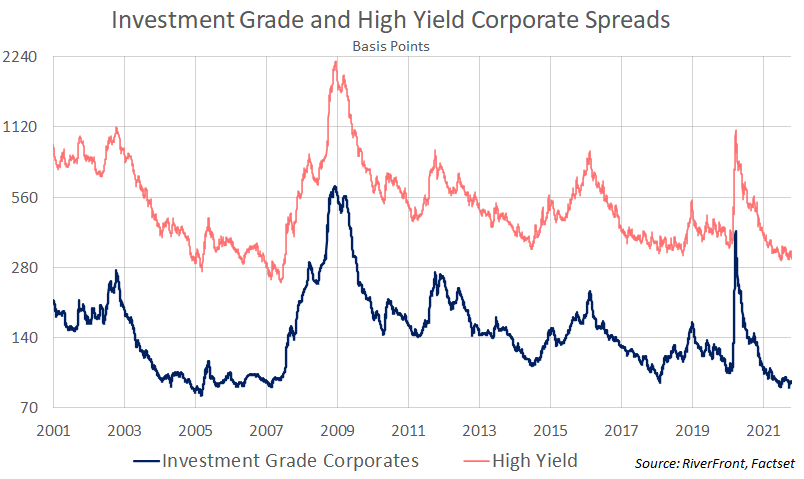

Corporate Bonds: Opportunities for Active Managers: Bonds issued by companies nearly always pay higher interest rates than those issued by the government since there is always the risk of default. The more investors perceive a risk of default, the higher the yield investors require. Those with the highest default risk are known as ‘junk’ bonds; the others are called ‘investment grade’ bonds. During times of economic weakness or other times when default risk rises, the spread between yields on corporate bonds and Treasury bonds widens (see chart below). This often coincides with stock market declines so investors should be aware that corporate bonds offer less protection than Treasury bonds during these times.

The chart below shows the spread over Treasuries on both investment grade and junk bonds. You can see how spreads widened in 2008/9 during the ‘Great Recession’ and in the first quarter of 2020 due to COVID-19. For an active manager, these present the opportunity to buy corporate bonds at attractive yields, but the timing of purchases is important and another active decision, in our view. Continuing the theme of a tough hand, current spreads are at historically low levels, meaning you are no longer getting as much extra yield for your extra risk. Therefore, especially now, we believe owning corporate bonds is something that should be managed actively.

Spreads at Historic Lows:

Source: RiverFront, Factset. Data as of 10.21.2021. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Mortgage Bonds: Another alternative to Treasury bonds. Investors can buy pools of mortgages, collecting the interest payments paid by homeowners. They tend to offer yields somewhere between Treasuries and corporates. RiverFront prefers mortgages when rates are stable because the payment of mortgages can be affected by the interest rate environment.

RiverFront’s Strategy: We believe that one of the best ways to outperform broad bond indexes over the long term is to own bonds with higher yields such as corporates and mortgages. Investors should recognize that additional yield comes with additional risk. We believe this requires considerable experience analyzing the issuers and thus recommend an active approach. Currently, RiverFront’s bond portfolios favor corporate bonds since we are optimistic about the outlook for the economy.

Duration/Maturity

The importance of knowing a bond’s maturity and duration. Different maturities offer different risk/reward profiles. Selecting the timeframe of maturities in a bond portfolio is another important decision, and one we believe should be made deliberately. To measure this risk there is a calculation called ‘duration’. Duration is the sensitivity of the price of the bond to a change in interest rates. In general, the higher the duration, the more a price will drop as interest rates rise and vice versa. For example, if rates were to rise 1% a bond with a 10-year duration would likely lose 10% of its value.

Durations are closely related to maturities and the longer the duration, the greater the bond price movement. Thus, bonds with longer maturities tend to be more volatile than similar bonds with shorter ones. The Bloomberg US Bond index currently has a duration of roughly 6.5 years.

RiverFront’s Strategy: Since we expect interest rates to increase over the long term, our fixed income portfolios have durations shorter than the Bloomberg index, making them less susceptible to rising rates.

In Summary: Investors face tough choices in today’s low interest rate environment. As a result, we strongly recommend having an expert to make judgments regarding those choices, rather than investing passively in an index. For investors in the Distribute and Sustain phases of their investment journey this is especially important, in our view.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Mortgage-backed securities are subject to prepayment and extension risk ; as such, they react differently to changes in interest rates than other bonds. Small movements in interest rates may quickly and significantly reduce the value of certain mortgage backed securities.

Index Definitions:

Bloomberg US Aggregate Bond Index TR USD (Fixed Income Investment Grade) is an unmanaged index that covers the investment grade fixed rate bond market with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. The issues must be rated investment grade, be publicly traded, and meet certain maturity and issue size requirements.

For each outcome category (accumulate, sustain and distribute) RiverFront’s portfolio management team has assigned one or more RiverFront product(s) based on their assessment of the product’s investment objective as it relates to a typical client’s return and risk objectives when seeking investment outcomes of accumulating wealth, sustaining wealth and distributing wealth. The team has also designated RiverFront product alternatives for those clients looking to take more or less risk with the outcome category. The ‘more aggressive’ (or more risk) alternatives will generally have greater equity and international exposure as well as longer time horizon targets, while those designated as ‘more conservative’ (or less risk) will have fewer equities, a lower exposure to international and shorter time horizon targets. Since the risk assessments are dependent on the outcome category selected, RiverFront products may fall in multiple categories. For example, the Advantage Global Allocation portfolio, may fall under ‘more aggressive’ to those with the outcome of ‘sustain’, but ‘more conservative’ for investors interested in ‘accumulation’. All investments carry a risk of loss and there is no guarantee that an investment product or strategy will meet its stated objectives.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1891323