THE S&P 500 IS UP MORE THAN 40% SINCE MARCH 23RD, DESPITE THE NEGATIVE HEADLINES

By Riverfront Investment Group

Some investors are understandably baffled by the 40% rally in the S&P 500 since the market low on March 23rd. Against the tragic and disturbing backdrop of the COVID-19 pandemic, record levels of unemployment, and now the protests and social unrest that has swept the country, how is it possible that stocks have risen so much? This week, we would like to focus on this question and try to offer reasons for the market’s gains. We will also explain why we have been adding equities back into our portfolios since April 9th and added some more last week.

When less bad is good: In our experience, markets usually react to the rate of change in the data rather than the level. We expect economic and earnings data to continue to be very bad in absolute terms. However, the message from the stock market is that investors expect the data to improve now that the lock-down has ended. A good example of this was last week’s employment report which showed that unemployment is still very high at 13%, but there were 2.5 million non-farm payroll gains and the unemployment rate fell from last month.

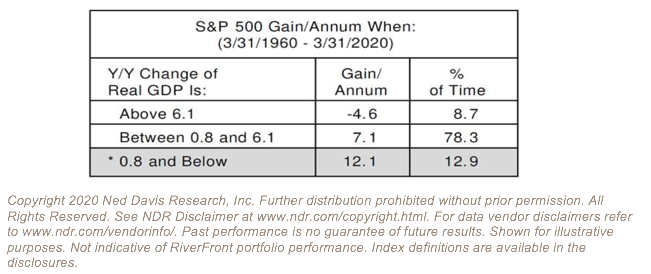

What is happening to stocks is consistent with other recessions and the Great Recession of 2008/09. The S&P 500 bottomed in March of 2009 and rose every month for the next 6 months, recovering 50% of its losses by the end of the year. This happened well in advance of any meaningful improvement in earnings, but rather in the expectation that the improvement would follow… which it did. The following table from Ned Davis Research shows that the S&P 500 surprisingly has its best returns when economic growth is low (below 0.5%). We believe this is because stocks typically fall dramatically as the economy slows, but also recovers quickly as investors anticipate improvement.

Process Over Prediction: Over the last month we have repeated our mantra of ‘process over prediction’ several times. This means we believe that an unemotional, disciplined process for managing risks and opportunities is more effective than anchoring on any one forecast. As Yogi Berra said, “It’s tough to make predictions, especially about the future.” Considering the current environment, we are looking at the forecasts with caution as they are highly dependent on the potential occurrence of a second wave of the virus and how quickly consumers return to more normal behavior. Based on the rally, stock investors are currently taking an optimistic view. A second wave would likely cause the data to deteriorate again, raise the level of uncertainty and increase expectations of the length of the recession, all likely resulting in the stock market giving back some of its gains.

Due to the difficulty of forecasting, especially since what we are experiencing is unprecedented, we are continuing to focus on process, acknowledging the wisdom of crowds. Since the market reflects the summation of collective insights from investors around the world, it also acts as the final arbiter of news. Our “Don’t fight the trend” rule is the recognition of this.

In our view, the rally above 2950 on the S&P 500 was significant, even though the quickness and magnitude of the breakout was unexpected by many financial professionals, including our investment team. We believe the recent strength in the stock market highlights that most investors believe the reopening of the economy will have a larger positive impact on stocks than the potential headwinds caused by the recent protests and riots. Therefore, the combination of a humble approach and disciplined process has encouraged us to add back equity risk, even when it feels uncomfortable and we are buying as prices rise.

The Pessimistic Trap: In times of crises, many investors fall into the trap of extrapolating the dire situation far into the future. In fact, most humans are genetically wired to think this way. There are many studies to suggest that pessimism is more tempting than optimism. As psychologist Daniel Kahneman pointed out, “organisms that treat threats as more urgent than opportunities have a better chance to survive and reproduce.”

Many times, pessimistic thinking blocks out creative ideas and solutions. For example, while there is understandable fear of a rise in COVID-19 cases due to the protest gatherings, if we don’t see a wave of virus cases in the next few weeks, it might suggest the worst of the pandemic is behind us. The policy response to an economic shock is also critical to how markets behave. Just as the pandemic has been unprecedented in modern times, so has the size of the global coordinated policy mix of fiscal and monetary stimulus. The pessimists will point to a growing and potentially unsustainable budget deficit. However, the optimistic view is that all this money will have to flow somewhere, and it could support asset prices initially and then the economy. In other words, risk takers will be rewarded while savers are punished by extremely low interest rates and the risk of inflation over time, in our view.

As an investor, this type of optimism can be extremely uncomfortable. As financial columnist Morgan Housel points out, “In investing, a bull sounds like a reckless cheerleader, while a bear sounds like a sharp mind who has dug past the headlines.” However, history suggests that long-term optimistic thinking (with regards to the stock market) is a much more profitable exercise. According to data from Ned Davis Research, the S&P 500 has posted positive total return in 79% of calendar years from 1972-2019, averaging roughly 12% return per year over that time frame.

The reality is that we are all operating with incomplete and imperfect information. This, combined with the human tendency to focus on the pessimistic outcomes, can lead to suboptimal investment decisions, especially when relying on forecasts instead of a disciplined process.

Working with a trusted advisor can help navigate emotionally charged times like this: We believe that one of the most important pieces of advice we can offer investors is to get some professional help. The process of investing can trigger all sorts of emotions for individuals, especially when headline risks surrounding global pandemics, racial tensions, and national debt are involved. For these reasons, we believe its valuable to get an unbiased opinion from an advisor that can focus on financial goals. With the proper financial plan, many times the best portfolio action in a time of crisis is to do nothing. However, our human nature makes that type of inaction extremely difficult, especially without the help of a professional.

Bottom Line: The pandemic and the social unrest happening all over the country have caused emotions to become highly charged, and understandably so. We agree that these are uncertain and trying times for Americans and for the world. However, we believe that the best investment decisions are made when investors unemotionally weigh all the information and focus on the news that is most likely to have meaningful investment implications. Beneath the unsettling headlines, the burgeoning reopening of the economy in the US and Europe is a logical economic catalyst for stock market strength, in our opinion. For investors, we believe the final arbiter of news is the market itself and thus far the optimists are prevailing. So even though there are many risks on the horizon, our process incorporates the message of the markets and thus has been gradually adding to stocks since early April. As we wait for additional clarity and ultimate resolution of many of today’s headlines, we will stay vigilant, and will continue to adjust our portfolios accordingly.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

You cannot invest directly in an index

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Definitions: Don’t Fight the Fed – ‘Supportive’ means the Fed’s monetary policy regarding inflation and employment is in what we believe based on our analysis to be the investors’ best interest; ‘Against’ means the Fed’s monetary policy, in our view, is going against the investors’ best interest; ‘Neutral’ means the Fed’s monetary policy is neither supportive or against the investors’ best interest in our view. Don’t Fight the Trend – Terms correlate to the 200-day moving average as it relates to the equity indexes: ‘Positive’ means that the trend is rising, ‘Flat’ means the trend is flat, ‘Negative’ means the trend is falling. Beware the Crowd at Extremes – Terms correlate to the NDR Crowd Sentiment Poll and its measurement of Extreme Optimism (Bearish), Neutral, or Extreme Pessimism (Bullish).

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1209291