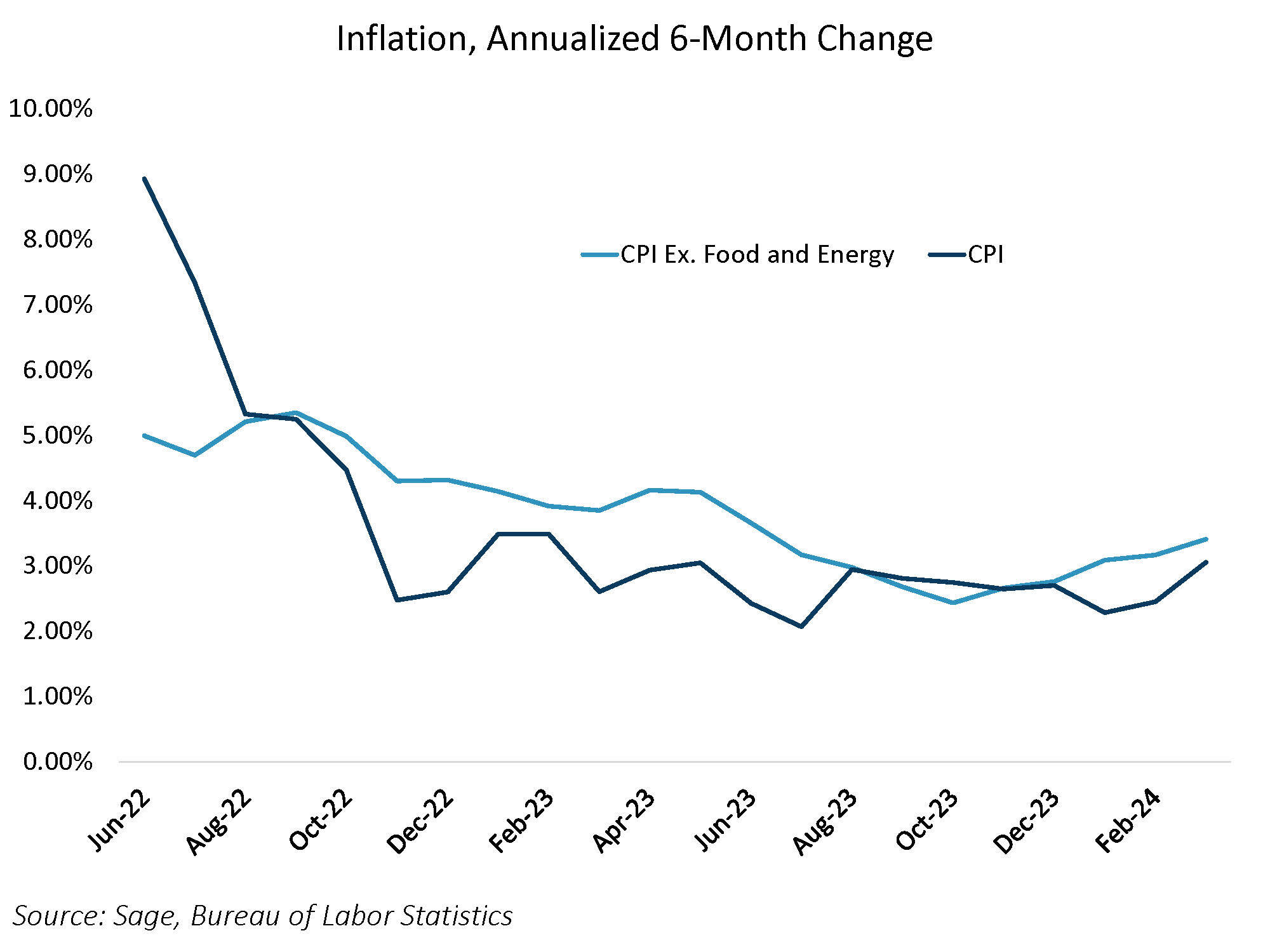

On Wednesday, the FOMC will release its May policy statement, which will not contain any accompanying “Fed dots” or economic projections, and nearly all market participants, us included, are expecting no change in the Fed policy rate at this meeting. However, given the inflation trend since the last meeting, the FOMC and Fed Chair Jerome Powell will likely give a nod to the lack of progress on inflation, which on balance will be a more hawkish stance versus the March meeting.

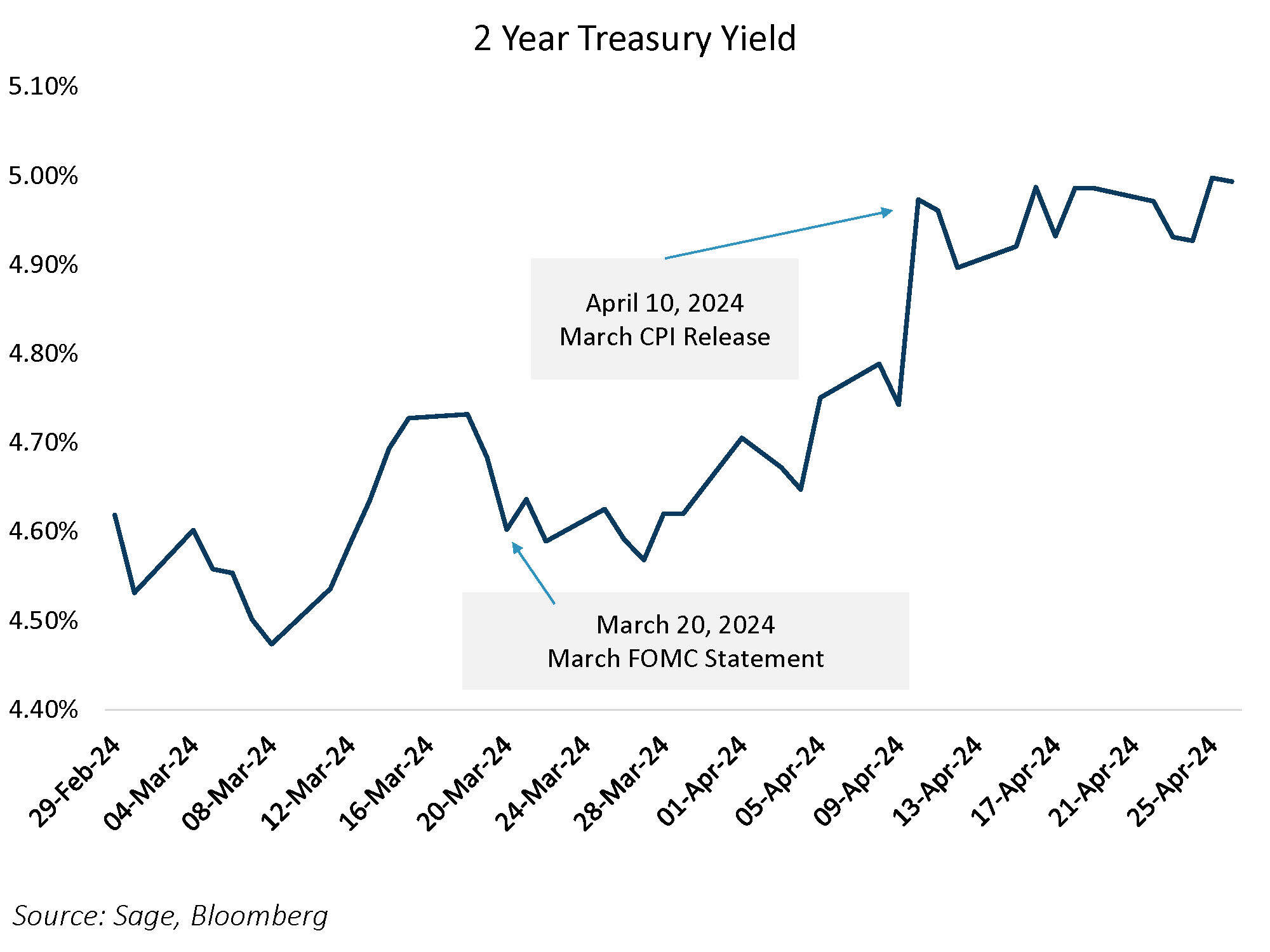

Since the last FOMC meeting in March, the 2-year Treasury yield rose by 40 basis points, and the 10-year Treasury yield rose by 19 basis points as the curve “bear flattened” to account for the resilient inflation picture. Indeed, much of the move happened on the day of the March CPI print release, when the 2-year and 10-year Treasury yields rose by 23 and 18 basis points, respectively.

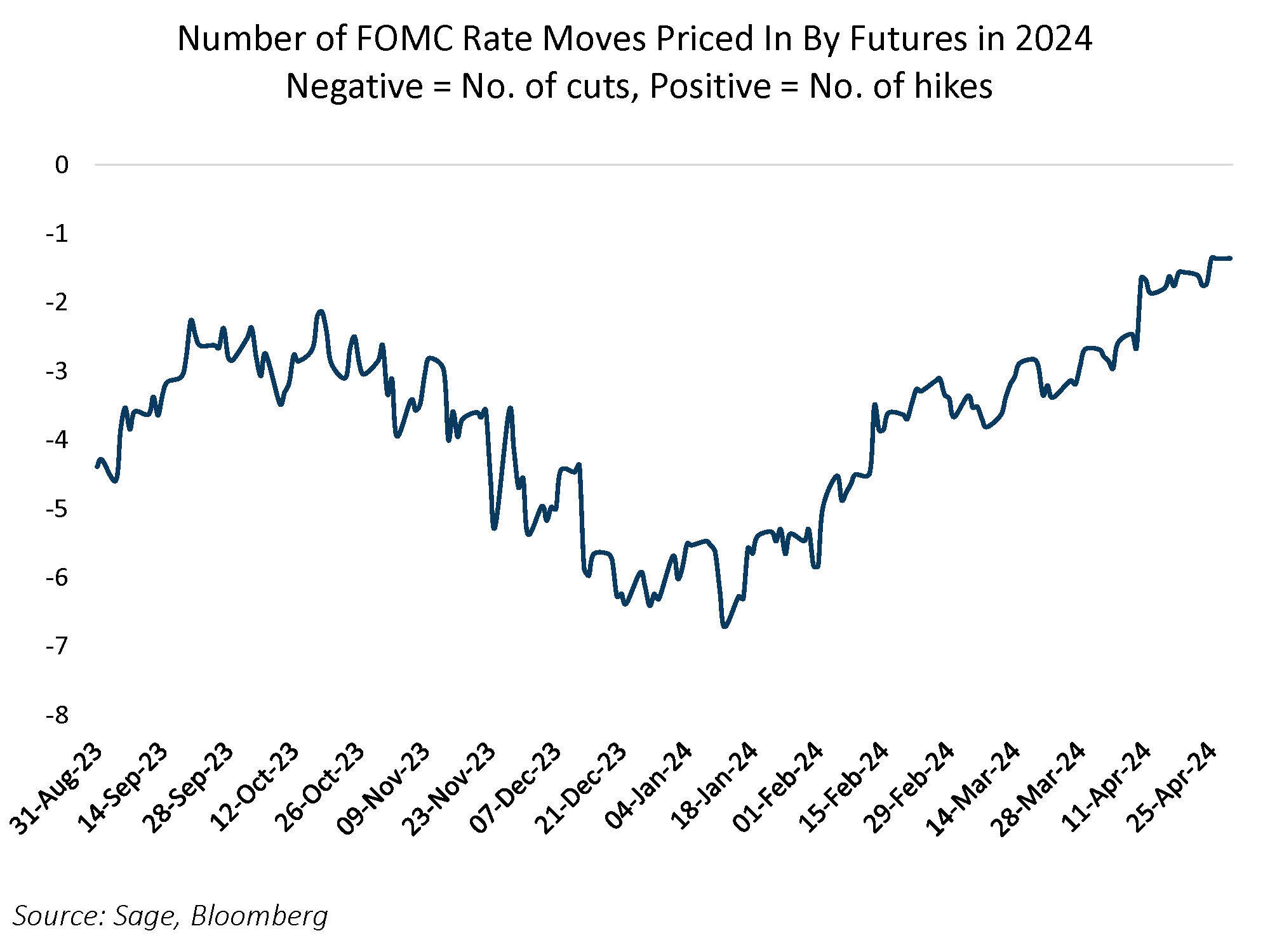

Markets are largely discounting a hawkish Fed stance at this juncture. As of April 26th, there is only one interest rate cut fully priced for 2024, beginning in June. As of now, strong inflation data has resulted in continued delays for the first rate cut, rather than a rate hike. We believe that through the balance of the year, there is scope for inflation to disappoint versus expectations. Combined with the market’s pricing (or lack thereof) of interest rate cuts for this year, as well as the higher inflation that the FOMC will tolerate, we believe the risk is to the downside in rates.

At this week’s meeting, we also expect an announcement about the slowing of the Fed’s balance sheet runoff. In the March FOMC meeting minutes released this month, the FOMC stated: “In light of the uncertainty regarding the level of reserves consistent with operating in an ample-reserves regime, slowing the pace of balance sheet runoff sooner rather than later would help facilitate a smooth transition from abundant to ample reserve balances. Slower runoff would give the Committee more time to assess market conditions as the balance sheet continues to shrink.” We wrote about the rationale for this decision in January.

While the Fed potentially alters its demand for Treasuries, the Treasury will announce the supply picture for Treasuries over the next quarter at its Quarterly Refunding Announcement (QRA) this week. The increase in coupon treasury supply (in lieu of a decrease in T-bill issuance) has contributed to the increase in term premium this year. In its January 31st statement, the Treasury set expectations for future issuance by stating: “Based on current projected borrowing needs, the Treasury does not anticipate needing to make any further increases in nominal coupon or FRN auction sizes, beyond those being announced today, for at least the next several quarters.”

A deviation from this statement could have a large impact on financial markets. Increasing issuance could become a concern for fiscal sustainability, similar to the 3Q 2023. However, given healthy tax receipts during April and the Treasury’s sensitivity to market disruptions, as well as the tone of its last two Quarterly Refunding Announcements, we expect Treasury Secretary Janet Yellen and the Treasury to err on the lower side of issuance.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.