By Chris Konstantinos, CFA, Director of Investments, Chief Investment Strategist

SUMMARY

- We believe inflation will peak in 2022.

- We believe Federal Reserve policy will remain supportive of stocks.

- Bonds’ real risk-adjusted return potential remains unattractive, in our view.

Every year around this time, the RiverFront Investment Team looks to communicate our thoughts for the coming year. As a teaser for our 2022 Outlook release in mid-December, I sat down with Global Fixed Income Co-Chief Investment Officer (CIO) Kevin Nicholson to discuss some of the most important questions facing income investors as we move towards the new year.

Some of the topics we covered include the direction of inflation and Federal Reserve policy, favorite and least favorite areas of the global bond market, contagion risks facing investors, just how ‘risk-free’ the risk-free rate really is… and importantly, the challenges facing income investors in a ‘low rates forever’ environment. Here is a transcript of that interview, edited for clarity.

Chris Konstantinos: Kevin, you’ve been one of our most consistent voices in ’21 in stating that the high inflation we’ve been seeing is likely to moderate next year. Given some of the big recent headline inflation numbers, do you still feel that way? Why or why not?

Kevin Nicholson: We believe inflation will peak in the first quarter of 2022 and then gradually return to a more normal level, likely around 2%, over the next 12 to 18 months. Currently, we are in a ‘show-and-prove’ cycle, where companies must show that they have pricing power and prove that they can grow earnings during a supply constrained environment. Thus far, the companies that have been ‘showing and proving’ have consisted of the large-cap S&P 500 companies. However, the ability to pass cost increases along to customers works only until they can no longer afford the item or find a substitute. So far, markets are taking inflation in stride because consumer net wealth continues to rise. In addition, supply chain bottlenecks may be alleviated by a fully re-opened economy where consumers can shift their spending away from goods and toward services. We recognize that market-based inflation expectations have moved up recently, and if this continues it could dampen equity market returns in 2022.

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

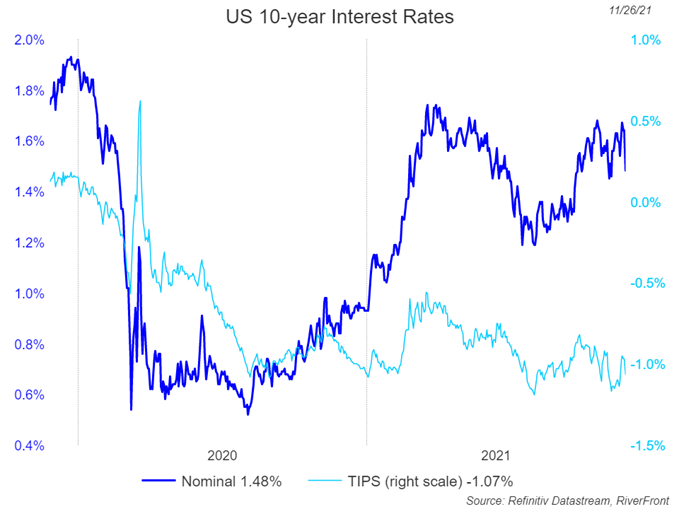

Chris Konstantinos: 2021 thus far has been a difficult time to own ‘risk-free’ paper, with the US 10-year treasury posting a negative total return for the first time in years. Considering that and the above question, what is our baseline forecast for the range of the US-10 year for 2022? What are your bull and bear case scenarios?

Kevin Nicholson:

- Baseline forecast for 10-year is approximately 2%, above recent levels (see chart).

- Bear case scenario for the 10-year: 2 – 2.50%, if inflation remains elevated and real yields stay negative.

- Bull case scenario for the 10-year: 1.50 – 2%, if inflation rolls over and returns to a more normal 2 to 2.5% range.

Chris Konstantinos: For credit markets, what are your favorite areas for total return in ’22? Areas to avoid?

Kevin Nicholson: High yield and possibly bank loans would be areas of interest looking for total return in 2022. We anticipate most of the return to come from income and do not expect much, if any, price appreciation.

- We are less attracted to traditional fixed income assets such as agencies and mortgages.

Chris Konstantinos: Talk about how the complexion of the Fed may change as we head into the new year. Do you see any risks to our house view that the Fed has little choice but to remain dovish?

Kevin Nicholson: Heading into the new year, the Fed may take on a more dovish tone as President Biden has at least 3 seats to fill on the FOMC (Federal Open Market Committee) and is expected to fill those seats with less hawkish governors than those being replaced. However, the Fed is becoming less accommodative as it tapers bond purchases by $15 billion per month through June 2022. With the reappointment of Fed Chairman Powell, we believe monetary policy will continue to be slow walked and the Fed will remain patient and data dependent as it pertains to raising rates to fight inflation. Lael Brainard, President Biden’s pick for Vice Chair, is unlikely to change the Fed’s course on interest rates but is expected to be tougher on financial services regulations.

Our current view is that inflation will peak and gradually return to the Fed’s 2% target. However, if inflation does not peak in the first quarter, we could see more than the two rate hikes that the futures market is pricing in currently by the end of 2022. Under this scenario, we would not hit our baseline forecast of a 2% yield on the 10-year and would instead likely see closer to 2.5%. While this would not hurt our fixed income allocation (as we expect to continue to underweight the asset class) it could have a negative impact on our equity portfolio, as it could curtail growth and cause a market correction.

Chris Konstantinos: You and I have had many conversations regarding the dynamic around negative real yields in the US bond market…how does this affect your view on fixed income risks and opportunities globally? And how do you think this will affect the US Dollar?

Source: Bloomberg; RiverFront. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Kevin Nicholson: ‘Real yields, which is the return an investor gets for loaning their money to the government for a period of time, continue to fall despite rising inflation expectations. In fact, the yield on TIPS (Treasury Inflation Protection Securities) are negative throughout all maturities (see chart on page 1). Nominal yields appear to be pricing in growth slowing slightly with inflation dissipating. Regardless of which market view is correct, fixed income still is not attractive to us. Negative real yields do not help the bond market but serve as a catalyst for higher prices in risky assets, like stocks, as investors seek higher returns. Additionally, with most of the world having negative real yields (see right chart), US real yields are relatively attractive causing foreigners to gravitate to the US bond market. This added demand will push up the US dollar.

Chris Konstantinos: For savers, people on a fixed income and income investors who wish to generate enough passive income to have a fighting chance of keeping up with cost of living increases in the years to come, what solutions can you recommend? Are there ways to augment traditional yield strategies with ‘alternative’ sources of yield?

Kevin Nicholson: Given the low level of interest rates, it is virtually impossible for investors to meet their income needs using traditional fixed income. Investors can invest in TIPS to help guard against rising inflation but will not generate enough income to make them attractive to investors. One alternative to assist investors in meeting their income goal is high yield, however even using this alternative asset is not sufficient, in our view, in generating attractive risk-adjusted real returns. Thus, investors will likely have to use the equity portion of their portfolio to meet spending needs. In our balanced portfolios, one of our preferred ways to generate yield is through covered call writing.

Chris Konstantinos: Successful bond investors have a well-earned reputation for being aware of contagion risks before equity markets. What possible major risks do you see on the horizon looking forward? How likely do you think they will come to fruition in the next 12 months?

Kevin Nicholson: The biggest risk we see over the next 12 months is a policy mistake by the Federal Reserve as it pertains to fighting inflation. This could come in two forms. First, if the Fed raises rates too soon and dampens economic growth. Right now, the Fed fund futures market is pricing two rate hikes by the end of 2022. The second mistake may be the Fed being too slow to react to increasing inflation, causing it to have to make bigger rate increases to try and catch up. In both cases, the policy misstep will be detrimental to economic growth, and we would experience a significant market correction within risky assets. While we do not believe that the Fed would rest on its laurels in either direction for too long, we put the odds of a policy mistake occurring at 25% currently.

Chris Konstantinos: Tactically, what should investors do if Yields move 50 basis points (bps) up from here in the next 6-12 months? Or down?

Kevin Nicholson: If yields move down 50 bps (bps = 1/100th of 1%) in the next 6-12 months, we believe investors should reduce their fixed income exposure and increase their equity exposure. Conversely, if yields move up 50 bps, we believe investors should rebalance their portfolios back to their targeted equity/bond weights. It is important to remember that this is a general portfolio position scenario, however the catalyst of these events would play into the actual positioning which could differ from the overall general view.

Chris Konstantinos: How do you think about the benefits of bond investing in a balanced account in a low interest world?

Kevin Nicholson: We continue to use a barbell approach to our fixed income strategy. We own corporates on the front-end of the curve to help generate income and Treasuries on the back end of the curve to serve as a shock absorber for risk-off events. Our approach has not changed over the last year because we still find fixed income to be unattractive relative to equities.

Chris Konstantinos: Are there opportunities overseas to add bonds from other countries, and what risks does that pose?

Kevin Nicholson: Given that there is roughly $13 trillion worth of negative yielding debt globally, the opportunities to add overseas bonds to the portfolio without taking on some added risk is limited. Most 10 year developed market sovereign debt is yielding under 1%, so there is not much incentive to buy longer maturity/duration securities for the portfolio that will yield less than shorter duration US high yield in a rising interest rate environment. While there is some emerging markets debt that offers the high single digit to low double digit yields, you would be introducing more credit risk, currency risk, duration risk, and event risk to your portfolio at the wrong time, in our view.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%).

Treasury Inflation Protected Securities (TIPS) are Treasury securities that are indexed to inflation in an effort to protect investors from the negative effects of inflation. The principal value of TIPS is periodically adjusted according to the rate of inflation as measured by the Consumer Price Index (CPI), while the interest rate remains fixed. TIPS will decline in value when real interest rates rise. Portfolios that invest in TIPS are not guaranteed and will fluctuate in value.

An option is a contract sold by one party to another that gives the buyer the right, but not the obligation, to buy (call) or sell (put) a stock at an agreed upon price within a certain period or on a specific date. A covered call option involves holding a long position in a particular asset, in this case U.S. common equities, and writing a call option on that same asset with the goal of realizing additional income from the option premium. Certain ETFs use a covered call strategy. By selling covered call options, the fund limits its opportunity to profit from an increase in the price of the underlying index above the exercise price, but continues to bear the risk of a decline in the index. A liquid market may not exist for options held by the fund. While the fund receives premiums for writing the call options, the price it realizes from the exercise of an option could be substantially below the indices current market price.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1937684