SUMMARY

- International markets present an opportunity but need a catalyst, in our view.

- We believe moderate inflation is a good thing for stocks while interest rates remain low.

- More conservative investors are being forced to own more risky assets to achieve their goals. We believe these risks need to be managed.

Every year around this time, the RiverFront Investment Team looks to communicate our thoughts for the coming year. As a teaser for our 2022 Outlook release in mid-December, I sat down with Global Equity Chief Investment Officer (CIO) Adam Grossman to discuss some of the most important questions facing investors as we move towards the new year, including international investing, inflation, China, tech earnings, and preferred themes to invest in for ’22. In addition, we had a wide-ranging philosophical conversation concerning potential risks, contrarian ideas, and the traits of a high-performing investment team. Here is a transcript of that interview, edited for clarity.

Chris Konstantinos: You can allocate to equities anywhere in the world. How are you currently sizing up the return and risk potential in US markets vs. the opportunity overseas?

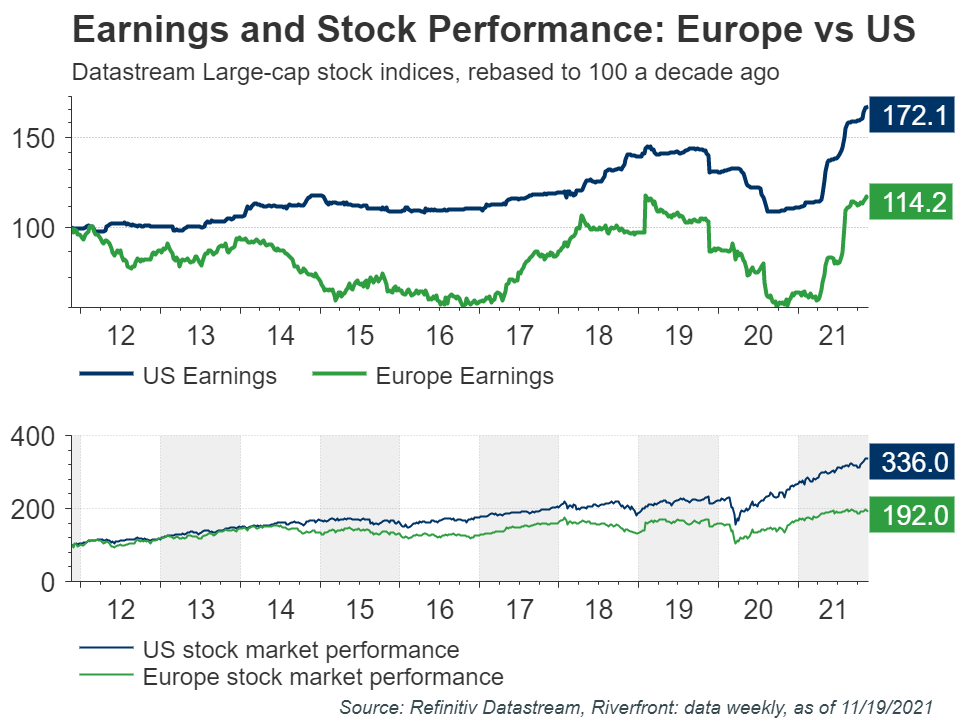

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Adam Grossman: Right now, we are favoring the US. We view international markets as cheaper for sure – both Price Matters® as well as other valuation methodologies confirm this. The problem for International as a ‘value’ play is that ‘value’ works best when there is earnings growth to sustain it. There is a strong case for a positive inflection point in international earnings relative to the US in 2022, but investors have been frustrated on this point for almost a decade. We hope the delay is not indefinite.

While we think there will be opportunities to allocate to international in ’22 as monetary policy diverges between the US and Europe, the question is whether they are just shorter-term ‘trades’ or something more sustainable. This will depend on whether areas like Europe can sustain earnings growth similar to the US, something they have failed to do in the last decade (see chart below).

Chris Konstantinos: In the chart I am displaying to the right, it’s easy to see just how right you are about international – and particularly Europe – underachieving vs. the US in both earnings and stock prices. Why is that, and do you think these trends will persist in the future?

Adam Grossman: US earnings growth has been driven by great global brands, especially in technology. European earnings have been held back by several macro headwinds. Some of these – Brexit, the Euro Crisis, geopolitical headwinds with China, and the various governments’ response to COVID-19 – have hurt GDP growth both relative to the US and in absolute terms. In addition, the corporate sector overseas has been run more for employees than shareholders so overseas companies have been slower to cut costs. Both of these things have had a direct negative impact on international earnings relative to the US.

Furthermore, international stock markets have a higher percentage of ‘cyclical’ sectors vs. the US. Cyclically-oriented companies, who have higher operating leverage, thrive on strong GDP growth – something that the last decade has not really produced overseas. Our belief is that increasing inflation and low and rising interest rates provide a backdrop where higher levels of nominal GDP growth may be generated, and some of these cyclical and value-oriented areas can start to shine, providing the catalyst for international markets.

Chris Konstantinos: Despite inflation at its highest level in decades, bond yields seem stubbornly anchored at low levels relative to history. To what do you attribute this? How long do you think it could persist?

Adam Grossman: We think the reason for low interest rates is that the Federal Reserve has been a huge buyer of government bonds, deliberately keeping interest rates low. Our hope is that this will continue for a long enough period of time to allow some sustainable inflation generation, which will help all debtor nations. This may allow indebted sovereign nations, like the US, a chance to pay off their overwhelming debt in inflation-reduced future dollars. Inflation has historically caused currencies to decline. However, since inflation is a global problem and most central banks are running low interest rate policies, exchange rates are likely to remain relatively stable, in our opinion.

Chris Konstantinos: Volatility has been extraordinarily low since monetary and fiscal policymakers engaged in massive pandemic stimulus. Do you expect volatility to be significantly higher in ’22?

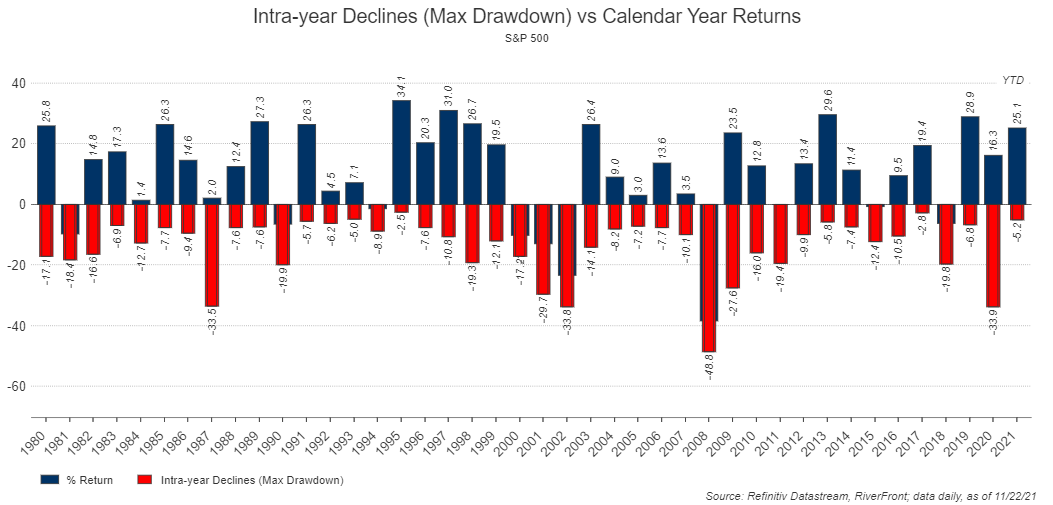

Adam Grossman: Short answer is ‘yes’ – the reality is that intra-year S&P 500 pullbacks of 7-10% or even greater are normal. 2021 was an anomaly, with just one pullback thus far of roughly 5% peak-to-trough (see chart). As we seek to return to more normal interest rate levels and inflation, the stage is set for market pullbacks, even as we see overall positive equity returns. We think a key to our success will be sizing risky positions appropriately so we do not get shaken out of volatile positions. This will require leaning on our risk management processes, and using strategies like covered call writing, which can benefit from higher levels of volatility in driving returns.

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

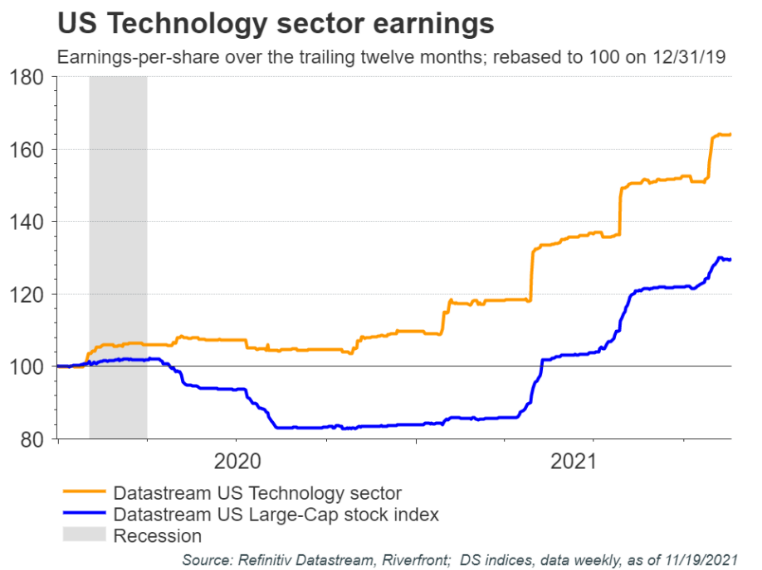

Chris Konstantinos: Technology has significantly out-earned most other S&P sectors over the past year as well as for the past number of years. Remarkably, Tech earnings barely dipped during the recession and are now up ~60% vs. pre-pandemic levels – see chart below as evidence. Do you expect this trend can continue in ’22?

Shown for illustrative purposes. Not indicative of RiverFront portfolio performance.

Adam Grossman: Yes, we think Tech earnings in general will continue to grow, but we do not think that means all Tech companies will outperform. We should also recognize that the stronger earnings potential of Tech vs. other sectors is now well understood. That said, while many view the Technology sector as ‘expensive’, we do not. In fact, we believe the sector is not overvalued based on its extraordinary long-term ability to grow topline and repurchase shares against a backdrop of low economic growth and interest rates. In 2022, we think Value-oriented themes in general will have a slight tailwind vs. Tech (see our Weekly View: ‘Ford Vs. Ferrari’: Comparing the Dow Jones Industrials to the Nasdaq), but we believe it will be a closer race than a lot of people are thinking. In addition, we believe Technology will be more defensive than people expect when growth scares inevitably happen, because of its more consistent earnings and cash flow generation.

Chris Konstantinos: After the controversy surrounding the deteriorating US/China relationship and overarching government regulation, is China still ‘investible’, in your mind?

Adam Grossman: Yes, but cautiously, and best done on a contrarian basis, i.e. trading against sentiment. Uniquely for Chinese equity, for it to ‘work’ as an investment, our view is the following things must happen:

- China must allow profits to flow to the company – this is tenuous given President Xi’s stated goals placing ‘common prosperity’ over corporate profit.

- China must allow foreigners to access those profits – this is also increasingly tenuous, given the growing geopolitical divide between China and the West.

Taken together, this suggests there are better places to allocate capital over the long run, although opportunities will periodically arise when we feel the market over-discounts these risks.

We think one opportunity here is to play China ‘indirectly’ – China is a dominant economic force that creates a massive impact on the global supply chain. China’s challenges may end up being other regions’ gains as the West looks to other areas to fill the void: Mexico, Southeast Asia, and Korea being a few that come to mind. Also, it’s worth noting that many quality companies that play into the tastes of the burgeoning Chinese urban middle class – whether the company is based in China or elsewhere – can be good investments regardless of geopolitics.

Chris Konstantinos: Name one consensus investment view that you believe will be proven wrong in ‘22.

Adam Grossman: The consensus is very worried about high inflation. We believe that acutely high inflation we’re currently witnessing will eventually yield to a combination of greater supply and structural disinflationary forces (innovation and a global labor force) that will bring the level of inflation down and that will be supportive of equity prices. We believe this backdrop will benefit US Growth equities as much as Value-oriented plays, and that Growth equities will become the most defensive stocks (stocks that outperform in a downturn).

We believe we should embrace the inflation that is currently happening, at least to a point. The reality of 2008’s and 2020’s monetary responses is the world is awash in debt, and the only plausible way out of it is ‘financial repression’ – the slow steady suppression of long interest rates below the rate of inflation. The good news for the world is we are all in the same boat together, so it’s not the exchange rate disaster it would be if it weren’t universal.

Chris Konstantinos: What is the biggest risk you see that investors should have on their radar?

Adam Grossman: The biggest risk we see over the next five years is that investors are overpaying for income-generating assets. The quest for income has attracted money from traditionally conservative investors into much higher-risk securities, such as high-yield bonds, preferred stocks, and high dividend equities with low dividend coverage. We think these types of investments are fraught with idiosyncrasies and potential peril that passive investors may not be paying close enough attention to. It’s not that we think these types of investments are necessarily inappropriate, but the risks inherent in them need to be actively managed.

Chris Konstantinos: Do you believe ’22 will be a good backdrop for active portfolio management and stock selection?

Adam Grossman: Yes, we do – higher valuations increase the importance of being selective in searching out value, and in identifying growth opportunities that will last longer than clients expect. Both characteristics represent intrinsic value that we think can be unlocked by active management. I tend to think of the overarching movement from active to passive investing styles acts like a ‘pendulum’, with a swing back to the center after a style becomes too stretched. While large institutional flows have driven passive for a long time, this has opened an opportunity for active management and planning as the pendulum swings. All the data out there is useful, but it takes wisdom to turn that data into information. We think flexibility in investment style will be key to creating core solutions that steadily increase wealth.

Chris Konstantinos: What are a couple of your favorite equity sectors/themes for ’22? Which ones do you think will be underperformers?

Adam Grossman: We have three broad themes we think will be particularly powerful in 2022. These include industries and companies that benefit from sustained low interest rates, ones that benefit directly or indirectly from the reemergence of mild inflation, and companies, like large financial conglomerates and REITs, that benefit from a steep yield curve.

Inflation and low-rate beneficiaries include logistics companies, industrial conglomerates and machinery companies, as well as semiconductors and energy pipeline and exploration & production companies. Indirectly, we think software and IT services companies will remain strong earners who act defensively. We also think property and casualty insurers, payment processors, along with some food retail and medical device and provider companies, will benefit from an upturn in inflation along with solid economic trends.

We think some losers in the environment we’re picturing include materials companies for whom higher commodity prices represent higher input costs, consumer staples companies like big box retailers, grocers, and some pharma who don’t have enough pricing power to adequately pass higher prices on to consumers. We are also cautious on utilities, smaller regional banks, and life insurance companies, who may be disproportionately hurt by low interest rates.

Chris Konstantinos: What is one key aspect of our Investment Team here at RiverFront that you think is underappreciated?

Adam Grossman: It is the right size team – twelve members with a diverse set of experiences and skillsets can go around the horn in a meeting, and bring technical, fundamental, and quantitative perspectives to almost any issue. A smaller team would not be staffed enough, and a much larger team would have more resources but be unable to coordinate and collaborate the way we do.

Chris Konstantinos: As you think about popular conceptions of what makes for a worthwhile investment team or approach, which skills do you think are underrated? Which are overrated?

Adam Grossman: We think any team where the focus is on finding “the answer” will always fail – markets are not random, but there is enough uncertainty that overconfidence on any one approach will lead to failure. We call this the 60/40 rule – even if we are right 60% of the time, that means 2 out of 5 calls will be wrong.

We think a team that goes into any decision with a humbler view of the probabilities of success will approach it differently – multiple disciplines and weight of the evidence will create a more stable view of an investment, and “pre-underwriting” allows us to size bets before they go in. We think that approach is likely to outperform over the long haul.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

There are special risks associated with an investment in real estate and Real Estate Investment Trusts (REITs), including credit risk, interest rate fluctuations and the impact of varied economic conditions.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation.

Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health.

Index Definitions:

Dow Jones Industrial Average Index — measures the stock performance of thirty leading blue-chip U.S. companies.

NASDAQ 100 Index includes 100 of the largest domestic and international non-financial securities listed on the Nasdaq Stock Market based on market capitalization.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1931773