By RiverFront Investment Management

We believe a nuanced approach to “growth” investing is appropriate

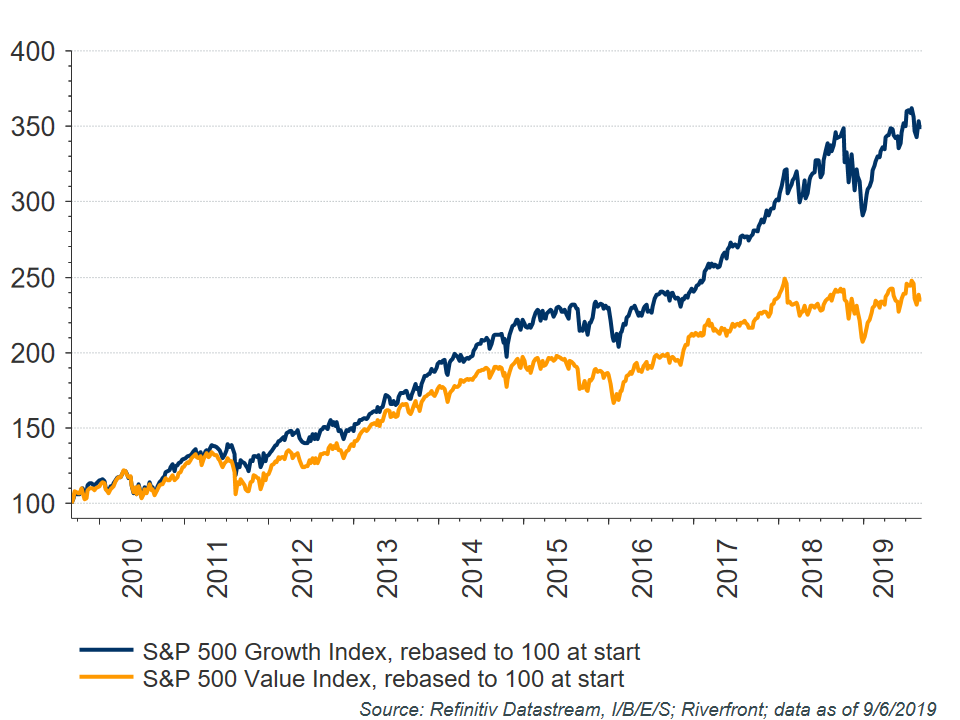

Last week in our Strategic View, we described the US economy as simmering in a ‘low and slow’ phase. We think this aids the durability of our current economic recovery, and believe it has implications on security selection as well. Growth stocks (as defined by the S&P 500 Growth Index) in general have been long-term outperformers relative to Value (as defined by the S&P 500 Value Index) in the US (see chart), but we think a nuanced approach to growth investing is the ”right,“ or appropriate, way to proceed. We believe low economic growth and interest rates, combined with heightened uncertainty, cause US investors to seek out the following characteristics:

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available at the end of this publication.

1. SECULAR TOP-LINE GROWTH: Not surprisingly, in a low GDP growth environment, investors seek out companies and industries that can demonstrate consistent revenue (top-line) growth. Additionally in this cycle there is another challenge for many consumer companies, a theme known as the ”Amazon effect”; the ruthless disintermediation of traditional retail by online shopping. While there are clearly losers, such as traditional shopping malls, there is also an ecosystem of companies and industries that are benefiting from this secular theme. Companies that are succeeding here are making smart adaptations, focusing on the parts of their business that are not “Amazonable,” or growing in areas that complement internet sales initiatives.

2. EFFICIENT AND PRUDENT CAPITAL STRUCTURES: One of the benefits of low interest rates is that they make for an attractively low cost of debt for businesses. Well-run companies can use this capital to grow earnings by reinvesting in their business or via stock repurchase. We favor companies that have the ability and willingness to do both. An optimized capital structure emphasizes a prudent balance of debt and equity that can reduce a company’s vulnerability to negative economic surprises, in our view.

3. ABILITY TO ”GET PAID TO WAIT”: In a low-interest rate environment, investors often look to dividends as a way to replace the lack of returns available in bonds or at the bank. We believe companies that pay dividends out of steadily growing free cash flow will continue to be outperformers in a ”low and slow” environment. Stable cash flow can often be found in businesses with established brands whose goods are less linked to broad economic trends.

HOW RIVERFRONT IS IMPLEMENTING THESE THEMES IN OUR PORTFOLIOS

The economically uncertain environment has, so far, been incorporated into our asset allocation through risk reduction and a greater emphasis on US stocks. In addition, we believe that the stocks and ETFs purchased recently across RiverFront’s portfolios tend to represent one or more of these characteristics. Generally, our investment themes include the following:

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available at the end of this publication.

Software and Services: Our overweight in the technology sector, especially software and services, is intended to allow our portfolios to participate in the structural changes that technology stocks have had on the way we live. We believe the sector’s secular growth has made its earnings and cash flow less sensitive to the cyclical slowdown brought on by tariffs. We also see the continued growth of cloud services and associated activities to be a source of potential long-term growth. Software solutions, and the service-driven implementations of them, are typically important parts of a firm’s drive toward greater efficiency, a key focus in uncertain times. Despite this crucial role, certain larger software and services companies trade at reasonable valuations, in our opinion.

Dividend Growth: While dividend growth is a durable long-term theme for investors, we think it takes on an additional shorter-term appeal when interest rates are low. With rates dropping in the summer, S&P 500 dividend yields are again well above 10-year Treasury rates (see chart). We think this underscores the appeal of companies that can pay and grow dividends. But not all dividend-payers are equal. We prefer companies whose dividends are growing and supported by high free-cash flow over companies that simply pay high dividend yields, which may or may not be sustainable if the economic environment worsens.

Lower-Volatility: We have also sought out companies with strong domestic brands that have helped them to grow geographically, both inside and outside the US. Historically, these companies have also been resilient during economic slowdowns. While we are not forecasting a decline in consumer spending, or a general decline in the overall economy, we recognize that a global recession in manufacturing is underway, a direct consequence of the trade war between the US and China.

Consumer-Oriented Logistics: The growth of home delivery, a big part of the ”Amazon effect,“ has benefitted transportation and logistics companies. Recently, however, many logistics companies have been battered by fears over the effect of trade wars. We think this presents an opportunity to buy logistics companies at attractive valuations. This would include companies in both the package delivery industry and companies that operate warehouses/distribution centers. For example, as a result of the rise of online shopping and the continued resilience of the US consumer, distribution centers are running at capacity. We believe that companies with established warehouses in prime locations will continue to have the ability to increase rents. We also like their attractive current dividend yields and the opportunity for additional dividend growth in the future.

This article was written by the team at RiverFront Investment Group, a participant in the ETF Strategist Channel.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

Dividends are not guaranteed and are subject to change or elimination.

The dividend yield is the ratio of a company’s annual dividend compared to its share price.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the US dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the US dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the US and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-US securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Gross Domestic Product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of the country’s economic health.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

S&P 500 Growth Index measures growth stocks using three factors: sales growth, the ratio of earnings change to price, and momentum. S&P Style Indices divide the complete market capitalization of each parent index into growth and value segments. Constituents are drawn from the S&P 500®.

S&P 500 Value Index measures value stocks using three factors: the ratios of book value, earnings, and sales to price. S&P Style Indices divide the complete market capitalization of each parent index into growth and value segments. Constituents are drawn from the S&P 500®.

You cannot invest directly in an index.

RiverFront Investment Group, LLC, is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or expertise. The company manages a variety of portfolios utilizing stocks, bonds, and exchange-traded funds (ETFs). RiverFront also serves as sub-advisor to a series of mutual funds and ETFs. Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

Copyright ©2019 RiverFront Investment Group. All Rights Reserved. 947881