By Chris Konstantinos, CFA, Director of Investments, Chief Investment Strategist

SUMMARY

- Concerns of a pending recession are rising.

- Traditional indicators suggest that the economy is still healthy, in our view.

- We believe the economy will escape a recession in 2022 but anticipate continued volatility as those fears persist.

Current Signals Still Show Strength

As inflation rages and interest rates move higher, equity markets have felt more pain than the economy. Despite the continued reassurances provided by the monthly economic data releases, worries are mounting that higher prices and borrowing costs will extinguish economic growth. Add to that the growing number of forecasters warning of a US economic downturn, it is understandable that the question we have been getting most often in recent weeks has become “Is the US headed into a recession?” Our house view here at Riverfront is ‘not yet.’

Over the course of this week and next, our editorial team intends to show in detail some of the tools we use to make such determinations and to monitor the likelihood and magnitude of such an event. This week, we focus on some of the most widely followed measures of US economic activity as defined by the National Bureau of Economic Research (NBER), a non-profit network comprised of over 1,700 economists who attempt to retrospectively identify recessions.

According to a recent poll by the Wall Street Journal, economists surveyed in April put the probability of a recession in the US over the next twelve months at 28%. While low, that rate represents a 50%+ increase from the survey data in January. Since then, supply chain disruptions, rising energy costs, and the war in Ukraine have all contributed to inflation, which we believe the Federal Reserve (Fed) must tighten monetary policy to dampen.

At RiverFront, we believe in ‘Process over Prediction,’ which means our portfolio positioning is built to adapt as data changes, and thus not predicated on accurately forecasting the next economic downturn. Nonetheless, we are diligently monitoring economic output for signs of weakness. In addition, we are closely monitoring the trajectory of corporate earnings for the possibility of a significant earnings decline as that could be more impactful to equity markets than an economic recession. Given the frequency of the questions, we believe delving into the elements most often watched as indicators is important to frame our outlook for markets.

Who determines if we are in an economic recession?

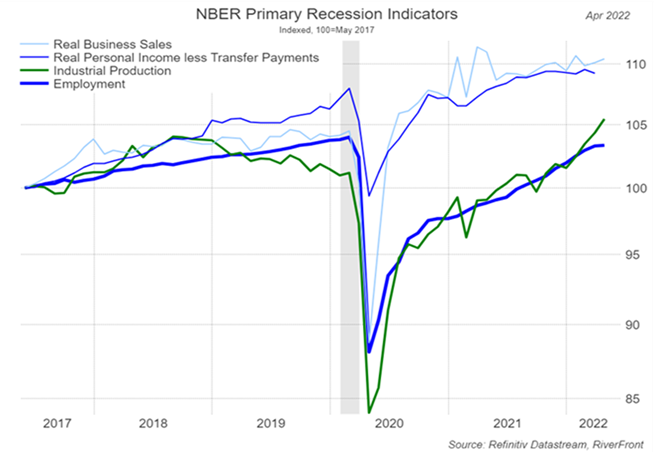

NBER’s definition of recession is a “significant decline in economic activity that is spread across the economy and lasts more than a few months.” The Business Cycle Dating Committee within the NBER makes the determination based on several economic datapoints believed to be gauges for the health of the country’s economy. These include Employment, Real Business Sales, Industrial Production and

Real Personal Income Less Transfer Payments (see chart below.)

Chart: Current Indicators Still Favorable

Just like the NBER, investors can track these metrics monthly. Let’s examine the most recent reports for each component:

- Employment: Positive: In April 2020, the US unemployment rate had risen to 14.8% which is the highest rate observed since data collection began in 1948 according to the Congressional Research Service. The most recent report showed that unemployment had fallen to 3.6%, in line with pre-pandemic levels, a remarkable achievement. Note that a tight labor market raises wage costs and pressures corporate profits.

- Real Business Sales: Positive: We are particularly encouraged by the health in the manufacturing sector given the ongoing issues with supply chain disruptions. The most recent data released by the U.S. Census Bureau revealed that not only were manufacturers’ shipments up month-over-month, but also year-over-year when compared to 2021. In addition to a healthy manufacturing sector, consumers are also doing well as evidenced by remarkably strong April retail sales which increased 8.2% year-over-year. This bodes well for US GDP, as household consumption accounts for over 65% of economic growth.

- Industrial Production: Positive: Despite supply chain issues, the Industrial Production data for April came in significantly above consensus, led by production at auto plants which increased almost 4% after a gain of over 8% in March. We also monitor manufacturing output which is a primary driver for industrial production. Both the ISM Manufacturing and Markit PMI surveys while lower, remain in expansionary territory.

- Real Personal Income Less Transfer Payments: Neutral: There are plenty of metrics to gauge the year over year growth in income for American workers. Earlier this month, the Bureau of Labor Statistics reported that over the previous twelve months, average hourly earnings have increased 5.55%. Additionally, the Atlanta Wage Tracker shows the most recent 3-month moving average for wages is growing at a rate of 6%. Taking home more in our paychecks is a wonderful feeling, but with inflation more than 8%, those gains are being eroded in purchasing power terms. You can observe this in the chart above (see the second line from the top); Real Personal Income Less Transfer Payments is adjusted for inflation. This line appears to have flattened out, in our view.

Looking at all four indicators collectively, we conclude that there are no signs in the latest data of an imminent recession.

Our Focus Remains on Our Process

It is worth noting that NBER’s primary recession indicators, while useful, only identify recession in retrospect. Next week we plan on providing a deeper dive into other indicators, both economic and financial, that we believe along with today’s analysis can help form a predictive recession ‘early warning’ system.

As we stated above, markets have fared poorer than the economy since the beginning of the year. This is not unusual in a Fed tightening cycle. Our opinion remains that volatility will continue and that, in the short term, the path of least resistance for stocks may be to the downside. Ultimately, if the economy can avoid a recession, we think stocks will put in a bottom and resume their uptrend. While we believe a recession will be avoided, our discipline will dictate our decisions. Our strategies reflect our caution as we are underweight stocks and overweight cash in our balanced portfolios.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

The ISM manufacturing index, also known as the purchasing managers’ index (PMI), is a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms. It is considered to be a key indicator of the state of the U.S. economy.

Flash Manufacturing PMI is an estimate of manufacturing for a country, based on about 85% to 90% of total Purchasing Managers’ Index (PMI) survey responses each month.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero).

Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2022 RiverFront Investment Group. All Rights Reserved. ID 2223968