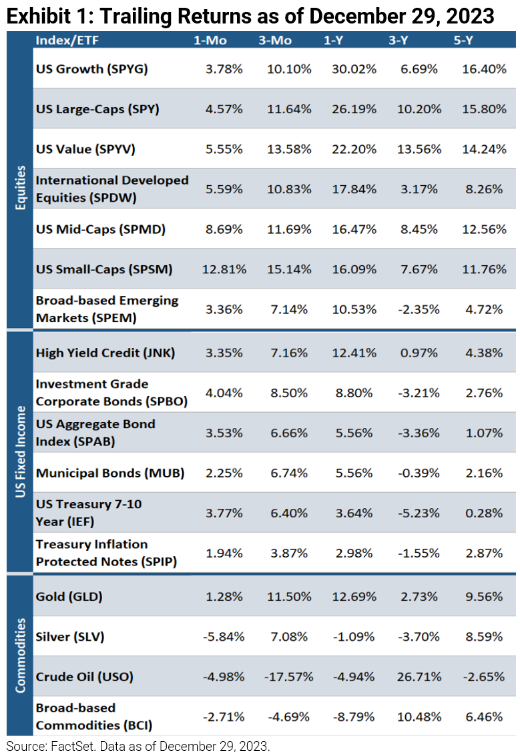

Major Indices Post Gains in 2023, with Many Erasing 2022 Losses

Amid a resilient economy, declining inflation, and increasing probabilities of a soft landing, equities were up in 2023. Though narrow market leadership via big technology stocks ensued for most of the year, market participation broadened in the final two months of 2023 as rates declined and the Fed discussed rate cuts ahead. The technology-heavy Nasdaq Composite was up 44.6%, the S&P 500 gained 26.3%, and the Dow Jones Industrial Average increased 16.2%. US growth (+30.0%) had a strong year while broad-based emerging markets were only up 10.5%. Within bonds, high yield credits were one of the best performers (+12.4%) while Treasury Inflation Protected Notes lagged (+3.0%). Aside from gold (+12.7%), commodities were down as broad-based commodities fell 8.8%, crude oil declined 4.9%, and silver decreased 1.1%.

Fed Signals Rate Cuts Ahead

The Federal Reserve kept interest rates unchanged at the December FOMC meeting, leaving the fed funds rate at the 5.25–5.50% range. Despite the recent sharp fall in bond yields, Fed Chairman Jerome Powell did not contend with the idea of easing monetary policy in the near future. More interestingly, he stated that the Fed discussed the timing of rate cuts, and their updated dot plot projections reveal that officials see 75 bps of cuts for 2024. Powell indicated that restrictive monetary policy is putting downward pressure on economic activity as seen by weakness in the housing market, less major borrowing by businesses, and slowing but still elevated wage growth. “Inflation has eased from its highs and this has come without the significant increase in unemployment. That’s very good news,” he said, suggesting that achieving a soft landing may be more plausible. Calling to mind the dual mandate of the Fed, which is price stability and max employment, Powell expressed the Fed is at or near the point where both goals are important given the progress that has been made. Markets welcomed the dovish tone, and approximately six 25 bps rate cuts are priced in for 2024.

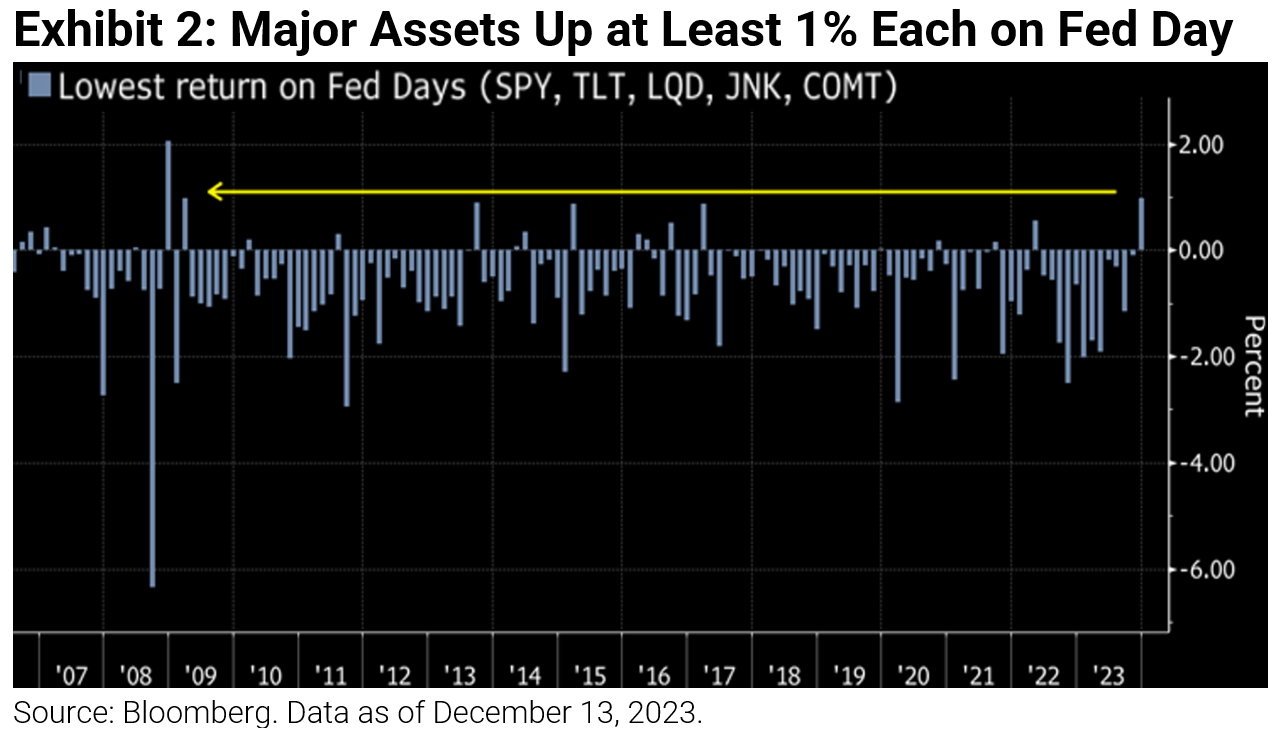

Best “Fed Day” Performance Since 2009

After Powell did not push back on the recent easing of financial conditions or anticipated rate cuts, a range of major assets had their best “Fed Day” performance in almost 15 years on the day of the December FOMC meeting. Large-cap stocks, long-term Treasuries, corporates, high yield credits, and broad-based commodities were all up at least 1%.

Market Breadth Improves

As the Federal Reserve signaled a pivot in its monetary policy campaign, equities have rallied in a broader fashion amid hopes for a healthier economic backdrop ahead. As of December 14th, approximately 78% of stocks in the S&P 500 were above their 200-day moving average.

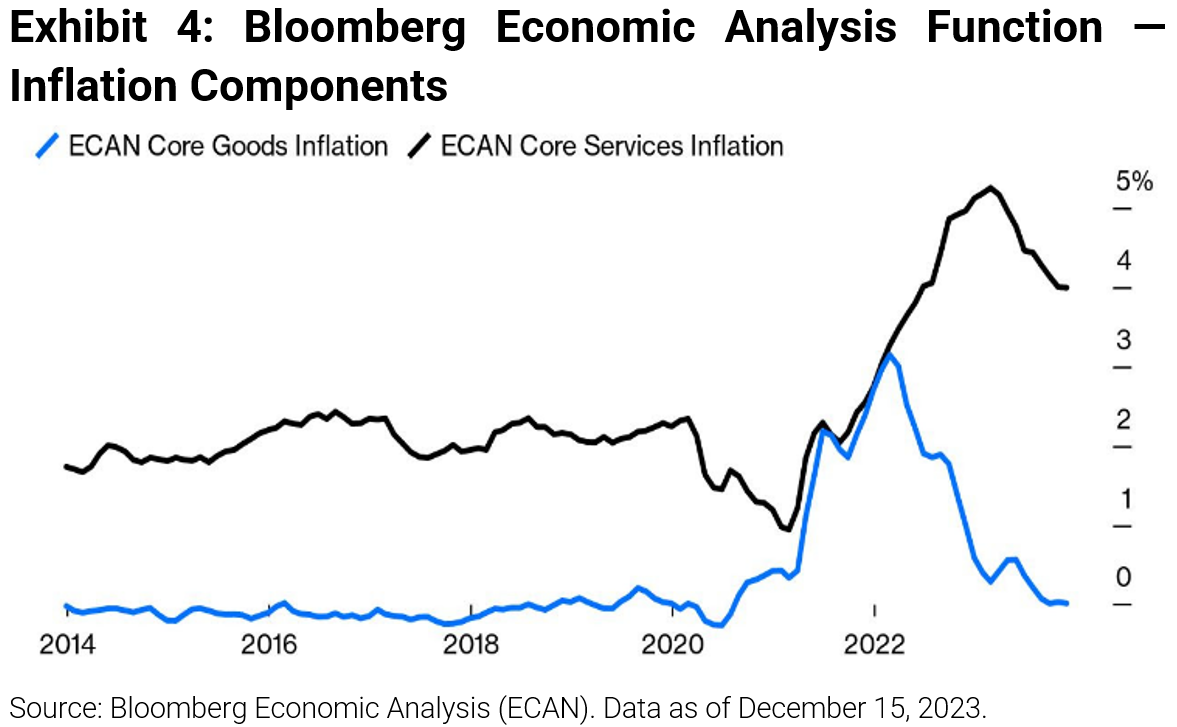

Inflation Down but Still Above Target

Although inflation has come down from its recent highs, measures such as annualized Core PCE and Core CPI (3.2% and 4.0% for November, respectively) still exceed the Fed’s 2% target. As pandemic-related supply chain bottlenecks have come to an end, core goods inflation is back to an annualized rate of 0% and has been a large contributor to inflation’s decline. However, core services inflation, which is tied to wage growth and shelter costs, remains at roughly 4% per year, or approximately double its pre-Covid level.

The Market is Transitioning from an Environment of Rate Hikes to Rate Cuts

1). The rate of change for future rate hikes has materially changed. The market is pricing in a higher probability of rate cuts compared to an incremental rate hike. This inherently translates into a new market cycle and, hence, a different portfolio construct.

2). The US earnings recession is now over. Year-over-year earnings growth for Q3 2023 was 4.9%, well ahead of the -0.3% estimate as of September 30th. As the prior three quarters saw declines, this marks the first quarter of positive growth since Q3 2022.

3) Investors seem to have thrown in the towel on the recession call. Q3 2023 GDP printed a 4.9% handle per the final estimate. In fact, we had an economic expansion amid an earnings recession in 2023. This is quite rare.

Because of items 1, 2, and 3, investors should consider moving beyond T-Bills, rolling, and waiting an entire year to accrue 5%. We believe this won’t cut it in the new cycle. While those T-Bill yields were attractive, just remember there is an opportunity cost of missing out on larger potential equity gains/fixed income price appreciation if the underlying macro picture continues to improve in 2024. Moreover, investors should ask themselves if it’s prudent to keep buying seven US stocks while ignoring the rest of the world. A broadening out of the market is likely to continue as we transition to a new cycle.

We’ve had the fastest rate hiking cycle in nearly half a century, but we’ve had an economic expansion in 2023. Sure, it’s possible that tightening effects materialize in 2024 and the US experiences worse than expected growth, or even negative growth. But what’s going to happen to growth if the Fed cuts rates in the mid to later part of next year? Stocks are forward-looking, and after two years of subdued returns for the average stock globally, it seems risks would be skewed towards the upside in this scenario.

We think six rate cuts is far too aggressive and is likely the market getting ahead of itself. With that said, even the potential end of Fed rate hikes is enough for stock market investors to cheer – see the 16.2% rally in the S&P 500 Index from October 27, 2023, lows through December 29, 2023.

Markets typically trade on the margin, and the rate of change is what drives risk assets. Stocks are forward-looking, discounting instruments and are rallying because six rate cuts are currently priced in for 2024. There is an acknowledgment that inflation is no longer the primary risk for stocks, and the US earnings recession is over.

The biggest risk we see is that lower rates shift back demand curves and re-ignite the inflation trade, leading to incremental rate hikes once again. This is a key reason why we are saying investors should always carry inflation protection.

While the profits recession may be over, corporates are not yet in the clear. With wage growth expected to decline and hiring to be sluggish, earnings and fundamentals may be of focus when it comes to selecting stocks. Stock-specific risk has increased in 2023, and we believe it should rise further in 2024 as macro variables become of less importance while corporate earnings take center stage.

How Should Investors Position Portfolios in 2024?

Increase your equity beta and be overweight equities. Barbell your portfolio risk by owning cyclical growth, transition away from market-cap-weighted strategies, overweight inflation sensitive assets, nibble on international developed markets, and diversify away from US large-cap index beta (we like GARP and US mid-caps). A new cycle usually signals a change in market leadership.

Say sayonara to those T-Bills. If the underlying macro improves in 2024 and market leadership broadens, the opportunity cost of sitting in money market/T-Bills as yields decline could cause one to miss out on larger potential equity gains/fixed income price appreciation. Deploy that cash in the previously mentioned equity cohorts or in fixed income via extending duration and increasing exposure to investment grade, high quality corporates and municipal bonds. Why? Given the level of starting yields, hypothetical forward returns for bonds look appealing.

Play convexity in the rates market. One of our best ideas for 2024 is to use fixed income strategies that benefit from declining rates at the intermediate and back end of the curve given the risk/reward for duration seems attractive. Find alternatives which give equity-like returns but lower volatility. This is crucial. Fund your alternatives by being underweight bonds.

Overweight inflation-linked assets such as energy, industrials, commodity equities, and physical commodities. Various commodities have historically produced positive returns with a high hit rate during prior inflationary regimes. When the profit cycle recovers, value centric stocks have historically performed well. Inflation sensitive assets also tend to have low correlation to US index beta, carry well in a multi-asset portfolio, and many currently trade at a discount to the S&P 500 Index.

Diversify away from the “Magnificent Seven.” If you were underweight technology, close the gap by using equal weighted growth/technology/broad market strategies.

Investors typically have a home country bias, but we strongly encourage advisors to look at international developed markets. Europe and Japan, specifically, have appealing growth prospects. Provided the US recession is modest, the rest of the world should benefit.

Use active managers for emerging markets as the region is highly nuanced. High US interest rates have always been an impediment to emerging market investing; 2023 was no different. However, emerging markets are trading at substantial discount to the US and can aid in portfolio diversification.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, JNK, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, TLT, and LQD on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.

For more news, information, and analysis, visit the ETF Strategist Channel.