If you have been listening to what advisors and portfolio managers have been talking about for the last couple of years you have probably heard about “smart beta”. What is it?

In its simplest form, smart beta (or Alternative Beta) is anything that isn’t a capitalization weighted index strategy. The reason it is “smart” is because it seeks to avoid common drawbacks of a pure index strategy. The reason it is called “beta” (as opposed to alpha) is because it doesn’t involve stock-picking. Beta is, according to capital markets theory, the return of the whole market as opposed to individual stocks. Alpha is the added return on top of the broad market return that a skilled manager can add by picking the right stocks.

Using the S&P500 Index as an example of a benchmark, how is a smart beta strategy different from a pure index strategy?

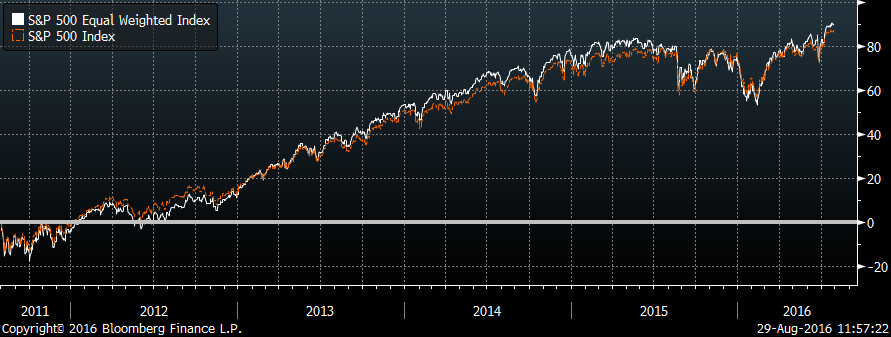

Seen from a smart beta perspective, the biggest problem with the S&P500 Index is that it is a capitalization-weighted index. A basic smart beta strategy would seek to avoid weighing individual names in an equity portfolio based on market capitalization only, since it gives the highest weight to the stocks that have performed the best recently and, conversely, under-weights the worst performing stocks. While this may not be a problem in the short term, the momentum of the best performing stocks will eventually peter out and give way to mean-reversion which will favor the laggards. In fact, history has shown that even a simple equal weighting strategy outperforms a market cap-weighted one over time. As illustrated in the chart below, the Equal Weighted S&P500 Index outperformed the regular Capitalization Weighted S&P500 Index by 35 basis points annually for the 5 year period through July 2016.

{kind=link}

Think about it this way: a cap-weighted strategy implicitly states that companies with higher market caps have a higher expected return than those with lower market caps. Why would you otherwise overweight the higher market cap stocks? Unless we are stock-pickers, a better starting point is to understand that market cap isn’t likely to be a driver of future performance over a long time horizon. So for example, a basic smart beta strategy focused on the S&P 500 Index universe would look for alternative ways of constructing a portfolio without having to express views on individual stocks. While having exposure to all 500 stocks that comprise the Index, it would be weighted in some other way to reflect the belief that larger-cap stocks will not necessarily outperform the other, lower-weighted stocks of the Index.

Smart beta strategies can in essence be reduced to factor-tilting , which means over-emphasizing certain attributes of the portfolio as a whole, such as size (small cap stocks do better over time) or value (low price to book value does better over time). Regarding value, the Price/Earnings ratio of the top 20 stocks by market capitalization in the S&P 500 Index is 35, versus the market as a whole at 20 times trailing 12 month earnings. This means that a portfolio underweight (relative to the Index) in these top names would have a value tilt, or, said differently, more exposure to value as a return factor.

Over the last decade, many alternative approaches seeking to gain exposure to other factors such as value or low volatility within a specific universe have cropped up. Many of these approaches have been successful both in performance terms and in attracting assets. Consequently, from equal-weighting to factor tilt approaches, the marketplace in smart beta ETFs is getting crowded and difficult to navigate for many investors.

Keeping it simple is often a good approach and investors seeking long-term exposure to equities should consider a significant allocation to smart beta ETFs. Historically smart beta strategies have been able to add around 50 basis points of extra return versus a pure index fund, while still charging low fees, and that can really make a difference over time.

RELATED: Macro-Driven Investing in Sector ETFs

At Hillswick, our approach in managing our S&P 500 Sector Strategy is to use Sector ETFs to construct a portfolio that incorporates our desired factor tilts (smart beta), while also expressing our macro view of the economy. The factor tilts can be seen as providing long-term tailwinds for the portfolio while our macro positioning is a form of short to medium term risk management to avoid turbulence. So instead of just owning the sectors according to their weight in the S&P 500 Index, we weigh them based on both their contribution to our desired factor exposure and on how they fit with our macro outlook.

In the next article on this subject I’ll delve deeper into how to use Sector ETFs to build a macro-driven smart beta portfolio.