By Doug Sandler, CFA

SUMMARY

- Following good relative performance in 2022…

- …high-yielding dividend stocks have struggled in 2023.

- The high level of interest rates is a big factor, in our view.

- We expect interest rates to remain higher for longer…

- …and so, expect further underperformance.

Answer: A ‘bond’!

After 20 years of running global balanced portfolios, we have learned a few things. There are no magic bullets, no crystal balls, and no error-free black boxes. That is because the markets reflect human behavior, and as any sociologist would tell you…humans can be fickle and pretty darn unpredictable. For this reason, the legends of Wall Street and their investment strategies get regularly humbled.

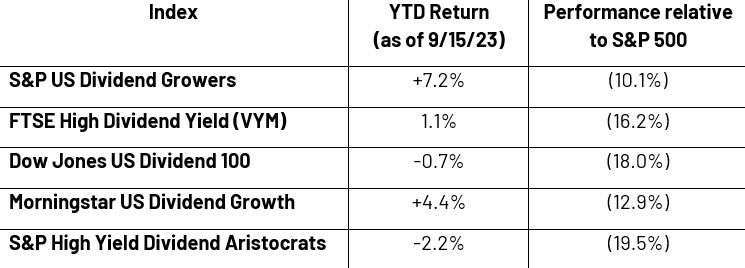

This year it is the dividend stocks – and in particular those that pay the highest dividends- that appear to be taking their turn in the doghouse. One must look no further than five of the most popular dividend indexes (table below) to see their struggle.

Dividend Stocks have Struggled in 2023

Source: Bloomberg, RiverFront. Data daily as of September 15, 2023. Past performance is no guarantee of future results. Chart shown for illustrative purposes. An investment cannot be made directly in an index.

In 2022, the defensive nature of the higher yielding sectors led to outperformance but, as the table shows, with the S&P 500 up over 17% YTD, their relative underperformance (3rd Column) has been significant. In this piece we will argue that the underperformance is set to continue and that our expectation for interest rates to remain higher for longer suggests further underperformance.

Rising interest rates are a headwind for dividend stocks: All investment disciplines have an ‘Achilles heel’, including dividend strategies. The Achilles heel of dividend strategies is rising interest rates and they are negatively affected in at least 3 ways, as outlined below.

1. Rising Interest Expenses: Many dividend companies are highly indebted. For this reason, rising interest rates can have significant negative impacts on a company’s health. As interest payments rise, dividend coverage rates fall, and the risk of future dividend cuts can increase. In our view, the trading range for interest rates will likely remain higher for longer, which is why we expect high dividend yielders to continue underperform from here.

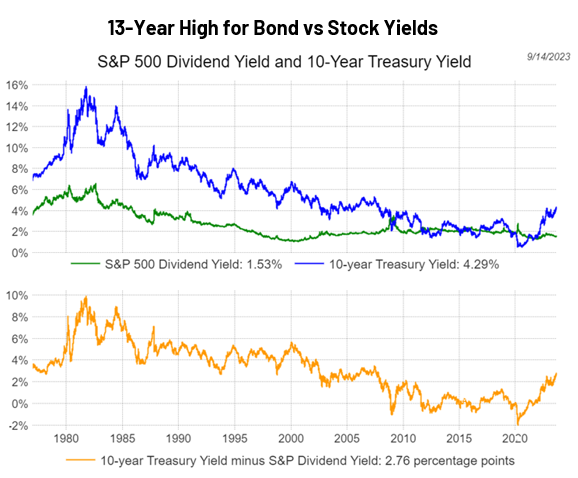

2. Substitution Effect: Rates on the 10-Yr Treasury have risen from 1.5% at the beginning of 2022 to over 4.3% today. As the chart to the right shows the 2.80% (280bps) jump in the 10-year Treasury yields (blue line) was one of the larger increases in history, nearly tripling the low-water mark for rates in this cycle. As a result, bond yields are now at a 13-year high relative to stock yields (orange line bottom panel). With the rise in rates, investors now have multiple income producing options with competitive yields to choose from, including Treasuries.

Source: LSEG Datastream, RiverFront. Data as of September 14, 2023. Chart shown for illustrative purposes. An investment cannot be made directly in an index.

3. Low Earnings Growth: One of the best ways to fight rising inflation and interest rates is to grow cash flows faster than inflation. Companies that can quickly grow earnings and cashflow have the ability to ‘outrun’ a higher rate environment, because they tend to have a greater ability to ‘pass along’ higher costs to their end customers. Unfortunately, some of the highest-yielding dividend indexes have significantly less exposure to growth-oriented companies and industries and are thus more likely to experience declining profit margins.

In addition to the direct pressures from rising rates, it is also important to note that dividend investing has been one of the hottest trends in investing over the past few years. While there have been many good reasons for its popularity, we think the ‘crowd’ may have gotten to an ‘extreme’ by the end of 2022, because dividend stocks held up relatively well in a tough equity market environment.

The Way Forward: There are ways to make dividend investing less sensitive to rising rates. While you can’t eliminate interest risk entirely, there are ways to lower a portfolios’ sensitivity. Below are a few of our favorites.

- Focus on dividend growth: The more a stock looks like a bond, the greater its vulnerability to the direct effects of rising rates. Stocks with the highest dividend yields tend to look the most like bonds, because they have little room to grow their yields. We prefer companies with significant annual dividend growth (greater than 5%). For instance, we find a meaningful number of strong dividend growers in the mega-cap tech space, a theme that we expounded on in our Weekly View in June. These stocks can compete more effectively against bonds in the environment we foresee, since most bonds don’t grow their coupons.

- Be more inclusive: When thinking about dividends, we regularly consider new dividend initiators and even a few companies that have yet to pay a dividend but generate significant free cashflow. Often the future’s fastest dividend growers are found in these categories of stocks.

- Consider ‘sector neutrality’: Traditional dividend strategies tend to focus on maximizing yields. As a result, they can create significant sector concentrations, like favoring utilities. They can also create absences, like avoiding information technology. Those biases can lead to an underweight in powerfully positive fundamental themes. In our portfolios, RiverFront prefers to focus more on dividend and cash flow growth over simply high dividend payouts.

Conclusion: We Expect the Impact of Higher Rates to Lead to Further Underperformance

The idea that dividend stocks should ‘catch back up’ to a stock market that is up significantly this year, is misplaced in our view. For this to happen, we believe that interest rates would need to decline by a significant magnitude. With the Fed willing to let rates remain ‘higher for longer’ and a strengthening US economy that will likely hold them to their word, we have little faith that rates will be declining to pre-2022 levels anytime soon, if ever.

We think this will be increasingly reflected in the earnings of high dividend payers since some impacts from rising rates will likely be delayed and not reflected in earnings immediately. For example, a company’s interest expense will not change until their lower interest-bearing debt matures and gets refinanced at higher rates. Slower growing companies may also have greater difficulty passing along rising inflation costs to their customers, and the resulting drop in profit margins may only appear later.

As a result, RiverFront portfolios have a greater focus on more high growth sectors like Technology, economically sensitive sectors like Energy and Industrials and an underweight to high-yield, low-growth sectors like Utilities and select areas of Consumer Staples.

For more news, information, and analysis, visit the ETF Strategist Channel.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Principle Risks:

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Interest rate sensitivity is a measure of how much the price of a fixed-income asset will fluctuate as a result of changes in the interest rate environment. Securities that are more sensitive have greater price fluctuations than those with less sensitivity. This type of sensitivity must be taken into account when selecting a bond or other fixed-income instrument the investor may sell in the secondary market. Interest rate sensitivity affects buying as well as selling.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Dividends are not guaranteed and are subject to change or elimination.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

The S&P U.S. Dividend Growers Index is designed to measure the performance of U.S. companies that have followed a policy of consistently increasing dividends every year for at least 10 consecutive years. The index excludes the top 25% highest-yielding eligible companies from the index.

The FTSE High Dividend Yield Index is derived from the U.S. component of the FTSE Global Equity Index Series (GEIS) and includes stocks with the highest dividend yields (excluding REITs).

The Dow Jones U.S. Dividend 100 Index is designed to measure the performance of high-dividend-yielding stocks in the U.S. with a record of consistently paying dividends, selected for fundamental strength relative to their peers, based on financial ratios.

Morningstar US Dividend Growth Index tracks U.S.-based securities with a history of uninterrupted dividend growth. The index is a subset of the Morningstar US Market Index, a broad market index representing 97% of U.S. equity market capitalization.

The S&P High Yield Dividend Aristocrats® index is designed to measure the performance of companies within the S&P Composite 1500® that have followed a managed-dividends policy of consistently increasing dividends every year for at least 20 years.

The 10-year Treasury yield describes what 10-year U.S. Treasury notes will pay over 10 years if bought today.

A bond yield is the return an investor realizes on a bond. Put simply, a bond yield is the return on the capital invested by an investor. Bond yields are different from bond prices—both of which share an inverse relationship. The yield matches the bond’s coupon rate when the bond is issued. Bond yields can be derived in different ways, including the coupon yield and current yield. Additional calculations of a bond’s yield include yield to maturity (YTM) among others.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2023 RiverFront Investment Group. All Rights Reserved. ID 3119711