By Kevin Nicholson, CFA and Tim Anderson, CFA

SUMMARY

- We believe a diversified portfolio of individual bonds is difficult to build without a sizable time and dollar investment.

- Mutual funds provide greater diversification than individual bonds, but less customization, in our view.

- ETFs can provide diversification and are a good small portfolio solution, in our opinion.

Making Sense of a Confusing Bond Investment Landscape

After years of investors neglecting bonds due to near-zero interest rates, the once forgotten asset class is now back in the spotlight. For this reason, we have decided to write a piece that would reorient investors with bond fundamentals to help investors make informed decisions, and to dispel the myth that the asset class is complicated. In this publication we will discuss the characteristics of bonds, compare both the different investment vehicles that are used to gain exposure to bonds, as well as strategies to deploy bonds in portfolios.

Fixed Income as an Asset Class:

The fixed income market consists of both traditional and non-traditional sectors. The traditional sectors consist of Treasuries, government agencies bonds, mortgage-backed securities, corporate bonds, commercial mortgage-backed securities, and asset-backed securities. These sectors are in the Bloomberg Aggregate Bond Index, which is representative of the US investment grade bond market and serves as the primary benchmark for measuring fixed income portfolio performance. Some of the non-traditional sectors within the fixed income market are high yield bonds, emerging market debt, bank loans, preferred stock, and convertible bonds. The non-traditional sectors typically require a higher level of due diligence and risk tolerance. Together the combination of sectors represents the fixed income market product mix.

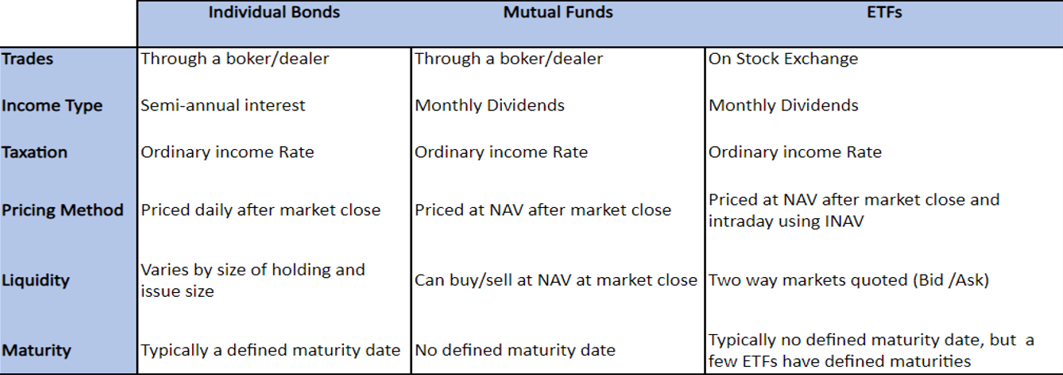

Individual Bonds:

Individual bonds offer clients the flexibility to control cash flow more precisely, because bonds typically have specific maturity dates and pay coupon payments every six months. A well-constructed portfolio can create a consistent cash flow ‘check’ for the investor on a monthly basis. However, it will take a large investment to be able to pull this off in a meaningful way. Individual bonds on a whole require a higher initial investment than their equity peers, as the par value of a single bond is typically $1,000 per bond. Individual bonds can trade at, above, and below the par value depending on the credit worthiness of the issuer, the current level of interest rates, and the specific interest rate (coupon) that the bond was issued.

Given the price of a single bond, it is difficult for individual investors to build a diversified portfolio of bonds without making a sizable investment. For instance, if a $100,000 portfolio has an allocation of 50% equities and 50% bonds, only $50,000 will be allocated to bonds…which would make it difficult to have a diversified bond allocation. With a $50,000 allocation, theoretically an investor could allocate $10,000 to five different bonds and ladder the maturities to build the fixed income portfolio, but the investor ends up with a concentrated fixed income allocation. A concentrated portfolio may be over exposed to individual issuers, credit quality, sectors, and industry groups. Concentrated portfolios can be vulnerable during periods of rising interest rates, as longer maturity bonds are more sensitive to the changes in rates, thus they endure more price volatility. Hence, the need for a more diverse portfolio construction if the fixed income allocation is small. Additionally, from a liquidity standpoint, it is difficult to trade just $10,000 worth of a bond without the buying/selling dealer applying a markup/discount to the price due to the small transaction size.

Hence, pooled investments were created to address both the need for diversification and to overcome the trading hurdles that occur when buying individual bonds in smaller increments. Pooled investments allow the average investor the opportunity to gain exposure to the fixed income asset class by purchasing partial interest in a portfolio that has credit diversification. We believe that it is more important to diversify credit risk than to simply have diversification of issuers due to the return profile of bonds, which are capped on the upside but theoretically can go to zero if an issuer defaults. The two most popular pooled investment vehicles are mutual funds and exchanged traded funds.

Mutual Funds:

A fixed income mutual fund invests in hundreds and possibly thousands of individual bonds, by pooling the money from many investors. Shares of mutual funds are purchased/sold through broker dealers or directly with the issuer at the fund’s Net Asset Value (NAV). The NAV is calculated by taking the value of the fund’s total assets and subtracting its total liabilities, and then dividing that value by the number of shares outstanding for the fund. Investors in the mutual fund will then receive their proportional ownership in the fund based on the amount of their investment.

Even though each individual bond in the fund will pay its coupon every 6 months, the fund itself will pay out the coupon payments (minus fund expenses) on a monthly basis. Investors in the fixed income mutual fund will receive interest payments in the form of dividends that can fluctuate from month to month due to each bond having its own coupon and payment dates.

One of the benefits of investing in a mutual fund versus owning an individual bond portfolio is the investor receives a diversified portfolio with a lower initial outlay. However, unlike the individual bond portfolio, the investor can only buy and sell their shares in a mutual fund at the end of each trading day after the fund’s NAV is calculated. In contrast, investors in an individual bond portfolio can buy/sell any of their bonds in the portfolio anytime during the trading day. Additionally, mutual funds do not have a defined maturity, even though bonds inside the fund will either mature or be sold once the bonds are within a year of maturity.

Exchanged Traded Funds:

Fixed Income ETFs have some similarities to mutual funds, such as they invest in hundreds to thousands of individual bonds (diversification), dividends are paid monthly, they calculate a NAV at the end of the day, and they typically have no defined maturity. While there are similarities with mutual funds, there are a few differences as well. For instance, ETFs trade throughout the day on the public stock exchanges – an advantage when compared to mutual funds, in our opinion – and are quoted with a bid and ask price from the market makers, who are sometimes Authorized Participants (‘AP’). An AP is a financial institution that manages the creation and redemption of an ETF’s shares. The APs price the basket of bonds using an intra-day NAV (‘INAV’) based on where the underlying bonds are trading during the day. However, the price at which the fixed income ETF is traded on the exchange could be at a premium or a discount to its NAV.

ETFs tend to have lower expense ratios than mutual funds, with index-tracking ‘passive’ fixed income ETFs usually having lower expense ratios than actively managed fixed income ETFs. In addition, there are no front-end/back-end expenses when purchasing ETFs that often exist with mutual fund purchases. Thus, we view ETFs as a more efficient vehicle for fixed income investing than mutual funds.

Similarities and Differences:

How to Implement:

We feel that each of the investment solutions that have been discussed may have a specific place in one’s investment lifecycle. We believe that mutual funds are appropriate in company 401k plans where there is not an emphasis on trading. However, as ETFs become available in the 401k arena, we believe that they will take additional market share away from mutual funds given their superior cost structure.

As it pertains to ETFs, investors can build a fixed income portfolio using passive low-cost ETFs to gain exposure to the Bloomberg Aggregate Bond Index sectors, while satelliting with non-traditional assets to dial the risk exposure up and down for a reasonable price. We believe that ETFs are the best way to gain fixed income exposure if you want to minimize the risk of an individual company defaulting on its debt.

Lastly, individual bond strategies should be utilized when the investor has a large portfolio with specific needs that must be accommodated. For instance, a high net worth individual may be looking to reduce his/her tax bill and are looking for state specific municipal bonds to reduce the amount of taxes paid annually. In instances such as this, it makes sense to use individual bonds because there are fewer liquidity issues due to position sizes and it provides the investor with a customized solution specific to his/her needs.

Conclusion:

There are several different ways for investors to gain exposure to the fixed income markets. Our portfolios are geared to gaining that exposure through ETFs, given the varying minimum account sizes at our sponsor firms. Our fixed income team can pull levers to adjust the portfolio of ETFs to manage yield curve movements, credit risk, and duration risk. Additionally, where available, we do allow customization of our strategies using individual bonds on platforms where the account sizes are sufficiently large. We believe it is important for investors to consider accessibility, cost, and needs when deciding on which structure is appropriate for helping them meet their investment objectives.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Dividends are not guaranteed and are subject to change or elimination.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Index Definitions:

The Bloomberg Aggregate Bond Index or “the Agg” is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

Definitions:

Fixed income broadly refers to those types of investment security that pay investors fixed interest or dividend payments until their maturity date. At maturity, investors are repaid the principal amount they had invested. Government and corporate bonds are the most common types of fixed-income products.

An exchange-traded fund (ETF) is a type of pooled investment security that operates much like a mutual fund. Typically, ETFs will track a particular index, sector, commodity, or other assets, but unlike mutual funds, ETFs can be purchased or sold on a stock exchange the same way that a regular stock can. An ETF can be structured to track anything from the price of an individual commodity to a large and diverse collection of securities. ETFs can even be structured to track specific investment strategies.

A mutual fund is a financial vehicle that pools assets from shareholders to invest in securities like stocks, bonds, money market instruments, and other assets. Mutual funds are operated by professional money managers, who allocate the fund’s assets and attempt to produce capital gains or income for the fund’s investors. A mutual fund’s portfolio is structured and maintained to match the investment objectives stated in its prospectus.

Net Asset Value (NAV) is the net value of an investment fund’s assets less its liabilities, divided by the number of shares outstanding. Most commonly used in the context of a mutual fund or an exchange-traded fund (ETF), NAV is the price at which the shares of the funds registered with the U.S. Securities and Exchange Commission (SEC) are traded.

Indicative net asset value (iNAV) is a measure of the intraday net asset value (NAV) of an investment. INAV is reported approximately every 15 seconds. It gives investors a measure of the value of the investment throughout the day.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2023 RiverFront Investment Group. All Rights Reserved. ID 3131573

For more news, information, and analysis, visit the ETF Strategist Channel.