By Komson Silapachai

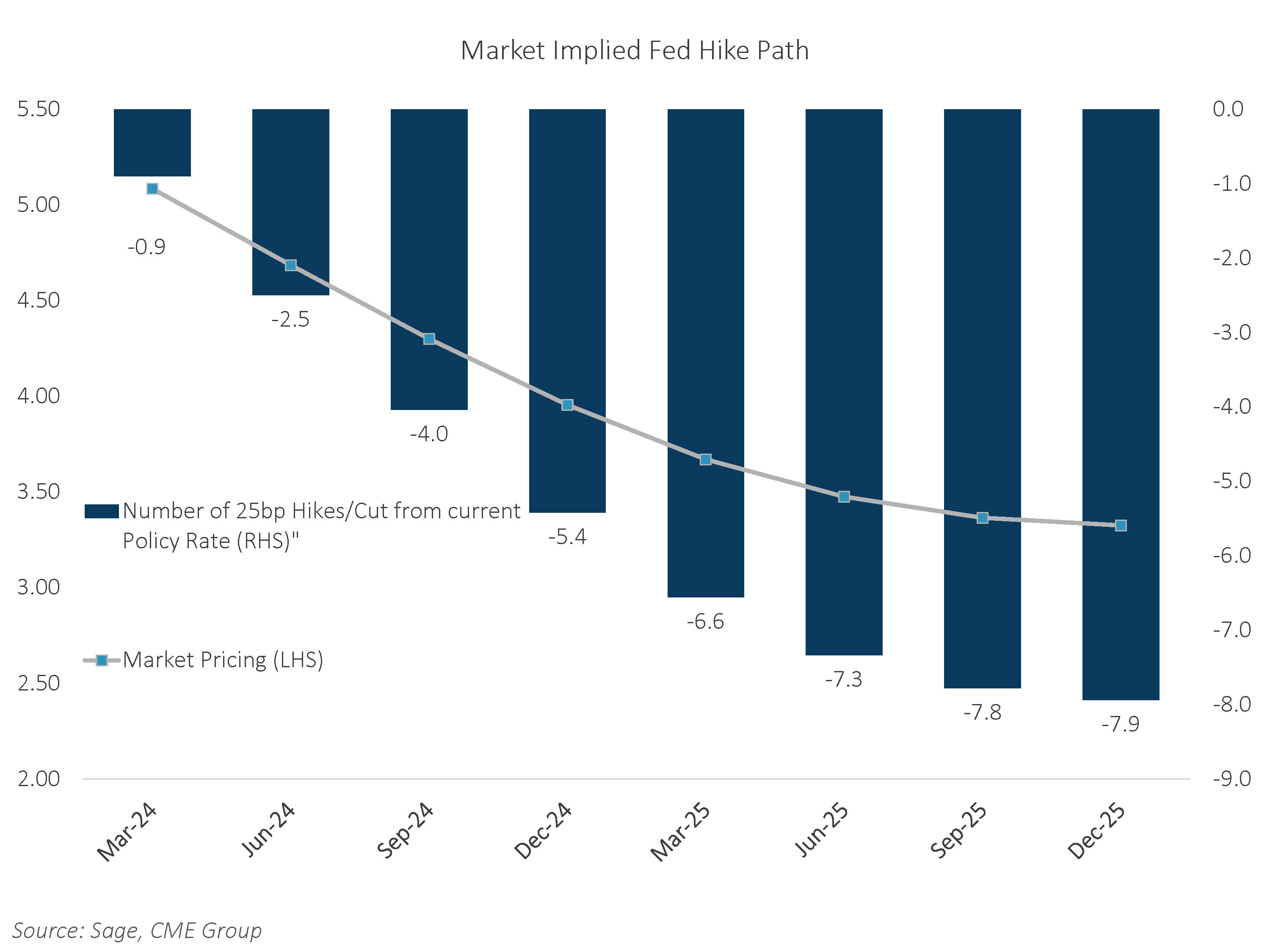

Declining inflation through the second half of 2023 has given the Fed the green light to pivot to the other side of their dual mandate: economic growth. The markets responded in kind, with a blistering rally in both fixed income and equities to end 2023. But do conditions warrant over five rate cuts in 2024? Given the available data readings, we believe the markets are getting ahead of themselves in pricing such an aggressively dovish scenario. Nonetheless, we believe risk/reward is favorable for fixed income as historical record points to solid returns for duration post-Fed hiking cycles.

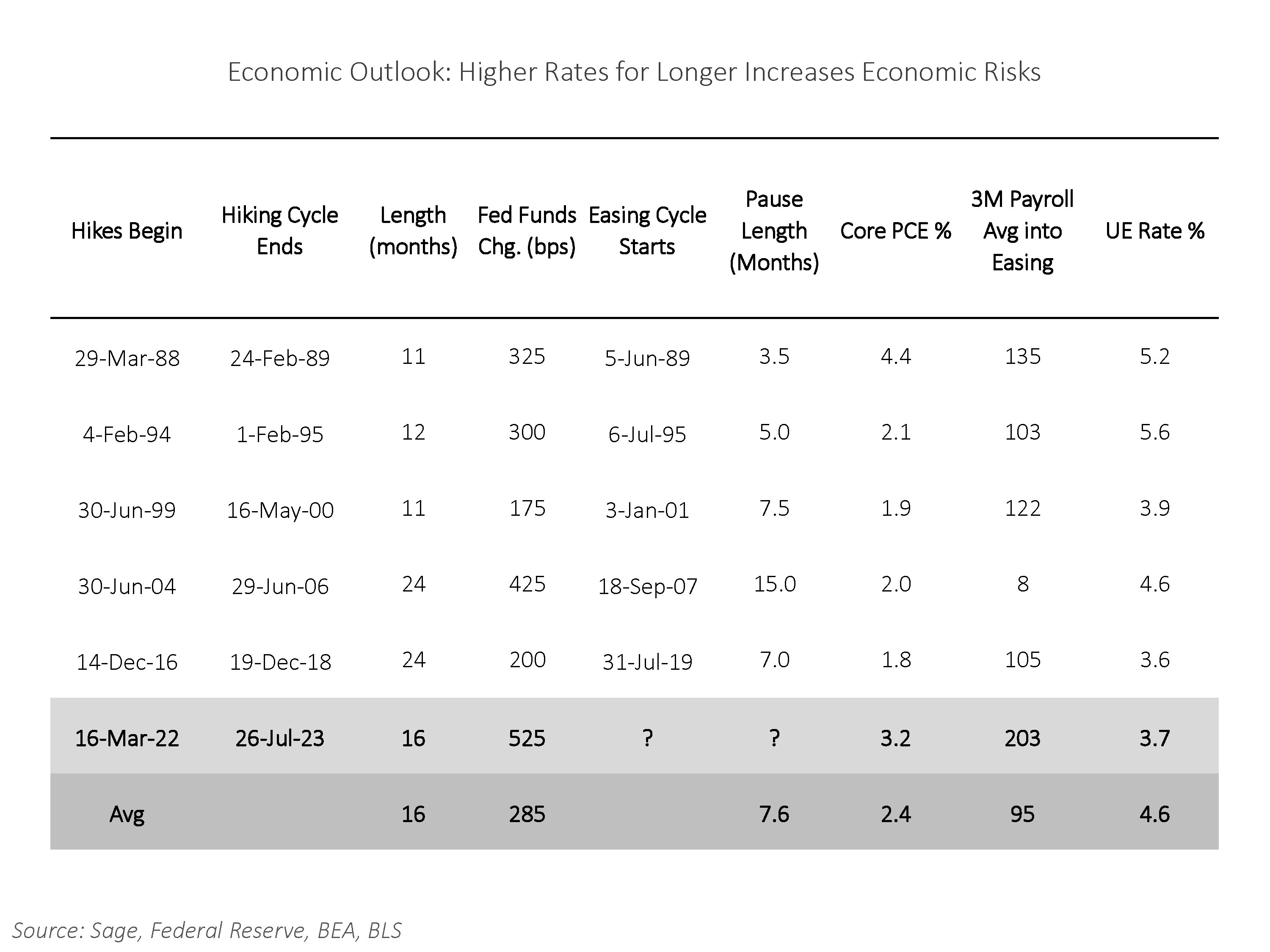

2. Economic Readings are Stronger than During Past Fed Cuts. The Fed typically cuts rates 8 months after the final rate hike which would line up with March 2024 for the onset of cuts. However, labor data is much stronger than would warrant rate cuts in the past.

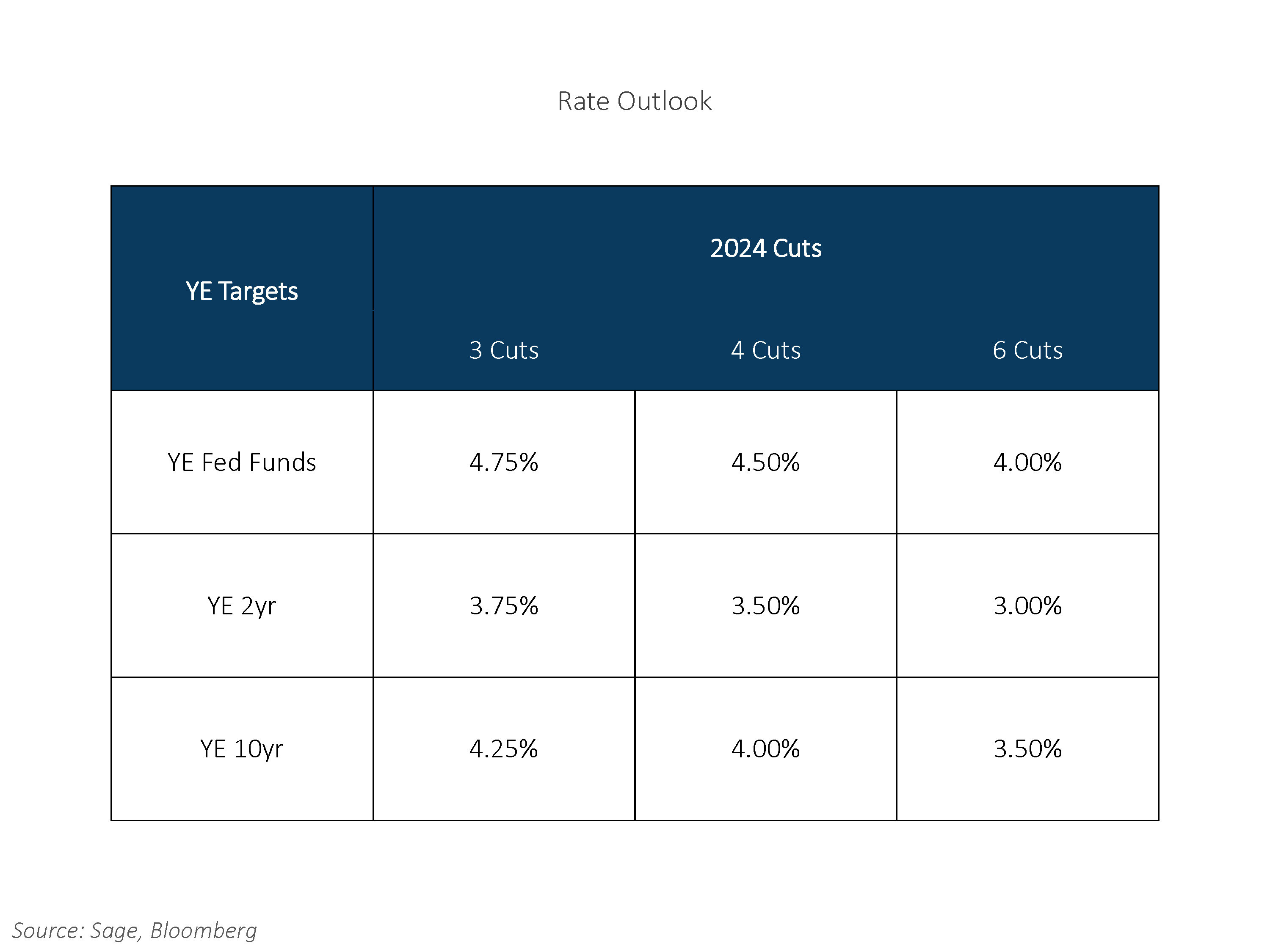

3. Year-End Yield Targets Relative to Number of Rate Cuts: We see three to four rate cuts this year as more likely given current economic conditions, which would see the 10-year Treasury yield at 4% at year end. Other outside factors could be term-premium changes relative to FOMC bond purchase programs and/or the size of global bond issuance on the year. In the case that an economic slowdown is deeper than the soft-landing that has become consensus, the level of yield could fall further.

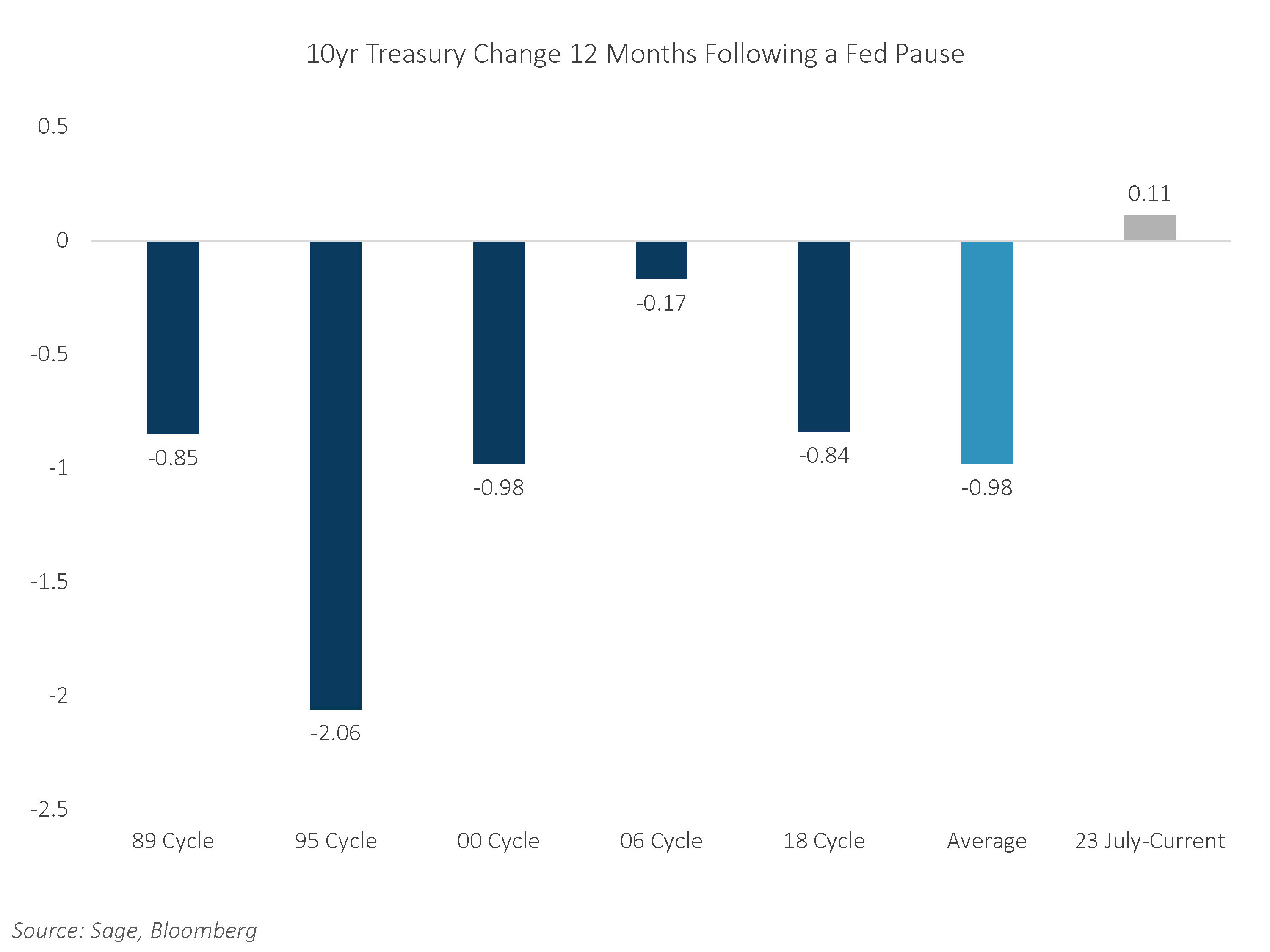

4. Current Market Pricing and Market Environment Favor Fixed Income. Fixed income remains one of the best risk-adjusted opportunities across markets given their historical performance post-rate hiking cycles. While there may be some near-term volatility in rates as the timing of rate cuts is still uncertain, over the next 12 months we believe rates are biased lower.

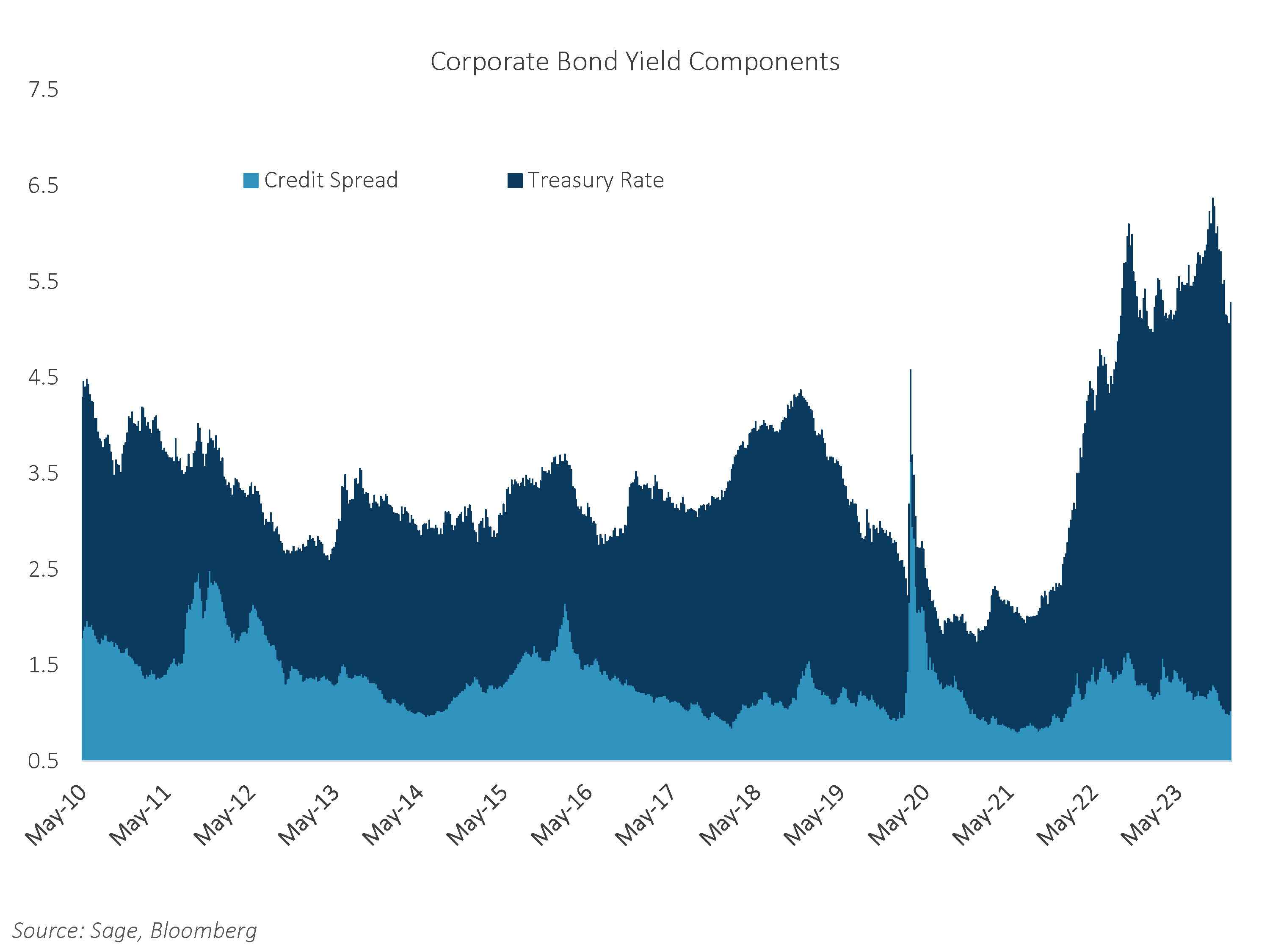

5. It’s About the Level of Yield, not Spreads. While corporate credit spreads are not offering historically high premium over Treasuries, we continue to see robust demand into high quality bonds. Industry and issuer selection will be key as there is less “juice” left to squeeze by being overweight credit as a sector.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our website at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.

For more news, information, and analysis, visit the ETF Strategist Channel.