We recently received an email inviting us to a webinar titled How to Position Portfolios for the “New Economy”. Anyone who lived through the late-1990s Tech Bubble is probably now cringing. It’s hard to believe that the Tech Bubble burst 19 years ago (NASDAQ’s bubble related peak was March 2000), but George Santayana’s famous quotation unfortunately seems to sum up the current environment, “Those who do not learn history are doomed to repeat it.”

The basic principles of economics and finance don’t have a subparagraph saying, “this holds for every industry except for Technology.” Our bearish views on Technology in the late-1990s were based on the simple fact that return on capital is highest when capital is scarce.

A mad rush to invest in anything (tulips, gold rush, technology stocks, housing, etc.) means that the longer-term investment returns will likely be subpar. The associated innovations may come to fruition, but investors should only care about their return on investment. The spread of the internet since the Tech Bubble has clearly had a major positive impact on the global economy, but many of the bubble’s hot stocks no longer exist. Technology is cyclical We significantly lowered our exposure to technology at the beginning of the year (from roughly 26% to about 11%) because Technology has historically been among the most cyclical sectors, and tends to underperform when profits cycles decelerate.

Our forecast is that the S&P 500® GAAP profits growth will slow from roughly 23% in 2018 to 0-5% in 2019. If that forecast proves correct, then Technology has a high probability of underperforming.

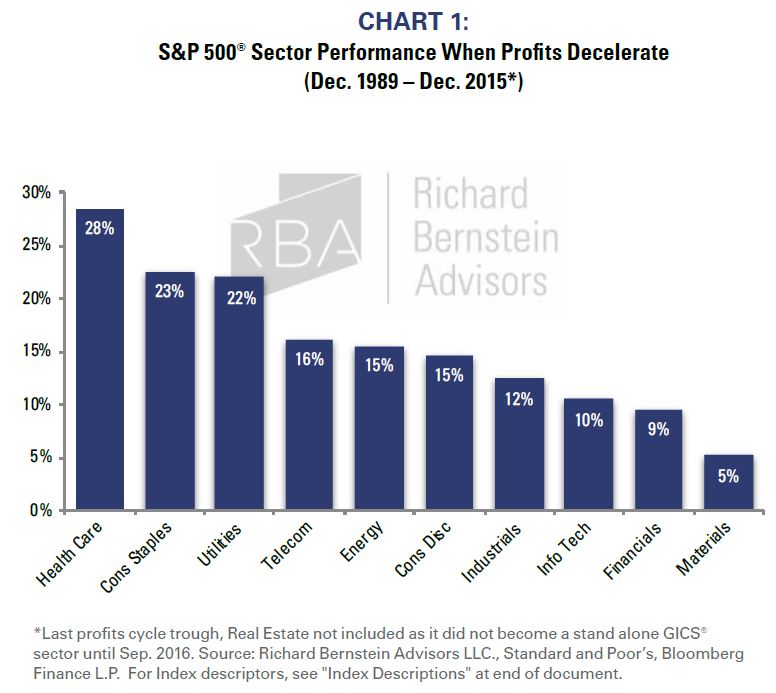

Chart 1 shows the performance of S&P 500® sectors when profits decelerate. Technology is the third worst performing sector. Most investors know that technology stocks are high-beta stocks, and that they tend to be more volatile than is the overall market. However, investors seem to forget that beta is generally symmetric. In other words, the sector is sensitive to both the upside and the downside.

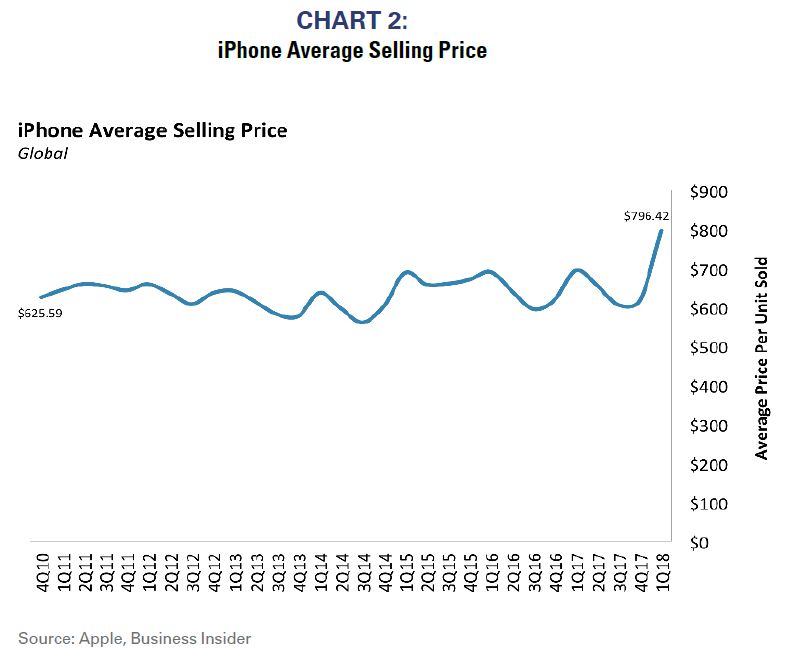

The inherent business of some technology companies may be more cyclical than analysts forecast. For example, Chart 2 shows the average selling price of an iPhone in the US.

The current price of the 2018 models, roughly $750-$1,000, is higher than the average selling price of a dishwasher and comparable to washer/dryer combinations. Appliances are considered durable goods, and consumers don’t mind paying higher prices because they mentally amortize the cost over the appliance’s anticipated 15-20 year lifespan.

Mobile phones rarely have a lifespan of even 5 years, but consumers are expected to pay durable goods prices for a non-durable good. Such odd economics might work when employment is strengthening (as it has been during the majority of the time period shown), but seem unlikely to work should employment cyclically weaken at some point.

Capital is flowing. Confidence is building Regardless of the sector involved, investors tend to primarily focus on momentum toward the end of a cycle and ignore the simple principle that returns are highest when capital is scarce.

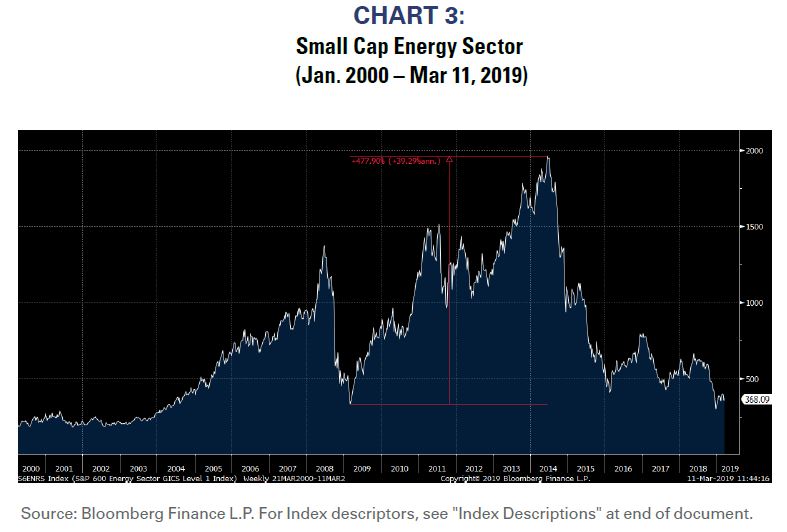

For example, Chart 3 shows the performance of the S&P 600 SmallCap® Energy Sector. The sector appreciated nearly five-fold from 2009 to 2014, the last two years of which were a classic momentum period when stock performance and capital flows significantly outpaced fundamentals. It wasn’t only investors who acted imprudently during the momentum period. The availability of cheap capital led energy companies to build inventories, increase debt, and expand capacity, which added tremendous operating and financial leverage to the businesses. As the cycle began to turn down, the added operating and financial leverage accelerated and exacerbated the downturn.