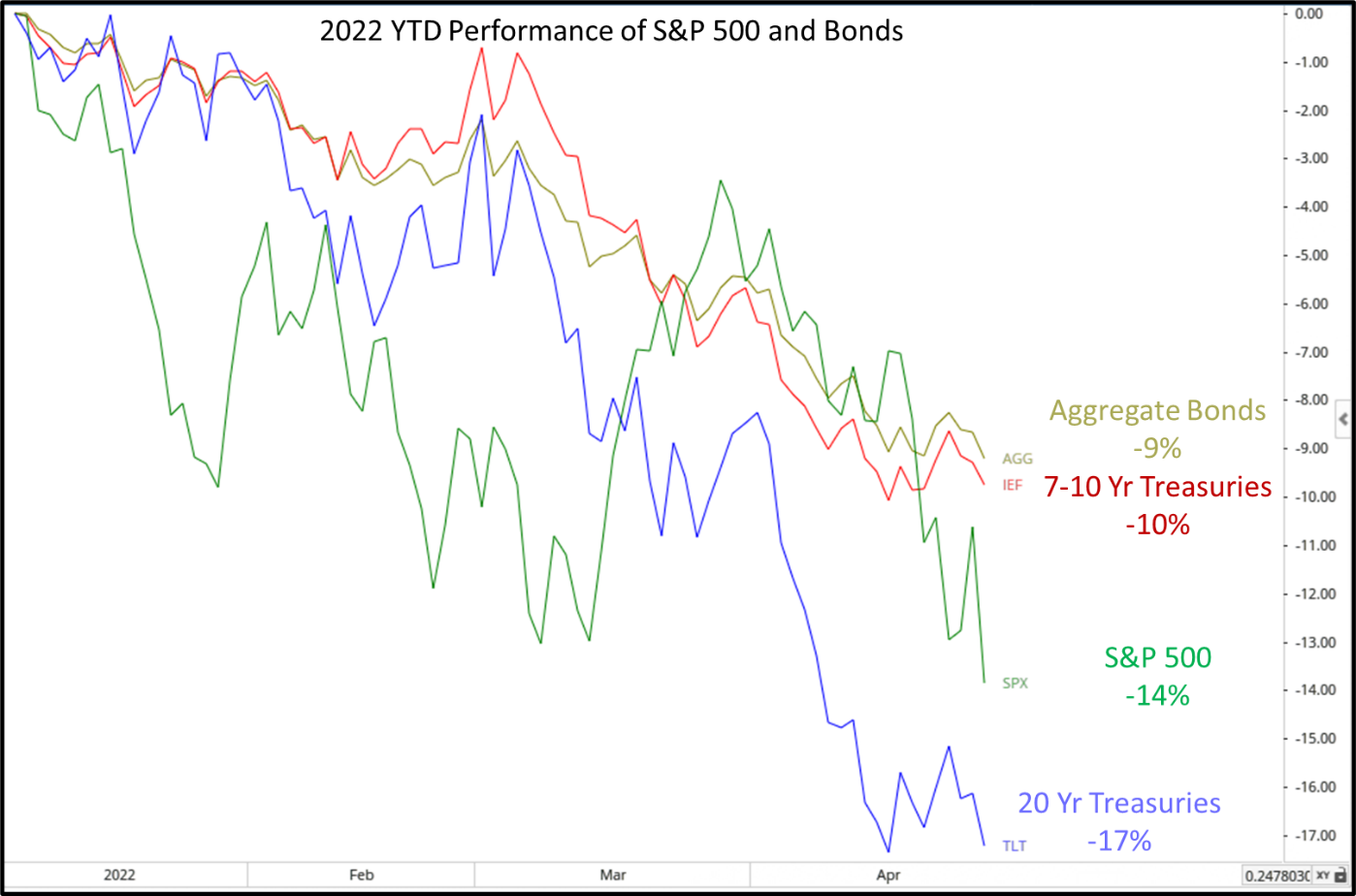

If 2022 has proven anything, it’s that broad diversification doesn’t always work. The traditional definition of a “conservative” portfolio has been anything but conservative. On Friday, the S&P 500 market index fell by -3.63%, which was the largest daily move (up or down), as the index put in a new low for the year. Twenty-year treasury bonds didn’t do much better, falling by -1.30% on Friday. Through Friday’s close, a conservative blend of 60% stocks and 40% bonds would be down about -12% on the year.

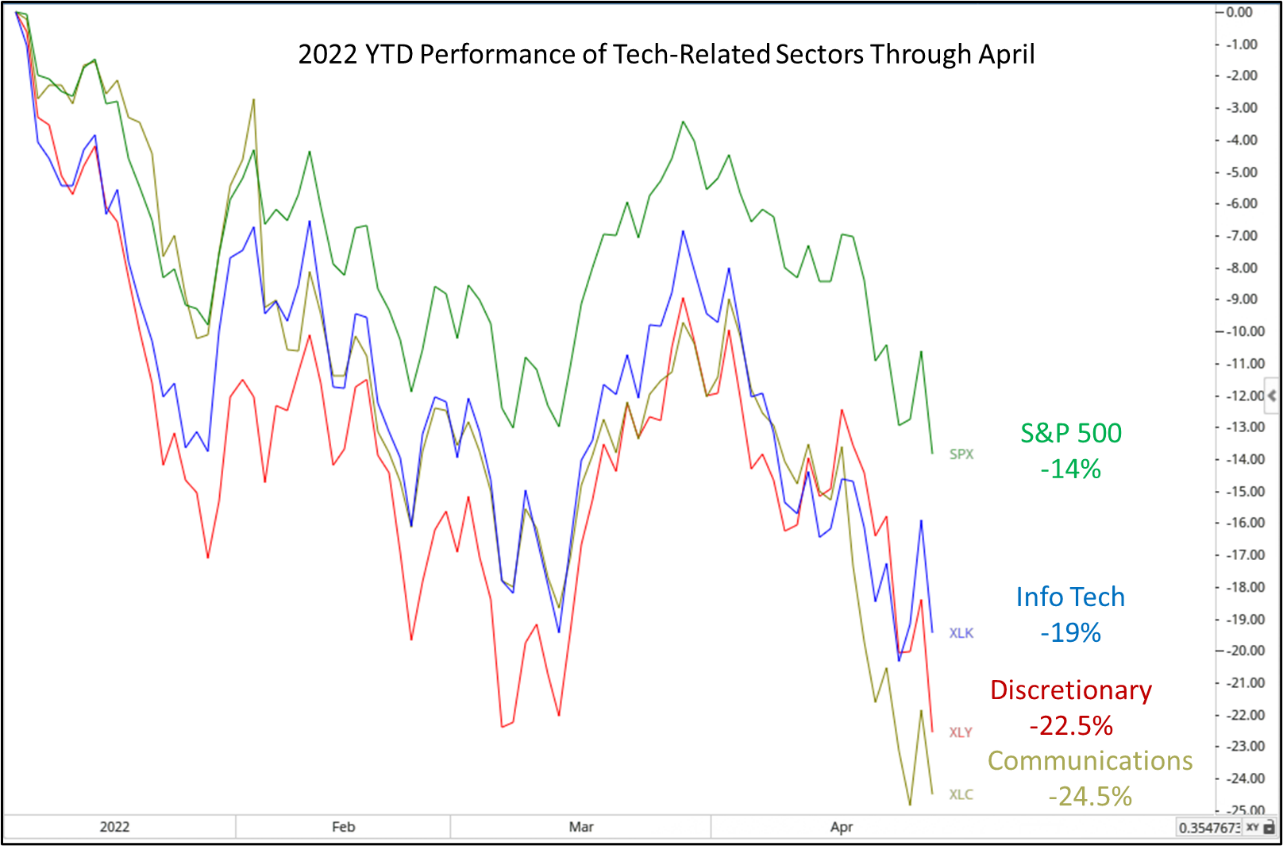

The S&P 500, often the benchmark for US equities is now down -14% year-to-date. The decline in US equities is mostly attributed to technology-related stocks. The Information Technology sector is down -19% YTD, Consumer Discretionary (Amazon and Tesla) is down -22.5%, and Communications is off by -24.5%. The sectors that have led the markets higher for the last several years, becoming the market’s largest components in the process, are now leading the market’s volatility.

Source: Optuma Technical Analysis Software

Traditionally, the risk in the markets is thought to be offset by holding fixed income, or bonds. Twenty-year treasury bonds are down -17% on the year. In otherwords, the conservative asset has been aggressive.

Why Are Both Stocks and Bonds Volatile?

Right now, stocks and bonds have high correlation and are both moving in the wrong direction. Not only is the risk in the markets increasing, but the risk in many diversified portfolios has increased substantially. Rather than mitigating portfolio risk, bonds have only increased it, and the expectation is that the risk in bonds will continue to increase.

Our Canterbury team produced and distributed a video on January 14th, 2022, discussing some of the inherent risks in both the equity and fixed income markets. The full-length video can be found below, but we will pull some quotes out.

Link To Video: “Technology and the State of the Markets”

Beginning at the 12:51 mark:

The problem that exists is that many investors are in balanced portfolios. So, they have stocks, which are going to be similar to the S&P 500 market portfolio, that are overexposed to technology, and they probably also hold bonds. In this type of environment, we know that inflation is through the roof and interest rates will probably go up, and therefore bonds will go down.

Since the time of publishing, that’s almost exactly what has happened. Stocks have generally gone down, led by the large technology stocks, and interest rates have gone up causing bonds to go down in price. Bottom line, a well-balanced portfolio has not behaved as such. Stocks and bonds have been highly correlated.

Bottom Line

According to Canterbury’s Market State indicators, this is a bear market. The traditional definition of a bear market is a decline from peak pricing of -20%. The S&P 500 has not yet crossed that line in the sand but is showing all the signs of being bearish– volatility is high and long-term and short-term indicators have turned negative. Technology-related sectors are in bear market territory, and other indexes like small cap stocks (Russell 2000) has long been in that bear market threshold. The point is that waiting until the S&P 500 declines by -20% to call it a bear market does very little to help investors. On the other hand, the big question becomes “what can investors do about it?”

The question of “what can you do about it?” is one the Canterbury seeks to answer. The markets are emotional. Do not let an emotional market inspire an emotional decision. Markets require systems and processes. In this type of environment, it is all about adaptive portfolio management.

We will end this update with another quote from the January 14th video, beginning at 14:05:

So going forward, what we know is that doing what traditional investing has done in the past is not going to work. The assumption is that if the stock market goes down, then bonds will go up… A conservative portfolio could end up being very risky. The answer to that is to use a process that looks at the reality of what is happening right now. The reality of what is happening now is that technology is beginning to show a sharp increase in volatility… and the rotation in leadership has been to more defensive areas like utilities, consumer staples, energy.

If the market continues to go down further, those areas will help, but there will be other areas and investment tools, like commodities or currencies or things that can benefit from bear markets like inverse securities. So, the key going forward will be to adapt and adjust to whatever this market throws at us and take a negative and turn it into a positive.

For more market trends, visit ETF Trends.