Will years of aggressive lending finally catch up with the U.S. economy at precisely the wrong time?

The U.S. economy is firing on all cylinders, with unemployment near record lows, labor force participation near record highs, and GDP growth and inflation moving along perfectly in line with the targets set by the U.S. Federal Reserve. Despite this rosy backdrop, signs of stress are appearing in one segment of the economy: regional banks.

Increasing Percentage of Leveraged Loans Among Regional Banks

According to a Moody’s survey of 38 regional banks, the percentage of leveraged loans at regional banks is increasing; 45% of regional banks expect their total amount of leveraged loans outstanding to increase over the next two to three years. Perhaps more concerning, nearly 50% of the outstanding loans held at these regional banks are unrated by Moody’s or S&P, reducing transparency for bank executives and investors. Overall, leveraged commercial loan exposure remains low at 3%, but the trend appears to be toward riskier credits, as banks struggle to compete with more aggressive non-bank lenders for business.

In addition to more leverage, there is some evidence that credit quality has started to suffer, leading to tighter lending standards. A recent survey by the Federal Reserve of 73 domestic banks found that in every loan category, a significant portion of banks expected to see loan performance “deteriorate somewhat.” These same loan officers surveyed indicated that their employers are beginning to exhibit a “reduction in risk tolerance” not seen in previous years.

This is classic “late-cycle” behavior by banks. When credit conditions start to deteriorate, banks begin to tighten lending standards, which can cause available credit to dry up right when the economy needs liquidity the most.

How is Sage Positioning for a Potential Credit Crunch?

At Sage, we are monitoring this situation closely. This trend will undoubtedly affect credit quality at the regional banks, but also has important implications for the overall U.S. economy.

Regional banks provide much of the lending to smaller businesses and the property development industry in the United States. If liquidity for these important growth engines begins to dry up due to concerns about credit quality caused by years of aggressive lending, the overall growth of the U.S. economy could begin to sputter.

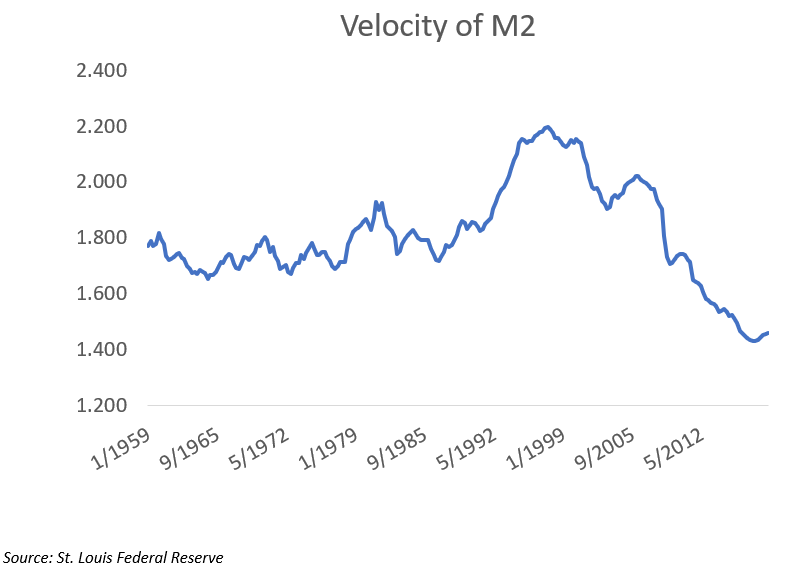

The velocity of the money supply in the U.S. has been declining for years, indicating that consumers are transacting less on each dollar of supply put into the system than they were 20 years ago. This means that as the Federal Reserve has pumped more and more liquidity into the system, there is a smaller marginal increase in spending per dollar added. Recently, the Federal Reserve has begun to shrink the size of their balance sheet, which has raised concerns that liquidity is drying up in the banking sector, which could lead to less lending by banks going forward. Sectors that may be vulnerable to a slowdown in grassroots lending growth are to be avoided. This includes capital goods, real estate development, and consumer products.

This somewhat precarious situation has made us concerned that the positive business cycle of the past 10 years may be coming to an end. Given this view, we believe now is the time to begin trimming more illiquid positions that have experienced outsized price performance.

This article was written by the team at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.