I’ve always thought the number one rule of investing was return on investment is highest when capital is scarce.

In other words, one should want to be the lone banker in a town with a thousand borrowers. An overwhelming demand for capital relative to the supply of capital implies that lenders set lending rates at undoubtedly profitable levels. However, if there were a thousand banks and only one borrower, then the over-supply of lenders would bid away the profitability of the one borrower’s loan and the borrower would get an extraordinarily cheap cost of capital. As in any economic event, it is simply the intersection of supply and demand that sets prices. In this case, prices are interest rates.

We’ve argued for some time that there is a bubble in long-duration assets, i.e., technology, innovation, disruption, venture capital, long-term bonds, cryptocurrencies, and other investments that incorporate longer time horizons into their valuations. The Fed artificially depressed long-term interest rates through their quantitative easing, and accordingly artificially inflated the valuations of assets priced off the long end of the yield curve. (Anatomy of a Bubble. https://rbadvisors.com/images/pdfs/RBA_Insights_Anatomy_of_a_bubble_09.21.pdf)

Bubbles misallocate capital

Financial bubbles can have a very detrimental economic effect because bubbles misallocate capital. Bubble sectors get too much capital (i.e., 1000 banks with one borrower), whereas the cost of capital is exorbitant for sectors that need capital investment (i.e., one banker in a town of 1000 borrowers).

Investors typically are very myopic during a financial bubble. They believe there is only a small universe of potential high returning assets. However, that myopia and misallocation of capital presents true investors with a broad range of investment opportunities with higher return on investment potential.

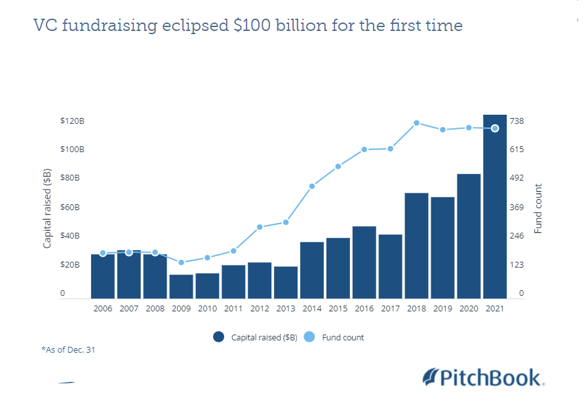

Today’s misallocation seems massive. Companies have had no trouble raising capital for space projects, but investors have little interest in solving the historic logistical dislocations here on earth. Chart 1 shows the record flows to venture capital.

Chart 1: Venture Capital Flows (2006-2021)

Source: Pitchbook

Energy appears to be a value story and…

A bullish story for Technology is the cash flow generation of the companies, but it seems as though that positive story is well discounted into the valuations of technology shares. On the other hand, few have highlighted the cash flow generation of the Energy sector and how valuations have not discounted that positive development.

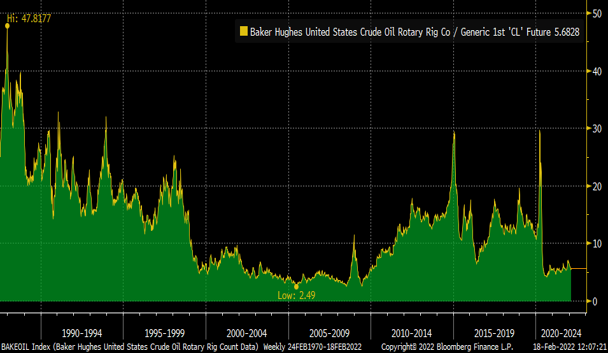

Unlike previous cycles of rising energy prices, energy companies are not significantly expanding capacity. Capacity in many cyclical industries tends to increase when commodity prices rise, and that was traditionally the story in the Energy sector. Energy companies would quickly expand capacity as commodity prices increased, which would sow the seeds of the cycle’s end as capacity eventually outstripped demand. Energy companies are showing tremendous capacity restraint despite the significant increases in energy prices.

Chart 2 shows the relationship between drilling rigs and the oil price (i.e., how many rigs does it take to produce a $1 of crude). Much of the downward trend in the chart is attributable to technological drilling advancements because drillers certainly don’t use the less efficient techniques of 40 years ago. However, that long-term trend does not explain today’s capital constraint relative to pre-pandemic levels. The ratio of rigs/oil is still roughly half of pre-pandemic levels.

The 2000s were the only period during which the ratio of rigs/oil was at similar levels to today’s, and the Energy sector was the best performing US sector for that decade.

Chart 2: Baker Hughes US Rig Count vs. Oil Prices (July 17, 1987 – Feb 18, 2022)

Source: Bloomberg Finance L.P.

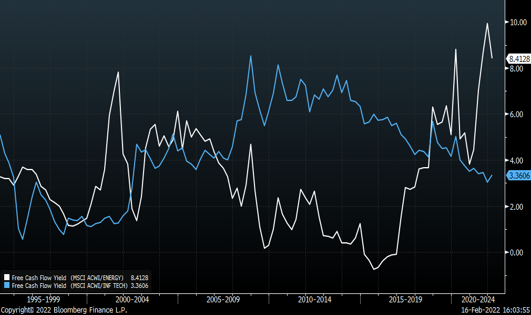

The sector’s conservative capital spending has meant greater cash flow to distribute to investors. Chart 3 shows the free cash flow yield of the energy sector. The FCF yield is about the highest in the last 30 years. Perhaps more important in light of the bubble in “innovation”, Energy’s FCF yield is more than twice that of the Technology sector. The last time the FCF yield of Energy was higher than Technology’s was also in the 2000s, which helped propel Energy to outperform Technology for the ensuing decade.

Chart 3: Free Cash Flow Yield: Global Energy vs. Global Technology

(Mar. 31, 1995 – Feb. 15. 2022)

Source: Richard Bernstein Advisors LLC., Bloomberg Finance L.P.

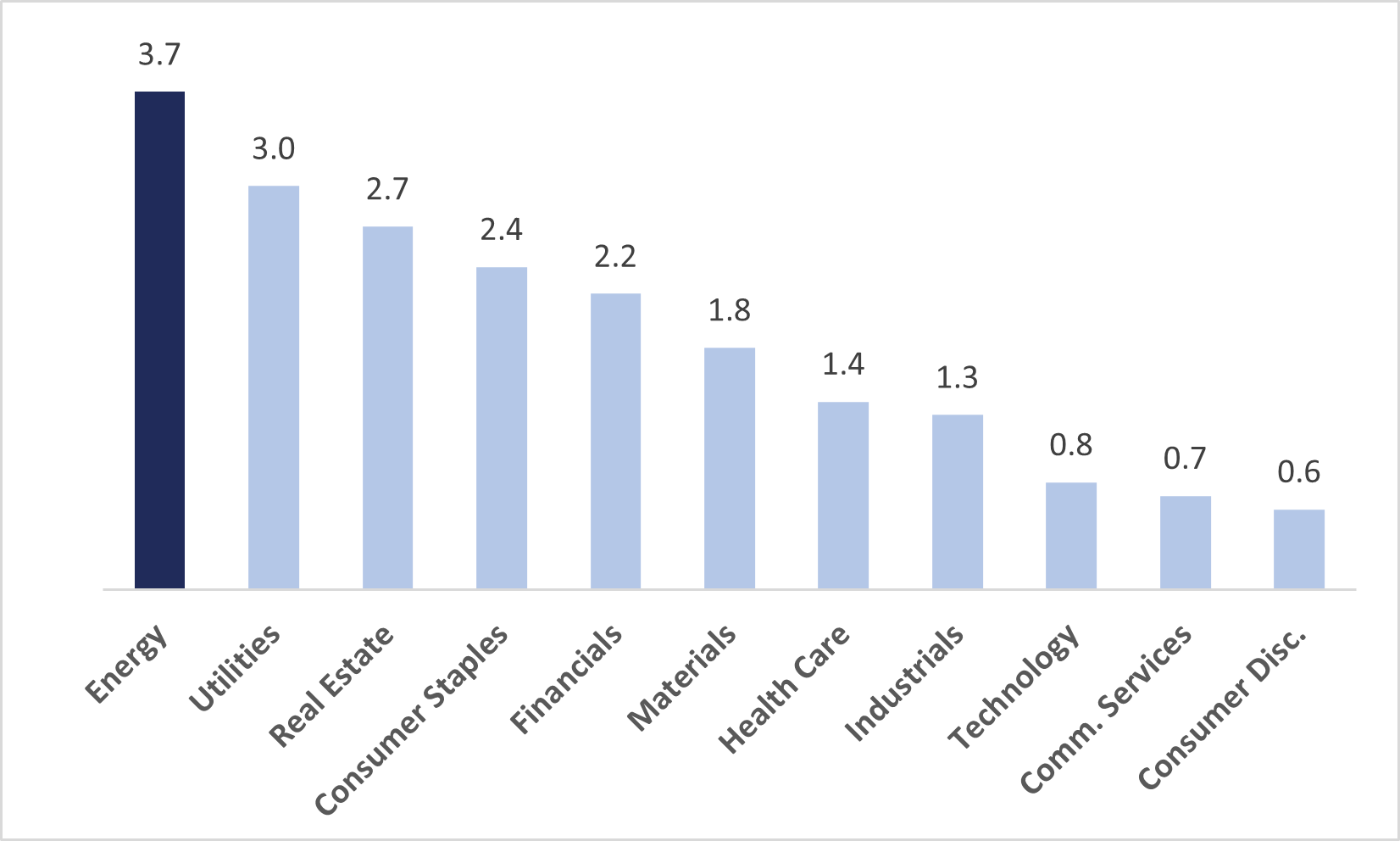

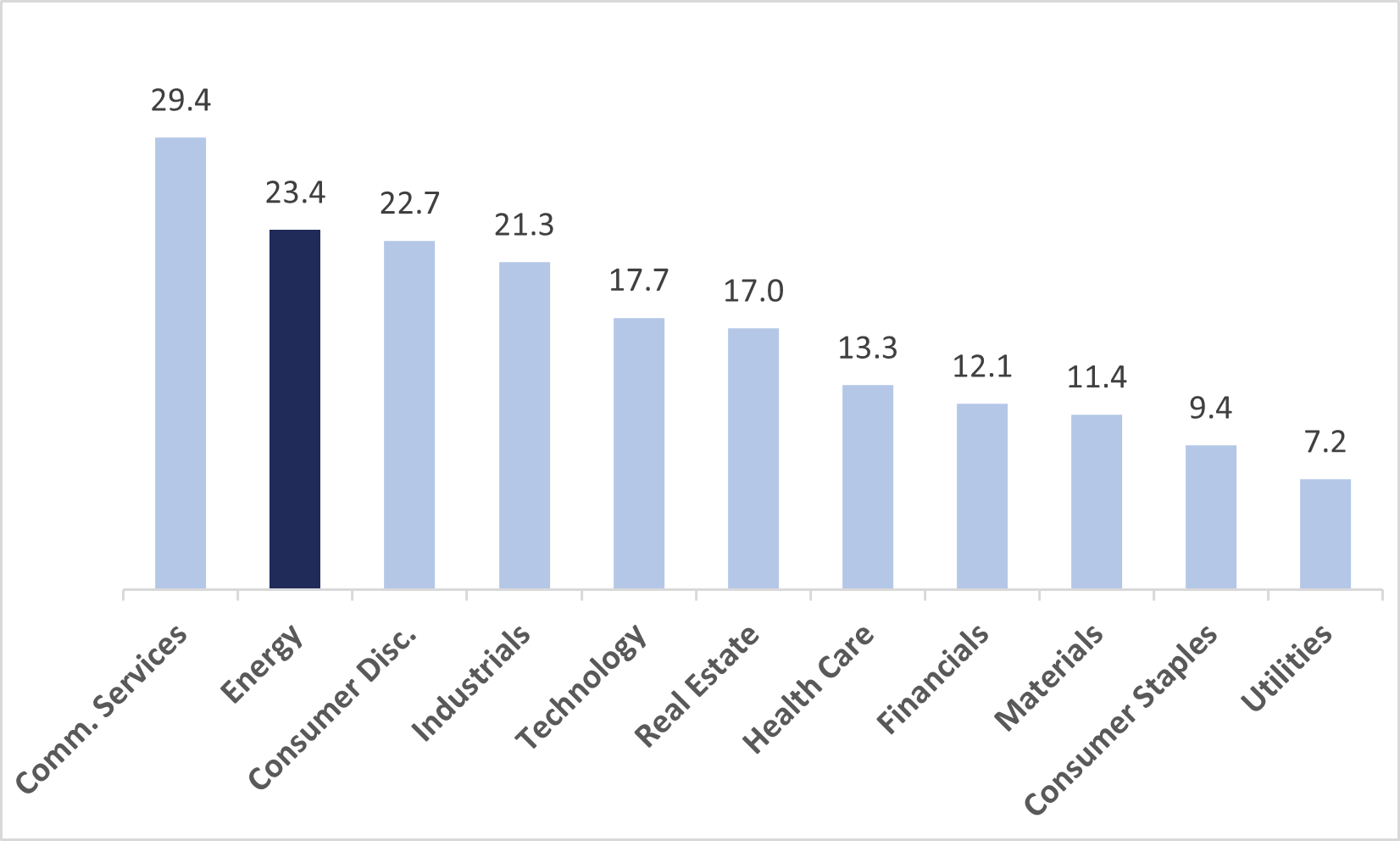

Free cash flow is a determinant of dividends and share repurchase. Accordingly, the Energy sector’s free cash flow has led it to offer the highest dividend yield of any US sector. (see Chart 4).

Chart 4: Dividend Yield by Sector as of Jan. 31, 2022

Source: BofA Equity Strategy

…Energy appears to be a growth story too!

“Growth” companies should by definition offer investors superior secular earnings growth relative to that of the overall stock market. If that characteristic is true, then the Energy sector qualifies as a growth sector.

Chart 5 shows the five-year projected earnings growth rates by sector derived by compiling analysts’ growth projections for individual companies (i.e., bottom-up forecasts). The Energy sector currently has the 2nd highest projected growth rate. In addition, its secular projected growth rate is meaningfully higher than is Technology’s.

Chart 5: Bottom Up Projected 5-Year EPS Growth as of Jan. 31, 2022

Source: BofA Equity Strategy

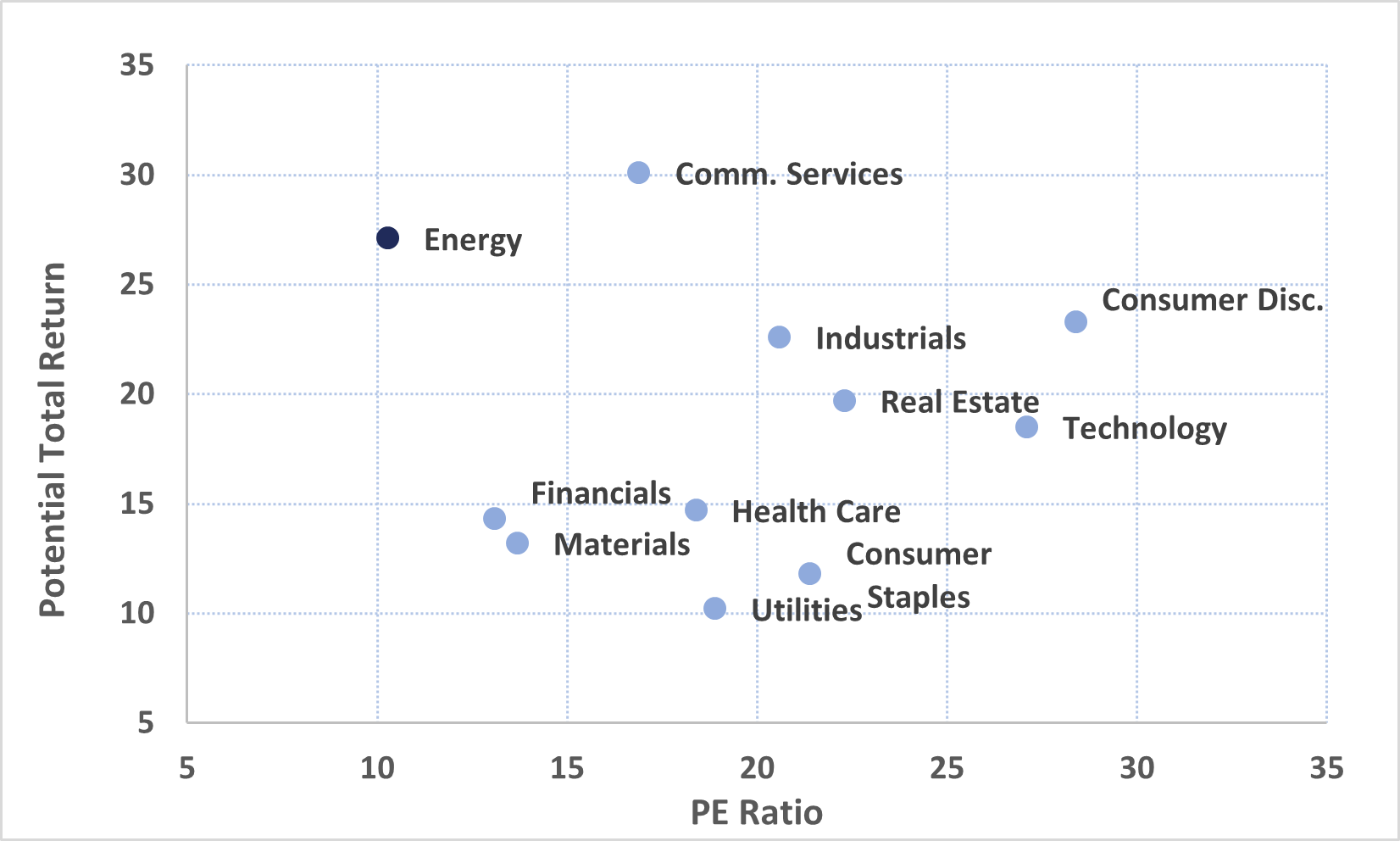

Growth + Value = Potential Return

Some equity investments offer income with less growth, whereas others offer growth with little or no income. History suggests that equities that offer both can be very attractive.

Many years ago, we posited that “potential return” was a function of the combination of dividend yield and projected long-term growth. That simple construct allowed investors to gauge the relative attractiveness of both growth and income investments in one framework.

Chart 6 shows the “potential return” (the addition of dividend yield plus five-year projected earnings growth rate) versus price/earnings ratio. The most attractive sectors within this framework at those with low P/E ratios and high potential return, which implies investors do not have to pay a lofty valuation to get superior return.

The Energy sector currently is the most “northwest” in the grid. It has the 2nd highest five-year projected growth rate and the highest dividend yield, but also has the lowest P/E ratio. For comparison, the Technology sector’s potential return” is in the middle of the range, but investors have to pay a very high P/E multiple to get that middling potential return.

Chart 6: Potential Total Return vs. PE as of Jan. 31, 2022

Source: BofA Equity Strategy

What about a recession?

The Energy sector is a very cyclical sector and energy companies are trying to reduce that cyclicality by conservative supply management. A recession that might significantly curtail demand is clearly a risk to our thesis because one can’t turn a cyclical industry into a stable one. Supply management can reduce cyclicality, but it can’t remove it completely.

However, we currently don’t think the chances of a full-blown recession are high enough to warrant us abandoning this theme. We remain overweight Energy, but are not blind to the sector’s cyclicality.

Although a recession would likely derail the shorter-term Energy story, a recession could actually augment the longer-term investment story. It would be very unrealistic to see energy capacity expand during a recession. Rather, history suggests energy companies contract capacity during periods of weak economic growth. Because supply is already very tight, a recession might simply further curtail production which could exacerbate supply/demand imbalances once the economy recovered.

Energy could be the next growth story

We continue to believe the Energy sector is a very attractive sector and could be the next longer-term growth story. The sector offers both yield and growth at a cheap price, and seems very attractive relative to sexier sectors that offer inferior fundamentals.