By Kimberly D. Woody, Senior Portfolio Manager

Japan has been largely dismissed for the better part of 20 years and for good reason. Following a massive debt bubble and demographic chasm, Japan entered into a period of economic stagnation. Back-to-back recessions persisted from 1997 to 2003 with a small respite during the height of the dot com bubble. Japan was caught in a liquidity trap with consumers refusing to part with cash for fear of deflation, lower rates or both – and the fear is self-fulfilling. Stagnation ensued. From 1991-2003, GDP grew a scant 1.14% annualized.

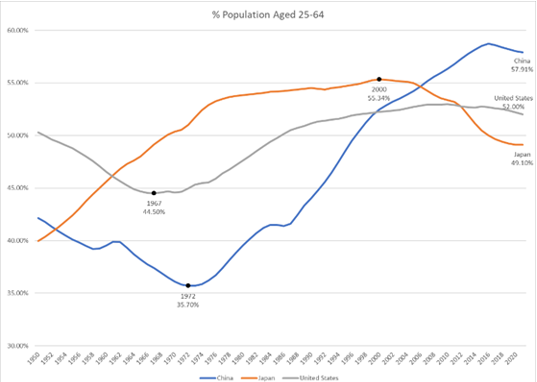

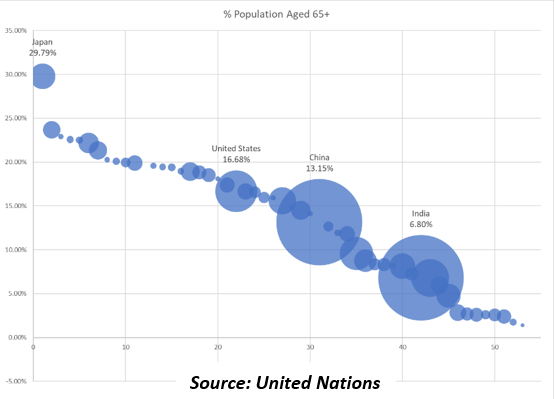

Regardless of how you calculate GDP, demographics play a key role. Economic growth depends on productivity gains and changes in the number of people in the workforce. Despite being technologically advanced, Japanese demographics thwarted any prospects of higher GDP growth. Japan’s cohort of people over age 65 has been rising precipitously post World War 2 and is the highest as a percentage of the population in the world save for the Kingdom of Monaco. The size of the working age population has been falling precipitously since its peak in 2000.

In an attempt to energize the economy, Japan turned to the three arrows of Abenomics – monetary easing, fiscal stimulus, and structural reform. Japan’s quantitative easing was aggressive in that the Bank of Japan (BOJ) actually got involved in purchases of stocks and bonds, and it was far more costly. Japanese debt to GDP stands now at 219.5% of GDP, the highest of any developed county by far and more in line with countries like Venezuela and Sudan. And the majority of the debt is owned by the BOJ.

Much like structural elements weighed for years on the Japanese economy, corporate reforms and easing demographic burden could revive the investment case for Japan. After another lost decade of false starts, the Tokyo Stock Exchange quietly initiated a policy to force companies trading below book value to “[back cast]from their future vision and move toward balance sheet management and cash flow management.” In other words, manage your capital and business with the goal of maximizing shareholder value. With half the companies on the Exchange trading below book value, there seemed to be significant opportunity for upside to equity values should the reforms drive meaningful change.

Unlike in the US, inflation has been a welcome development in Japan (+3.3% year over year in June). Skeptics point to supply chain disruptions following a later than average COVID re-opening, but wages have also been driven higher and governmental reforms are aimed at keeping them higher by making it easier for employees to change jobs. AI is poised to drive technological innovation and corporate and governmental reforms could certainly reignite a stagnant technology sector.

There are some obvious similarities between China now and Japan “then.” The size of China’s working age population appears to be on the wane (see chart above). China’s economy has been disproportionately buoyed by what is most certainly a real estate bubble. Unlike Japan, China is relatively unsophisticated in terms of technology and reliant upon the sheer size of its manual labor force. China is now facing weakening home sales, property investment, and consumer spending. GDP recently surprised to the downside. The Yuan is faltering but China is in no position to raise rates in the face of economic weakness. In fact, the People’s Bank of China or PBOC reduced two key lending rates this week sending the Yuan lower. Finally, the post COVID rebound has not resulted in the type of demand for commodities we would have associated with strong economic activity.

Japan’s economic growth in the 1980s morphed into multi-asset class struggles that lasted two decades. China’s economic progress of the 2000s set the stage for the challenges they are experiencing almost two decades later. Granted, China has the opportunity to avoid some policy mistakes that perhaps deepened and/or prolonged Japan’s difficulties. However, there does not seem to be an easy solution, and the all-too-familiar path that Japan suffered through is a very clear and present danger given the economies’ similarities.

While the picture we paint for China may not be so bullish, the case for Japan may be developing. From a geopolitical standpoint, and given China’s posturing towards Taiwan, we would prefer a strong Japan versus a strong China. But as our discipline dictates, we await cumulative weight of the evidence before reversing what has been a decades long underweight to the region.

Sources: Trading Economics, Wikipedia, World Population Review

GLOBALT is an SEC Registered Investment Adviser since 1991 and, effective July 10, 2013, remains a Registered Investment Adviser through a separately identifiable division of Synovus Trust N.A., a nationally chartered trust company. This information has been prepared for educational purposes only, as general information and should not be considered a solicitation for the purchase or sale of any security. This does not constitute legal or professional advice and is not tailored to the investment needs of any specific investor. Registration of an investment adviser does not imply any certain level of skill or training. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information may be required to make informed investment decisions, based on your individual investment objectives and suitability specifications.

Investors should seek tailored advice and should understand that statements regarding future prospects of the financial market may not be realized, as past performance does not guarantee and/or is not indicative of future results. Content may not be reproduced, distributed, or transmitted in whole or in part by any means without written permission from GLOBALT. Regarding permission, as well as to receive a copy of GLOBALT’s Form ADV Part 2 and Part 3, contact GLOBALT’s Chief Compliance Officer, 3400 Overton Park Drive, Suite 200, Atlanta GA 30339. You can obtain more information about GLOBALT Investments and its advisers via the Internet at adviserinfo.sec.gov, sponsored by the U.S. Securities and Exchange Commission.

The opinions and some comments contained herein reflect the judgment of the author, as of the date noted.

Investment products and services provided are offered through Synovus Securities, Inc. (SSI), a registered Broker-Dealer, member FINRA/SIPC and SEC Registered Investment Adviser, Synovus Trust Company, N.A. (STC), Creative Financial Group, a division of SSI. Trust services for Synovus are provided by STC.

Regarding the products and services provided by GLOBALT:

NOT A DEPOSIT. NOT FDIC INSURED. NOT GUARANTEED BY THE BANK. MAY LOSE VALUE. NOT INSURED BY ANY FEDERAL AGENCY

For more news, information, and analysis, visit the ETF Strategist Channel.