It’s time for our annual August report, “Charts for the Beach.” Each year we highlight five of our favorite charts we think consensus is currently overlooking. So, head for the beach, but be safe and heed the warnings about the critical lifeguard shortages. (Yet another sign the labor markets are historically tight!)

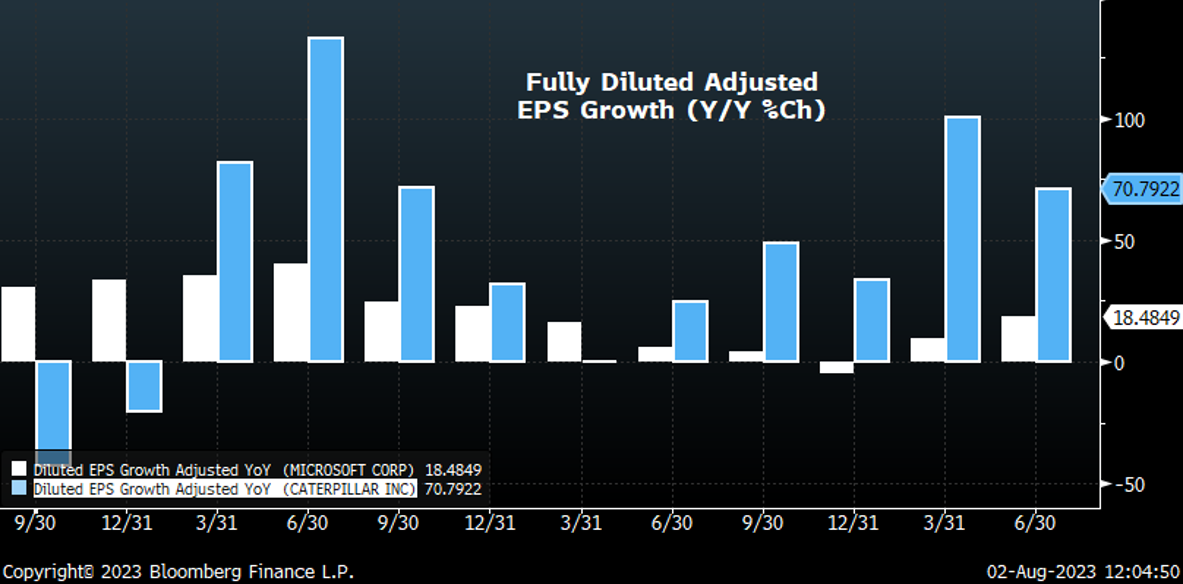

Are there really only 7 growth stories in the entire world?

We remain underweight the Magnificent 7 because we are not so bearish to believe that there are only 7 growth stories in the entire world. For example, Caterpillar’s earnings growth has been superior to Microsoft’s in nine of the last ten quarters. (Note: RBA may own both stocks in portfolios.)

Chart 1: EPS Growth: Caterpillar vs Microsoft (3Q 2020 – 2Q 2023)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

Downgrades do matter

If debt ratings changes don’t matter, then why are there debt ratings? Of course, they matter. They matter for companies, for municipalities, and for governments.

The 2011 US debt downgrade had a meaningful effect on the relative interest costs of US Treasuries and, because debt in the economy prices off government debt, raised the cost of capital for the entire US economy. No one cared because the absolute level of interest rates was low, but such omissions missed the important point that interest costs were unnecessarily high because of Washington dysfunction.

Prior to the 2011 downgrade, the yield spread between US Treasuries and German Bunds vacillated with neither country’s debt considered riskier for any length of time than the others. However, that all changed with 2011’s downgrade. US debt began to trade with a consistent 100-200 bps higher yield and has done so for the past 12 years.

One could argue how damaging the latest US debt downgrade might be, but it certainly won’t decrease the relative cost of capital for the US economy.

Chart 2: US vs Germany: 10-Yr Sovereign Debt Yield Spread (Aug. 29, 1993 – Aug. 2, 2023)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

Moving from cute wiener dogs in the metaverse (and AI?) to real productive assets

We continue to believe that long-term investment themes should focus on the combination of contracting globalization, the massive US trade deficit, and secular inflation, i.e., a focus on real productive assets.

The market continues to agree with us. Small and Mid-Cap Capital Goods companies have outperformed the Ark Innovation Fund (ARKK) since the ARKK came public in 2014.

Capital goods certainly aren’t as sexy as are innovative and disruptive technologies, but there remains a dire need to rebuild the US capital stock that the stock market seems to be appreciating.

Chart 3: Small and Mid-Cap Capital Goods vs. Ark Innovation Fund (Oct. 2014 – Jul. 2023)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. For index descriptions see Index Descriptions at end of document. RBA is not currently holding ARKK in any of its portfolios.

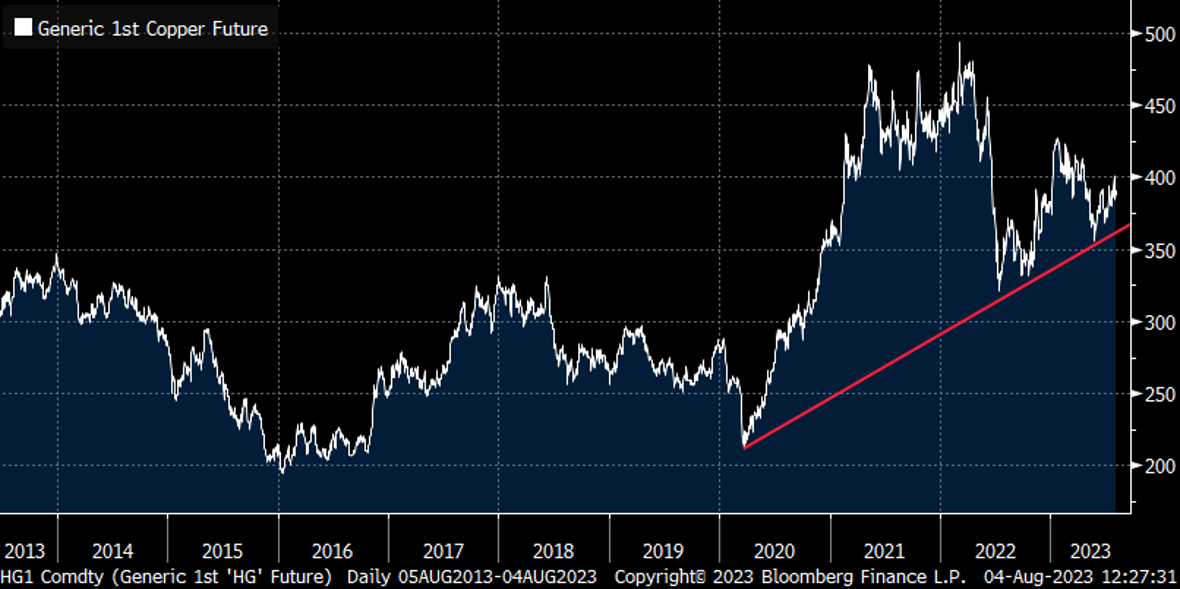

Something somewhere is fueling global growth

Some have called copper “Dr. Copper” because it tends to forecast the economy better than some (perhaps many?) economists. It appears as though Dr. Copper is once again disagreeing with the consensus economic forecast.

Consensus is US and global economic growth is slowing and the US is heading for a nice soft landing of the economy. However, copper prices have been rallying within the context of a what appears to be a multi-year bull market suggesting global growth is accelerating not slowing. Copper remains a critical component in our longer-term themes centered on real productive assets.

Chart 4: Copper Futures (Aug. 5, 2013 – Aug. 4, 2023)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P. For index descriptions see Index Descriptions at end of document.

Inflation expectations aren’t supporting the “Goldilocks” consensus

One might describe the current economic consensus as forecasting a “Goldilocks Economy,” i.e., one in which neither inflation nor growth is too hot nor too cold. That such a consensus has formed is understandable because Goldilocks economies have historically been good ones for financial assets.

Dr. Copper doesn’t appear to be agreeing with consensus, and now the Fed’s favorite measure of inflation expectations (the 5-Year 5-Year Implied Forward Inflation Expectations Rate) has jumped. It likely won’t take much higher inflation expectations for economists to remove their “inflation expectations are well-anchored” commentaries, which would certainly call into question the Goldilocks outcome.

These last two charts are raising a key question for the fall: What does the Fed do if the nominal economy actually accelerates?

Chart 5: Inflation Expectations (Aug. 5, 2018 – Aug. 4, 2023)

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P.

For more news, information, and analysis, visit the ETF Strategist Channel.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P Small Cap Capital Goods: The S&P 600 Capital Goods Industry GICS level 2 Index. S&P Global’s Smallcap Capital Goods Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1993.

S&P Mid Cap Capital Goods: The S&P 400 Capital Goods Industry GICS level 2 Index. S&P Global’s Midcap Capital Goods Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1990.

ARK Innovation ETF (ARKK): The ARK Innovation ETF is an actively managed exchange-traded fund incorporated in the USA. The Fund will invest in equity securities of companies relevant to the theme of disruptive innovation. Relevant themes are those that rely on or benefit from the development of new products or services in scientific research relating to Genomics Revolution, Web x.0, and Industrial Innovation.

Copper: Comex Copper Futures: Copper Futures contract (HG) offers the ability to deliver or take delivery of Grade 1 electrolytic copper cathode in a timely, transparent and efficient fashion at CME Group approved and regulated facilities located throughout the United States. Copper market participants across the board use COMEX Division high-grade copper futures and options to mitigate price risk, and the copper contracts are used as investment vehicles, as well. For this specific contract, the pricing is scaled by 100 in order to show greater precision for both the futures and options. https://www.cmegroup.com/trading/metals/base/copper_contract_specifications.html