S&P 500 Posts Best Q1 in 5 Years

S&P 500 Posts Best Q1 in 5 Years

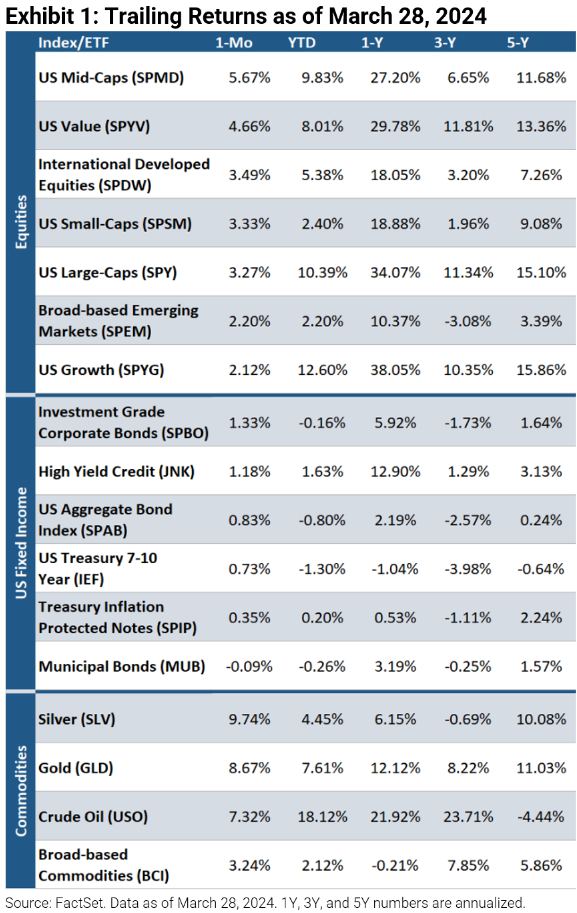

Despite still-elevated inflation and rate cut uncertainty, all three major stock market indices posted gains in Q1 2024 amid a tight labor market, economic strength, a continued earnings recovery, and AI optimism. The S&P 500 returned 10.6% for the quarter, notching its best Q1 performance since 2019. US growth (+12.6%) was among the best performers, followed by US large-caps (+10.4%) and US mid-caps (+9.8%). Bonds were mixed as 7-10 year US Treasuries (-1.3%) and the US Aggregate Bond Index (-0.8%) were down while high yield credits (+1.6%) and Treasury Inflation Protected Notes (+0.2%) rose. Commodities fared well as crude oil (+18.1%), gold (+7.6%), silver (+4.5%), and broad-based commodities (+2.1%) all posted positive returns.

Fed Continues to Forecast Three Cuts

The Federal Reserve kept interest rates unchanged at the March FOMC meeting, leaving the fed funds rate at the 5.25–5.50% range. Recent inflation readings for both January and February have come in above expectations, causing the bond market to slash its start of year rate cut forecast from six 25 bps cuts to just three. However, Fed Chairman Jerome Powell expressed the hotter inflation data has not changed Fed’s view on the broader disinflation trend. “I think they haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes bumpy road toward 2%,” Powell stated. Market participants were relieved that the updated median dot plot remained unchanged, still forecasting three cuts for the year, as there was anticipation one would be removed. The updated Summary of Economic Projections also revealed that the Fed expects real GDP to grow 2.1% in 2024, up from the December estimate of 1.4%, as the US economy remains resilient. Moreover, when asked if continued strength in the labor market would alter the Fed’s path, Powell responded, “Strong hiring in and of itself would not be a reason to hold off on rate cuts.” Per the CME FedWatch Tool, there is currently a 61% chance that the first cut will occur in June.

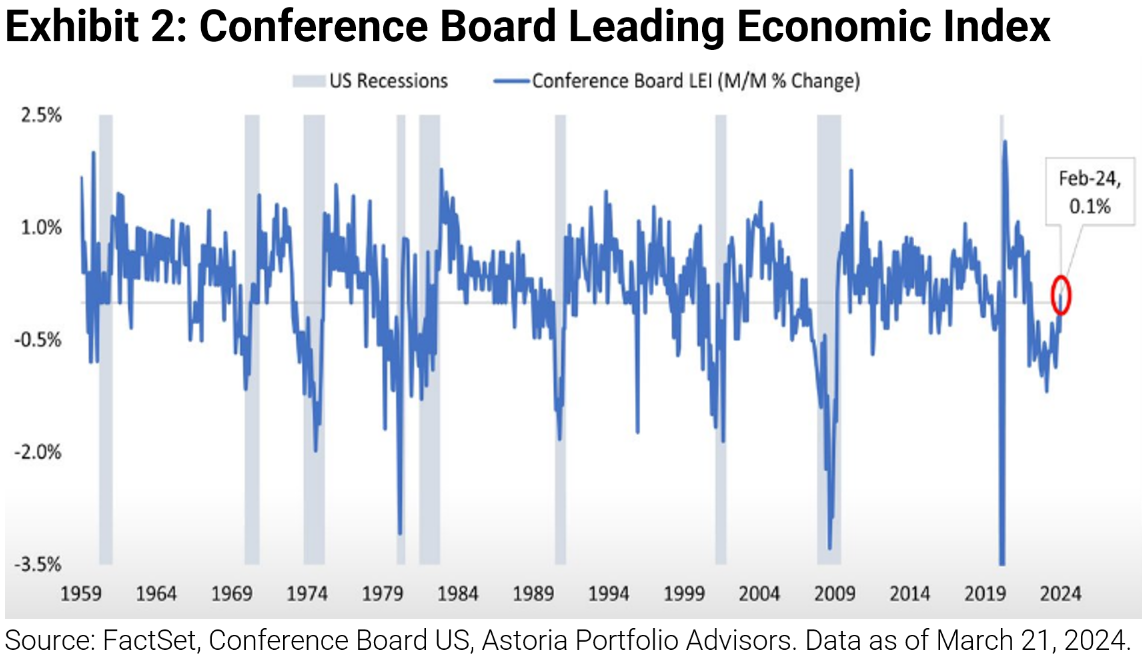

Leading Indicators End Streak of Declines

The Conference Board Leading Economic Index, designed to signal early indications of turning points in the business cycle, beat estimates in February and posted its first monthly increase since February 2022.

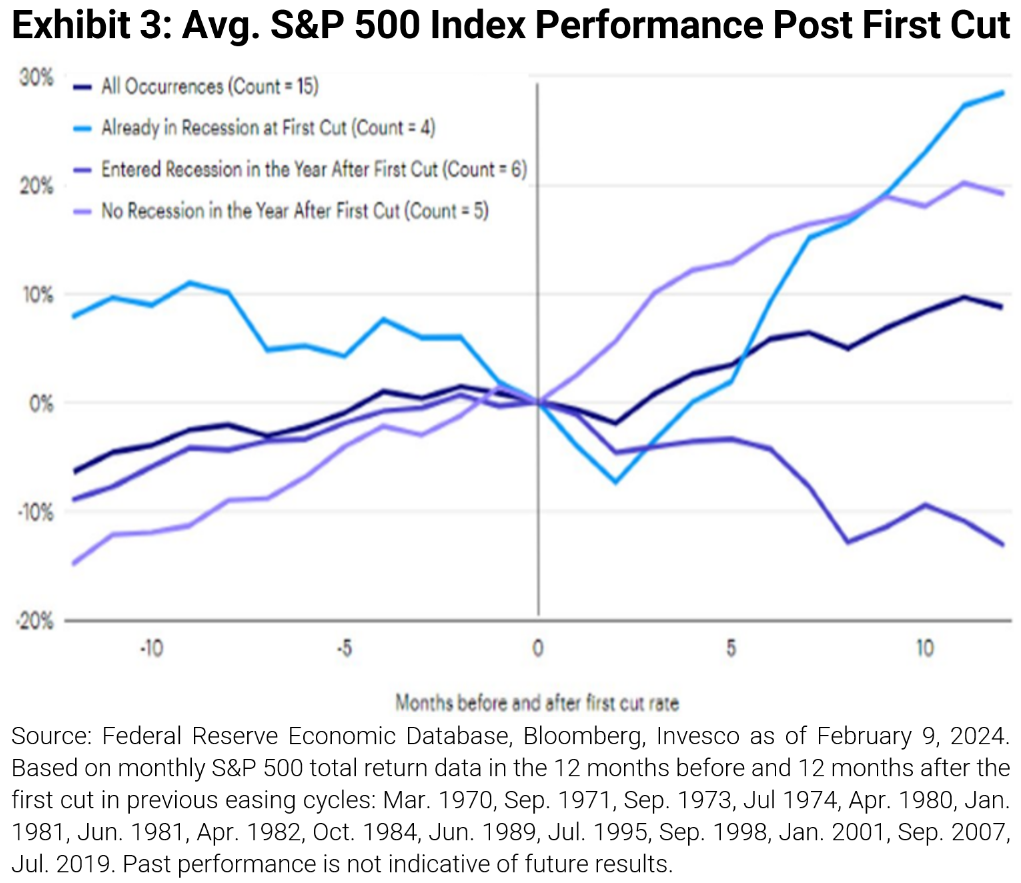

S&P Performance Over Past Cycles

When observing the S&P 500’s performance over past Fed easing cycles, the index tends to post positive returns in the months after the first rate cut, absent a recession (see light purple line below). Will it take the same path this cycle?

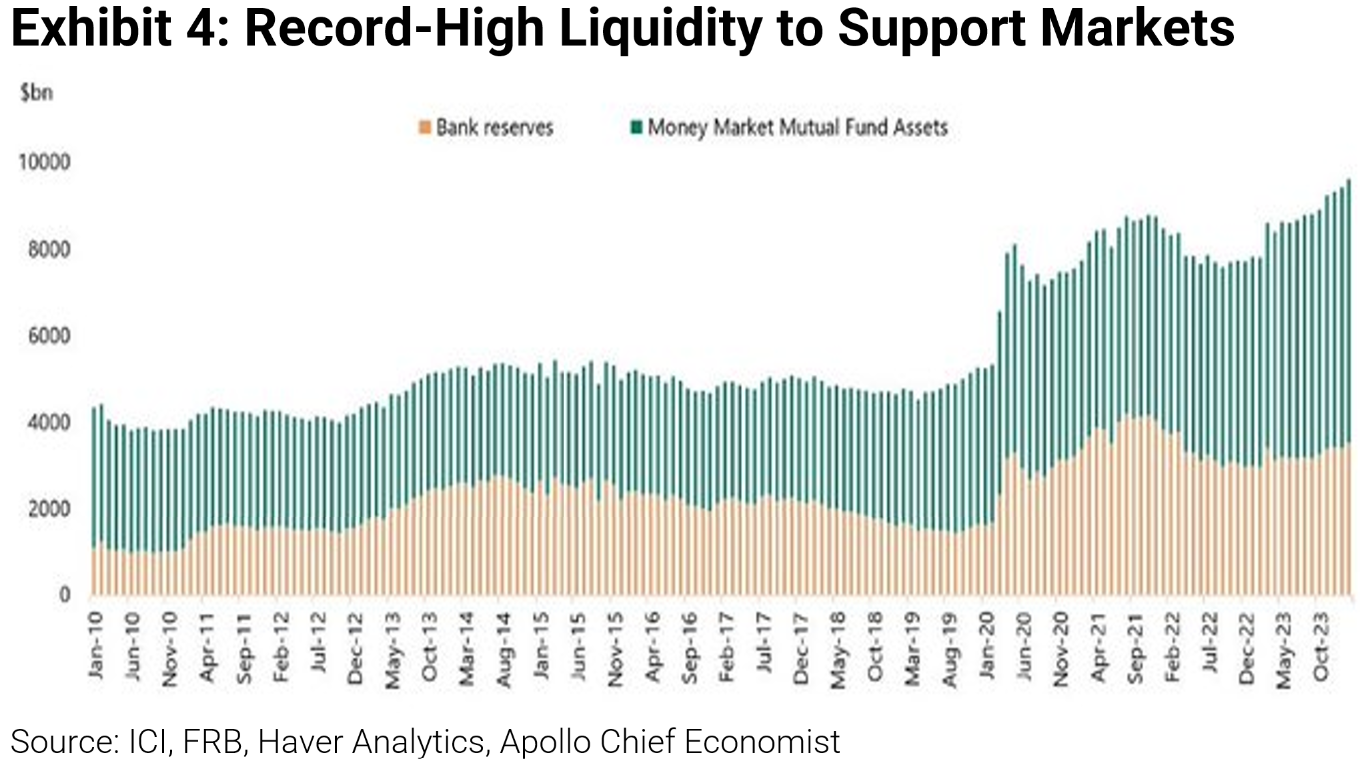

Liquidity Catalyst for Equities and Credit?

Higher interest rates have significantly increased allocations to money markets and bank deposits. When combining both, record high levels of liquidity exist, and funds in these areas are likely to make their way into equities and credit once the Fed cuts.

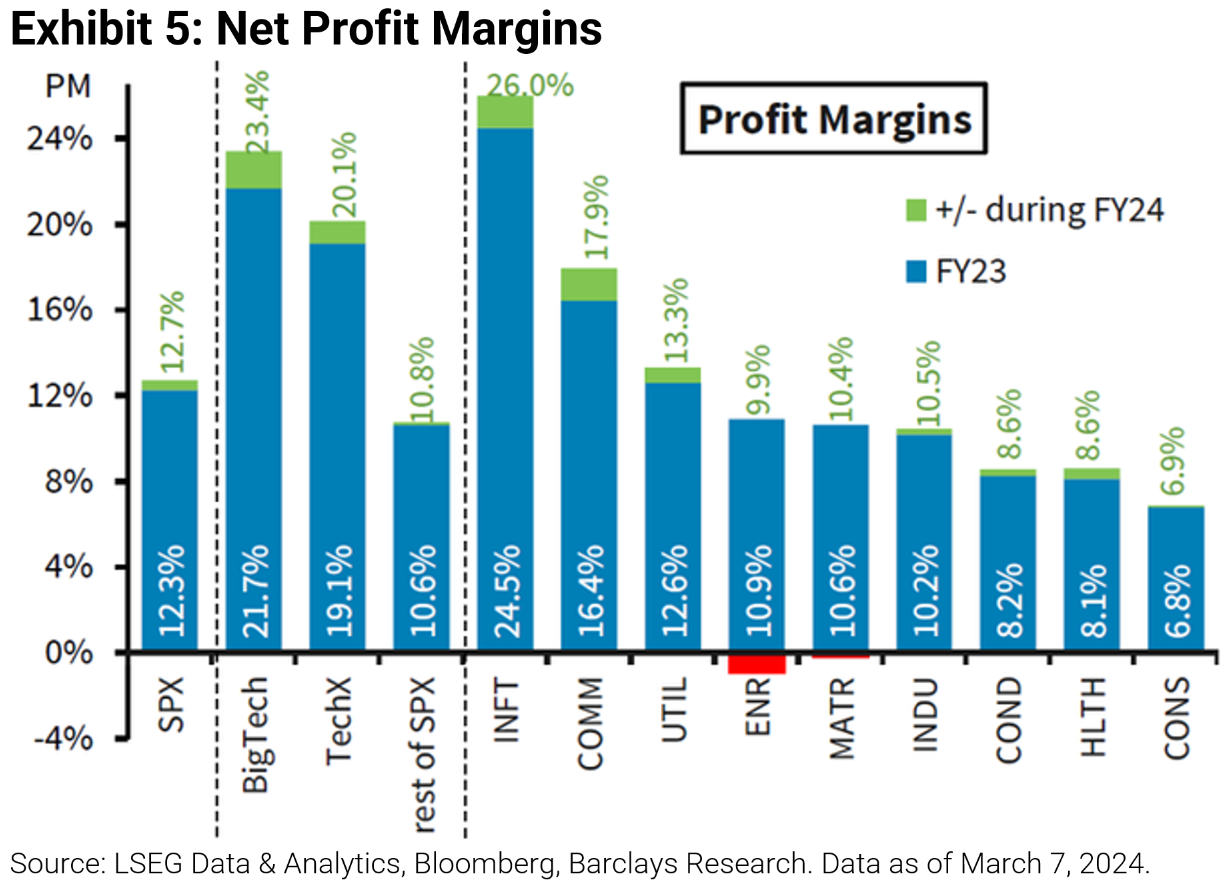

How Profitable is Technology?

The technology sector’s net profit margin is appealing at approximately double that of the S&P 500. However, as market-cap weighted strategies pose elevated concentration risk, it may be an appropriate time to consider owning such stocks in an equal-weighted manner.

Why are we Bullish? Better Margins, Earnings Recovery, and an Accommodative Fed

As written in our December commentary, we entered 2024 more bullish than we’ve been in the last 2 years. We believe better margins (due to AI-enhanced productivity + lower inflation), an earnings recovery, and an accommodative Fed will be catalysts for equities, and we think these dynamics will continue to provide support throughout 2024.

In the past few years, the market has dealt with aggressive rate hikes, rampant inflation, fear of recession, and an earnings recession. Those variables have dramatically improved and, in some cases, have reversed. Inflation has eased (granted, not conquered), the recession that seemed imminent now appears less likely to take place, and we’ve experienced two quarters of earnings growth. Additionally, many of the various economic indicators we monitor are now inflecting higher.

Hence, we are overweight equities, underweight alternatives, prefer credit over rates, and are running the highest beta in years.

Within equities, we prefer US stocks. Our preference is the US quality growth factor. For the first time in years, we find the technology sector appealing as net profit margins and PEGs for the sector are attractive. We are utilizing various equal-weighted strategies, which are by nature constructive on markets as they tilt towards mid-cap stocks (and away from the mega-cap stocks, hereby incurring tracking error). Recall that we began using equal-weighted strategies in our ETF portfolios in August 2023.

Moreover, we remain bullish on inflation sensitive/real assets, specifically industrials, energy, and materials. They maintain cheap valuations, have the potential to benefit from resurging inflation and deglobalization, and are significantly under owned versus history.

In the alternatives space, we also still find gold attractive as uncertainty around rate cut timing remains and the asset has historically posted positive returns in the months after the first rate cut.

For more news, information, and analysis, visit the ETF Strategist Channel.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, JNK, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, TLT, and LQD on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.