Will economic fundamentals support the new wave of optimism?

By the BCM Investment Team

Market running ahead of fundamentals.

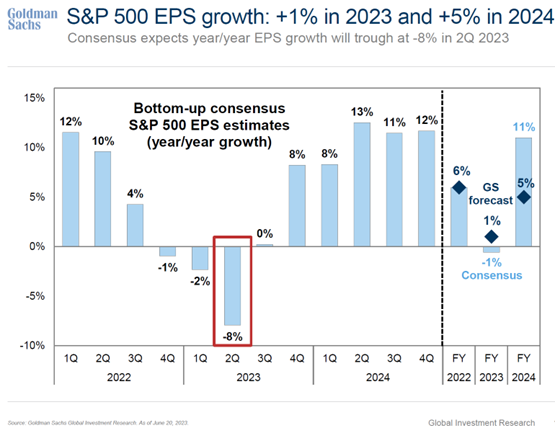

The prospect of an AI-fueled investment cycle as well as strong May jobs numbers propelled the market higher in Q2. Although we believe that many companies have already re-calibrated for a changing economic environment and will stand to benefit once growth resumes, there is little evidence yet of such growth.

We believe the strong appreciation in stock prices is well ahead of the fundamentals in most economic sectors. [1]

With Q2 earnings season at hand, many companies have to “prove” (justify) the runup in prices with the prospect of improving fundamentals later in the year.

AI may be overhyped.

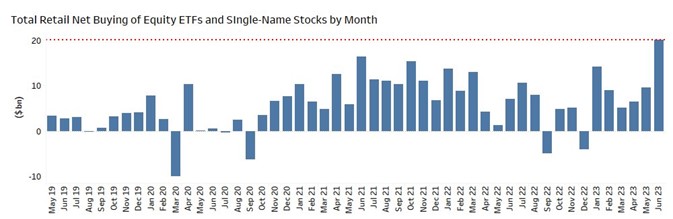

Nothing gets retail investors excited like a good growth story, and AI has delivered in spades. Retail investors returned to the market in mass in Q2, helping fuel the rally in stocks and giving us some unease about the current market despite the lack of overall volatility.

Source: Twitter; @rsandler21969. TAQ, Eminence Capital, June 23, 2023.

As software engineers, machine learning experts, and technology history buffs, we believe the investment buzz around “Generative AI” is considerably overhyped and overpriced. To us, semiconductor and software-based innovation has been the driving force of the economy for the last four decades, starting with the invention of the personal computer, with subsequent growth spurts driven by the invention of the internet, and later the mobile smartphone and the development of “apps” for everything.

In this light, Generative AI is just the latest incremental enhancement of software. The AI applications introduced so far simply automate something a human is already doing, rather than introducing radically new capabilities—as did the automobile, airplane, telephone, computer, internet, and smartphone, which revolutionized economic and social life. Many leading technology companies have already been incorporating AI tools for years, but consumers are seeing them for the first time with the release of chatbots such as Open AI’s ChatGPT and Google’s BARD. While the output of these products initially feels like magic, the applications remain incremental rather than transformational, and there is evidence some commercial interest has begun to wane despite their initial astounding popularity.

Interestingly, within the same quarter, Apple showcased perhaps the largest technology hardware innovation since the iPhone: the Vision Pro. While the product is far from mass market for now, and the hype was overshadowed by “AI”, Augmented and Virtual Reality also have the potential to change the way humans interact with computers and may offer another answer to the question of what innovation will drive the next generation of economic growth? Perhaps the real AI revolution will be a result of combining AI technology with hardware to create new real-world applications.

The unshakeable market for new homes.

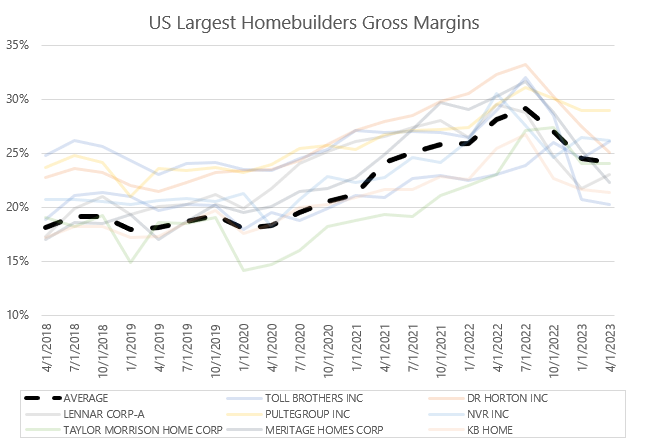

One area where strong equity performance has not run far ahead of the fundamentals, but alongside them, are the homebuilders. The lock-in effects of a huge swath of homeowners with average mortgages 3% or more below prevailing 30-year fixed rates have continued to keep supply of existing homes historically low. As a result, new homes (produced by Homebuilders) continue to be the only game in town for prospective buyers. Despite the average 30-year mortgage rate rising in the second quarter, many homebuilders are finally seeing their order books begin to increase again. Low overall inventories coupled with continued demand has kept overall home prices up while building costs have begun to fall, allowing homebuilders to continue to earn the historically high margins they saw in the early post-COVID era.

Source: Bloomberg. Data if for the largest 7 homebuilders by market cap for the period 4/30/2018 through 4/30/2023.

Source: U.S. Census Bureau and U.S. Department of Housing and Urban Development, New One Family Houses Sold: United States [HSN1F], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/HSN1F, July 7, 2023.

While our strategies initially gravitated towards the homebuilders as a value investment after the sector had sold off aggressively on the expected impact of higher rates, they may now be beginning to look more like momentum and represent a unique economic and market story. We believe the fundamentals support this market behavior as the equities remain inexpensive, and the longer-term two-pronged thesis of demand from demographics (millennials at homebuying age) and supply restricted from years of post-2008 underbuilding remains intact.

Is cash really on the sidelines?

While we believe consumer balance sheets are in great shape in aggregate, we are skeptical that the significant assets in money market funds represent “dry powder” for the equity market. Since the Federal Reserve sent interest rates to zero in the wake of the 2008 financial crisis, many traditional savers and retirement funds were forced to over-extend into risky equities in order to earn a meaningful return to achieve their financial goals. With short-term interest rates back to 5%, conservative investors can finally earn a meaningful return in traditional fixed income vehicles. Likewise, the balanced 60/40 portfolio offers an attractive risk-reward profile. So, the cash “on the sidelines” may be where it rightly belongs for the time being.

Where is China?

Many, including us, expected a boost to global economic growth from China’s re-opening. So far there is very little evidence of this—both imports and exports are down, the youth unemployment rate is staggeringly high and outbound travel remains heavily subdued despite restrictions being lifted. This has likely been the major driver of lower global oil prices, as China was expected to be an incremental source of demand.

A lack of exciting near-term investment opportunities.

For a multi-year horizon, we continue to like technology (XLK), semiconductors (SOXX), home builders (ITB), electrification plays (GRID) and the pharmaceutical companies leading the way with revolutionary obesity drugs (Lilly and Novo Nordisk) where the growth stories are robust. However we and our systems are struggling to find additional “table-pounding” ideas in the near term.

While the down and out Banking and Real Estate sectors may offer a good opportunity for carefully researched, highly selective value investing, we are wary of “catch-up trades” where investors aim to express a bullish view simply by buying the sectors which have recently lagged without a supporting economic thesis. [2]

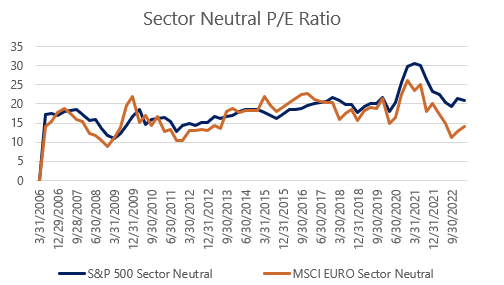

While the positioning of our strategies is clearly defensive, one area of opportunity percolating is in foreign equities. Historically European stock indices have been substantially cheaper than their U.S. counterparts, but much of this differential was justifiably driven by their lack of large Technology companies. When comparing European and U.S. equities on a sector neutral basis, their valuation differential looks historically anomalous as it stands today. This may present an area of opportunity for our global models if domestic equities cease to extend their current rally.

Source: Bloomberg. Data for GICS 9 Sectors Equal Weighted from 3/31/2006 through 3/31/2023

Source: JP Morgan Guide to the Markets Q3 2023. Data sources: FactSet, MSCI, J.P. Morgan Asset Management.

Positive Virtuous Wealth Effect

One place for optimism is simply our continued belief that “wealth effects” are a larger driver of economic activity than they were in the past. At the beginning of the year, we felt investors were overly pessimistic based on our belief in the rapid adaptivity and resulting resilience of the U.S. economy. The surprising resilience of the economy and U.S. consumer year-to-date has now spurred a $6 trillion rise in the value of U.S. stocks. This incremental wealth could fuel further consumer spending and stock market gains.

Prospective Risks (Adverse Developments)

- Resumption of student loan payments may slow economy.

- Vacant Commercial Real Estate might trigger a banking problem.

- The high expectations for AI to bolster growth and profit might fail to materialize.

- Further deterioration in the US/China relationship.

- Inflation is persistent and cuts into consumer spending. Central Banks hike further.

- Rapid interest rates begin to have larger overall effects after excess savings run out.

- Federal Reserve breaks something else or unforeseen.

- Residential housing market is disrupted perhaps due to recession, housing turnover is forced up due to layoffs or foreclosure, and home prices fall in line with the prevailing interest rates, resulting in a large negative wealth effect.

- High interest rates and bloated government debt ($100K per person) weigh down economy as fiscal support is removed.

Prospective Positive Developments:

- Inflation drops quickly. Interest rates fall. Economy and asset values surge.

- US/China relationship improves.

- Disruptive innovation akin to smartphones which creates new markets or drastically lowers costs or improves lives (e.g. better, cheaper EV batteries, wearable healthcare technology, obesity drugs)

- Clever solution to Office Real Estate problem.

- Cost cutting measures many companies undertook materialize as economic growth continues to march forward.

What’s next?

While we were happy to see the Fed pause, we think the market may need to pause as well in order to re-calibrate. Many issues remain unresolved, and the second half of the year will be a “show-me” period for businesses which now have higher equity values based on the prospect of improving fundamentals. Headwinds remain: Potential problems in real estate where properties face both a large re-finance risk as well as lower office occupancy in cities appear unresolved. Consumers continue to wind down their excess savings, which will eventually cease to boost aggregate consumption. Conversely wealth effects may begin to reignite spending for big ticket items, and thus far the economy has been more resilient than nearly anyone would have forecast.

A year ago we urged investors to stay the course in turbulent equity markets, stating that the odds were typically in equity investors’ favor after such bleak periods of performance. We would reiterate that same message now that markets have recovered much of their losses. The current market behavior (low volatility, high beta outperforming low beta) is exactly what one would expect to see in either a new bull market or the later stages of a bear market rally, posing a difficult risk reward proposition to investors. Given our investment flexibility, we hope to identify timely risk-appropriate opportunities in any market scenario.

For more insights like these, visit BCM’s blog at blog.investbcm.com.

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures:

Copyright © 2023 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC

125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)

[1] Some of the most disconnected examples are within the Semiconductor sector. Memory maker Micron is trading higher on earnings reports that are the worst in company history. Investors seem to be increasing their investment time horizon and/or raising their earnings expectations for the second half of the year (in this particular case speculating on a boost in sales from new AI demand).

[2] We’ve purchased several mortgage REITS and regional banks in our fundamentally driven strategies. Notably those with high trailing dividend yields yet manageable office exposure paired with strong management teams which we believe can navigate the dislocation