By: BCM Investment Team

From time to time, we find it useful to go back and read our past quarterly letters with the benefit of hindsight. We feel that the 1-year anniversary of the Covid-19 induced bear market is one of those times. A year ago, we wrote about the fastest bear market in history, a record high in the VIX (the CBOE Volatility Index), a massive oil market shock, and unparalleled volatility in the bond markets. We also wrote about the health of the U.S. consumer entering 2020, swift action by the U.S. Federal Reserve, and unprecedented fiscal stimulus to keep the economy afloat despite a public health induced shutdown. At the time, we were optimistic that coordinated fiscal and monetary stimulus could blunt the ensuing recession but worried that the virus would impact society for longer than most expected.

A year later, vaccine development should render the latter point moot, leaving us with an economy that has been primed with ample fiscal and monetary stimulus and is beginning to re-open. Increasing economic activity is beginning to show up in economic indicators such as the ISM Manufacturing and Services Purchasing Managers Indices (PMIs), which both recently recorded their strongest readings in decades. Additionally, there’s no shortage of optimism, as evidenced by the Conference Board’s Consumer Confidence Expectations Index®—which reached its highest level since July of 2019—and the Measure of CEO Confidence™, which reached its highest level since the first quarter of 2004.

Source: Bloomberg, from 4/5/21

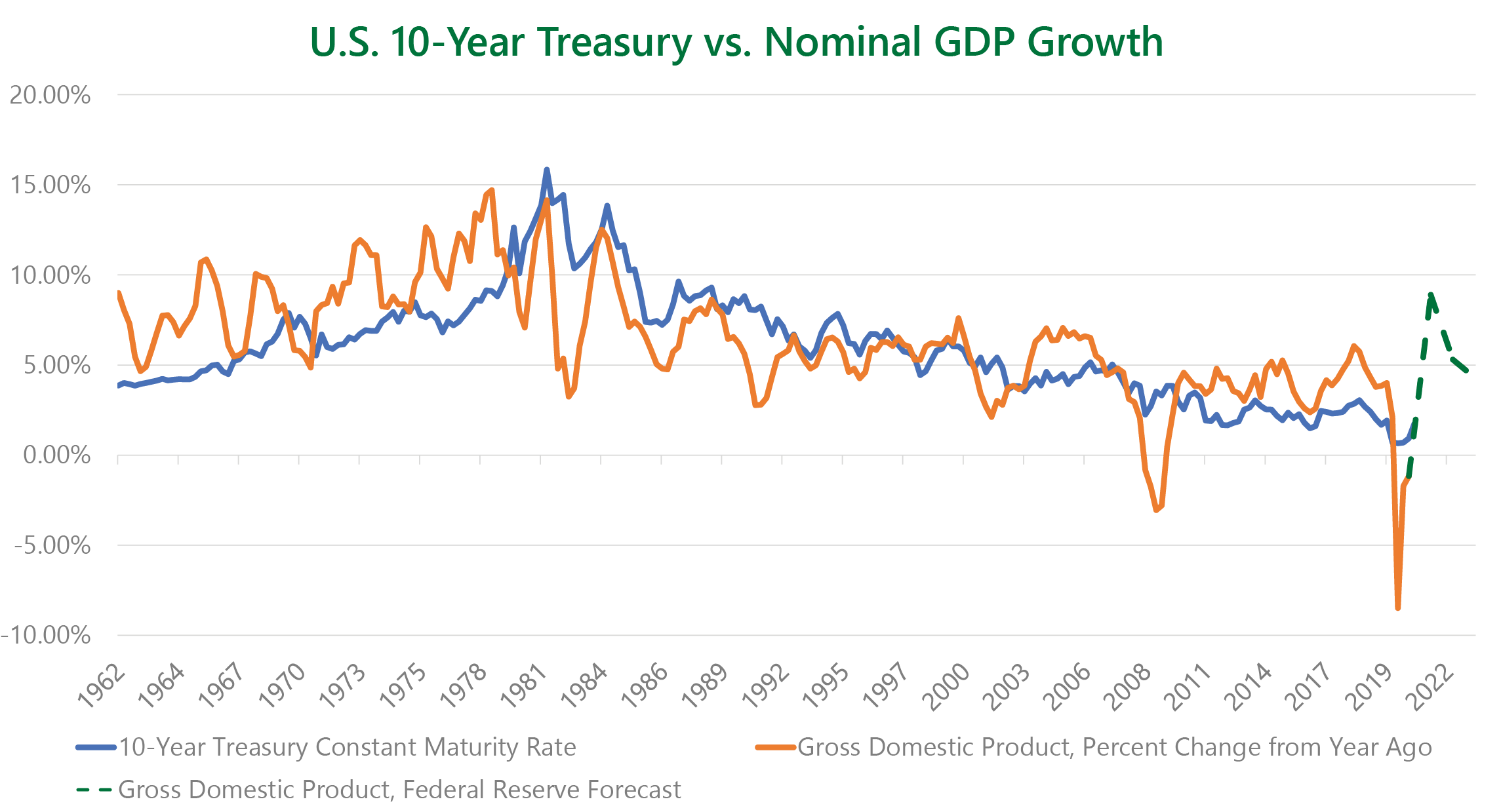

There are ample reasons to be optimistic about the direction of the economy in the near term, but unfortunately the direction of security markets is much murkier. Equity markets tend to look forward, people live in the present, and many economic indicators reflect on the past. Last year, while equity markets soared as the economy was in the clutches of Covid-19, it was common to say that the market was not representative of the economy. With the benefit of hindsight, equity markets seem prescient, but we believe the phrase is still worth repeating with additional caveats. Over the short-term, the market is not necessarily representative of the economy. The U.S. economy will likely realize its fastest real annual GDP growth rate in over 20 years in 2021. Will this supercharged growth simply lead us back to the days of 2% GDP growth or will it unleash the “animal spirits” that have been missing for so long? If the U.S. economy’s growth trajectory steepens, will interest rates rise significantly? What will this mean for inflation, the labor market, corporate profits, and equity market valuations?

Source: U.S. Federal Reserve &, Federal Reserve Bank of St. Louis. Time period for U.S. Treasury: quarterly from 3/31/62 – 3/31/21. Time period for GDP: quarterly from 3/31/62 – 12/31/20. Time period for GDP forecast: annually from 12/31/20 – 12/31/23. Federal Reserve Forecast is the Federal Open Market Committee’s (FOMC) median PCE inflation projection added to the median change in real GDP projection from the March 2021 Summary of Economic Projections.

These are incredibly difficult questions and it’s not easy to come up with answers. How these variables play out will obviously determine the direction of the markets, but perhaps more importantly they will determine the dispersion of the markets. Specifically, which sectors and securities will lead the market in the future. Broad market indices often hide much of the dispersion that is occurring among their constituents, but if we look below the surface, we see a market that is grappling with the questions posed above and many more. To illustrate this sentiment, we looked at the dispersion among the sectors of the S&P 500. During the 10 years prior to the pandemic, the maximum quarterly spread in performance between the best and worst performing sector was 26%, with an average spread of 16%. Since then, the performance spread between the best and worst sector has averaged 31%1. Put differently, the average sector dispersion since the beginning of the pandemic has been greater than the maximum dispersion in the 10 years prior. Far be it from us to predict a sustained change in market leadership, but it seems all but certain that this is a fundamentally different market environment than the one that preceded the pandemic.

Finally, we’d be remiss if we didn’t mention interest rates and inflation. U.S. interest rates almost doubled during the quarter with the 10-year U.S. Treasury yield rising from 0.93% to 1.74%. The U.S. Treasuries Index lost over 4% for the first time since 1980 and the Bloomberg Barclays Aggregate Bond Index slipped 3.4%. Inflation and interest rates are coming off such historic lows that the rise in both may have a muted effect for a while. We have quipped that “rising rates don’t matter until they do.” The competition for capital is an ever-present battle and at some point, higher yields may take capital from equities, but with equity volatility low and investor risk appetite high, we are not holding our breath quite yet.

Even though higher interest rates and inflation expectations haven’t spooked the broad market just yet, we can certainly see their effects below the surface. During recent history, large-cap growth companies have generally outperformed during periods of falling inflation expectations, while the opposite has generally been true for small-cap value companies. Relative performance of the S&P 600 Small-Cap Value Index vs the S&P 500 Large-Cap Growth Index reached its nadir in the first half of 2020 as inflation expectations fell to levels not seen since the 2008 Financial Crisis. However, inflation expectations rose significantly in the latter half of 2020 and this trend has continued into 2021. Around the same time that inflation expectations exceeded their pre-pandemic level, small-cap value’s performance began to turn around and it has handily outperformed large-cap growth since.

Source: Bloomberg & Federal Reserve Bank of St. Louis, trailing 10-years as of 3/31/21

We’ll finish by asking a question that we’ve asked many times before: Is your portfolio ready? Prior to the pandemic, U.S. large-cap equities produced stellar returns thanks in large part to high weightings to the technology, communication services, and consumer discretionary sectors. This regime was a boon to passive U.S. investors and provided little opportunity for active managers to add value. Since the pandemic, the dispersion among U.S. sectors and factors has increased markedly, providing ample opportunity for savvy active managers. Should the Covid-19 pandemic mark a turning point in general market leadership, it may continue to provide opportunity in parts of the market that have long been overlooked, as well as stress test asset allocation assumptions that have been anchored in more recent history. Given our flexibility as managers, we are excited about the opportunities that may lie ahead.

This article was contributed by Dave Haviland, Portfolio Manager and Managing Partner at Beaumont Capital Management, a participant in the ETF Strategist Channel.

For more insights like these, visit BCM’s blog at blog.investbcm.com.

Sources and Disclosures:

1Source: Bloomberg & Beaumont Capital Management (BCM), as of 3/31/21

Copyright © 2021 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Past performance is no guarantee of future results. Index performance is shown on a gross basis and an investment cannot be made directly in an index.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk.

Diversification does not ensure a profit or guarantee against a loss.

The Standard & Poor’s (S&P) 500® Index is an unmanaged index that tracks the performance of 500 widely held, large-capitalization U.S. stocks. Indices are not managed and do not incur fees or expenses. The S&P Small Cap 600® Index is an unmanaged index that tracks the performance of 600 widely held, small-capitalization U.S. stocks. The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World ex-U.S. Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the United States. The MSCI ACWI Index captures large and mid-cap representation across 23 Developed Markets and 26 Emerging Markets countries. The MSCI ACWI Index ex-U.S. captures large and mid-cap representation across 22 Developed Markets and 26 Emerging Markets countries, excluding the United States. The Bloomberg Barclay’s U.S. Aggregate Bond Index is a broad base index and is often used to represent investment grade bonds being traded in the United States.

“S&P 500®”, and “S&P Small Cap 600®” are registered trademarks of Standard & Poor’s, Inc., a division of S&P Global, Inc. MSCI® is the trademark of MSCI Inc. and/or its subsidiaries.

For Investment Professional use with clients, not for independent distribution. Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC

75 2nd Ave, Suite 700, Needham, MA 02494 (844-401-7699)