By DAN ZOLET, CFA

The Art and Science of Stock Selection

DCF – RiverFront’s Primary Stock Valuation Tool

As we digest earnings and Fed data this week, we thought it would be helpful to spend some time explaining how our equity team uses these inputs to properly position our portfolios. In our view, the goal of any valuation process is to examine current fundamentals, make some assumptions about future ones and try to assess what all that information is worth today. Our primary framework/tool we use for this is called Discounted Cash Flow analysis or DCF. In essence it is the process of making long-term forecasts of a company’s earnings/cash flows and ‘discounting’ them back to a current value, using judgment, an interest rate, math, and lots of humility.

Our hope is that using this process enables us to understand the economics of a company as it exists today, and to understand the drivers of value creation in the future. We can then assess whether the market is being reasonable in its current price it is paying for that company’s growth and use our fundamental judgement to project where we see opportunities to invest. This enables us to be multi-year owners of stocks, as long as our fundamental thesis remains in place and the market does not begin to overprice the stock. Being able to quantify this intrinsic value of a stock not only informs an investor’s security selection within a sector or industry, but also can be used with fundamental, top-down research to perform sector allocation. In this piece, we will provide an overview of DCF analysis, as well as its benefits and shortcomings.

What is DCF Analysis?

While DCF analysis sounds like the name of a math-heavy economics class many would like to skip, at its core, it is a simple, yet powerful tool. As its name suggests, DCF analysis takes future cash flows and discounts them to a current intrinsic price. Breaking this definition into two portions allows for further understanding.

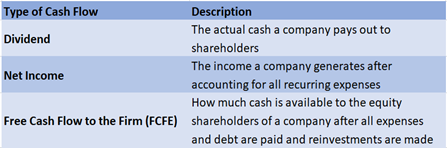

First, “cash flow” is the remaining revenue after accounting for various expenses the company incurs. The specific cash flow that is used for analysis is an individual decision but should remain consistent when comparing multiple companies. Some examples of potential cash flows for DCF analysis are:

Dividends are the most straightforward measurement, requiring the least number of assumptions and calculations, in our view. However, not every company pays dividends. At RiverFront, we prefer to use a blend of the valuation resulting from Net Income and Free Cash flow analysis as our intrinsic value. As we digest earnings data and management discussion, we align the numbers and commentary with our views of future cash flows, often combining these with industry research to adjust what we believe the potential future cash flows of the company are likely to be.

The next part of the process is using a Discount Rate to determine how valuable those cash flows are today, since they occur in the future, and are uncertain. This is critical to determine whether the investment is “worth it” – especially when compared to other investments. There are two primary inputs to how to “Discount” cash flows. The first is to look at the track record of the company and industry in question from an earnings and risk lens. The more stable a company’s earnings and the greater the visibility into the future, the more valuable those earnings are today. Similarly, the greater the perceived risk of the company regarding debt, litigation, or geopolitics, the greater that discount rate needs to be.

The second input in determining a discount rate is the opportunity cost. This involves looking at fixed income yields, since those are easily investable, as well as factoring in the level of valuation in the broad market – these ingredients help to set the standard against which our potential investment can be judged.

The Importance of The Fed

The reason the Fed is so critical to this analysis is two-fold. The first is because interest rates are a primary input to the discount rate. As the Fed raises interest rates, bonds and cash become more attractive as alternatives to equities. There is also an indirect effect to be considered. As the Fed raises the cost of corporate financing, companies will also be forced to pass on projects that they might have taken on at lower interest rates. This is why, even for stock investors, understanding Fed policy and tools is critical to evaluate equities.

How RiverFront Uses DCF Analysis

Now with a basic understanding of DCF analysis, we can discuss how we use it in our investment process. We use DCF analysis for two primary purposes: 1) Identifying current market assumptions for a company and 2) assigning an intrinsic value to an individual company.

Starting with the less involved function, using a DCF framework, we can back into the market assumptions of a company. When performing this kind of analysis, the primary inputs are Wall Street analyst expectations for revenues and historical averages for other income statement items. Using these items we can calculate, based on Wall Street’s views, what assumptions and discount rate are implied in the current price. We think “grounding” our analysis in the current price forces us to think through what the market thinks of the company’s prospects. If the market’s expectation for a company differs greatly from ours, an opportunity for further research has been identified. Additionally, if multiple companies in a sector or industry appear over or undervalued then a broader opportunity could exist – we can determine if an ETF or an individual stock is the right way to implement that view.

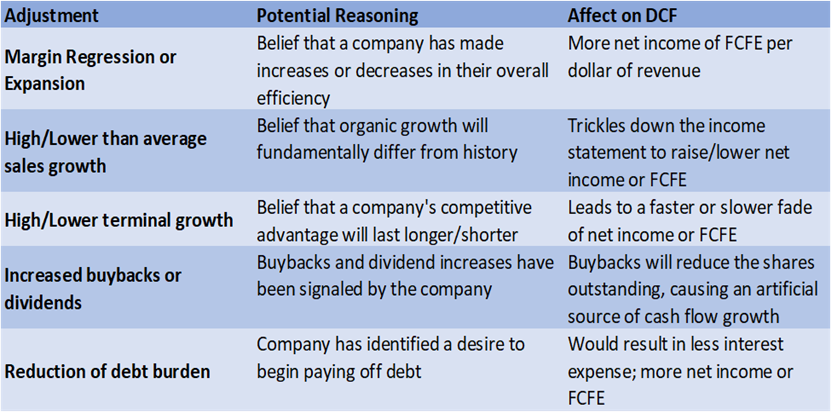

The second use of DCF analysis is assigning an intrinsic value to an individual company and involves much more investment team input. Once our equity team has done fundamental research and familiarized ourselves with the company’s guidance and the basis for analyst expectations, we can begin to create a DCF that reflects our house view on a stock. Working through the income statement, there are several adjustments an investment team member can make (see chart right). Once we have calculated an intrinsic value for a stock, we can identify what we think are potentially high upside stocks to be used as investment vehicles.

Benefits of Single Name Valuation

As discussed in the above section, the most obvious benefit of quantifying intrinsic values of stocks is it helps identify single name stocks that we believe are not being valued correctly by the market. In the most straightforward use case, an individual stock has a large amount of implied upside based on DCF analysis and is purchased within the portfolio to leverage this opportunity. However, there are some other less obvious benefits. Another more basic advantage is it can complement and flush out top-down, fundamental research. This is a two-way channel. Fundamental research can identify sectors and themes that are attractive and then DCF analysis can identify individual investments to be made within those areas. Inversely, DCF analysis could identify a sector or industry for which the market seems to assign an abnormally low or high expected growth rate.

Shortcomings of DCF Analysis

While we believe DCF analysis is a very powerful tool, it does have its shortcomings. The valuations resulting from this kind of analysis, especially for growth companies, are heavily reliant on our assumptions about earnings well into the future. As a rule of thumb, we try to be conservative in our estimates because relatively small changes can have an outsized impact. Additionally, DCF analysis requires an interest rate and credit outlook because the discount rate involves a premium over a risk-free rate. To alleviate this, our equity team leverages the views of our fixed income team. On a monthly basis, the equity team uses the fixed income team’s expectations to arrive at a single risk-free rate path to be used in all DCF analyses. Finally, when doing single name research, company specific risk is hard to quantify. The equity team mitigates this risk by peer review DCFs to make sure assumptions are conservative and consistent within and across sectors and industries, but large, unexpected events cannot be fully predicted by this comparison. This risk is also mitigated through Riverfront’s sizing discipline. Investments in individual equities are bought in quantities that we believe allow the portfolios to benefit from stock selection, while preventing a negative idiosyncratic event from overwhelming the overall goal of the portfolio.

Conclusion

The RiverFront equity team believes single-name stock selection is an important core competency. Using DCF analysis, we can identify market assumptions about a stock, as well as identify the intrinsic value of those stocks. While this is obviously helpful in instructing our individual stock investments, it has also become instrumental in augmenting our traditional, fundamental research.

For more news, information, and analysis, visit the ETF Strategist Channel.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Dividends are not guaranteed and are subject to change or elimination.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Definitions:

Discounted cash flow (DCF) refers to a valuation method that estimates the value of an investment using its expected future cash flows. DCF analysis attempts to determine the value of an investment today, based on projections of how much money that investment will generate in the future.

The Federal Reserve System (FRS) is the central bank of the United States. Often simply called the Fed, it is arguably the most powerful financial institution in the world. It was founded to provide the country with a safe, flexible, and stable monetary and financial system. The Fed has a board that is comprised of seven members. There are also 12 Federal Reserve banks with their own presidents that represent a separate district.

The term cash flow refers to the net amount of cash and cash equivalents being transferred in and out of a company. Cash received represents inflows, while money spent represents outflows.

The discount rate is the interest rate the Federal Reserve charges commercial banks and other financial institutions for short-term loans. The discount rate is applied at the Fed’s lending facility, which is called the discount window. A discount rate can also refer to the interest rate used in discounted cash flow (DCF) analysis to determine the present value of future cash flows. In this case, investors and businesses can use the discount rate for potential investments.

Free cash flow to equity is a measure of how much cash is available to the equity shareholders of a company after all expenses, reinvestment, and debt are paid. FCFE is a measure of equity capital usage.

An exchange-traded fund (ETF) is a type of pooled investment security that operates much like a mutual fund. Typically, ETFs will track a particular index, sector, commodity, or other assets, but unlike mutual funds, ETFs can be purchased or sold on a stock exchange the same way that a regular stock can.

Interest rate sensitivity is a measure of how much the price of a fixed-income asset will fluctuate as a result of changes in the interest rate environment. Securities that are more sensitive have greater price fluctuations than those with less sensitivity. This type of sensitivity must be taken into account when selecting a bond or other fixed-income instrument the investor may sell in the secondary market. Interest rate sensitivity affects buying as well as selling.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2023 RiverFront Investment Group. All Rights Reserved. ID 3020137