RiverFront places a high probability of positive market returns in 2021

2020 was a dark year by almost any standard imaginable. Riverfront’s Outlook theme for 2021 is Out of the Darkness, which references not only the renewed optimism society is placing on a vaccine for COVID-19, but also the emergence of what we believe is a new positive economic and market cycle. RiverFront places a high probability on positive market returns next year.

With the idea that ‘a picture is worth a thousand words’, this year we evolved our Outlook into a more visual format in order to make it easier to digest. In that spirit, this Weekly View, a summary of our Outlook, will also focus on the powerful story that charts can tell us about the potential for the economy and markets for 2021.

RiverFront is Optimistic about 2021

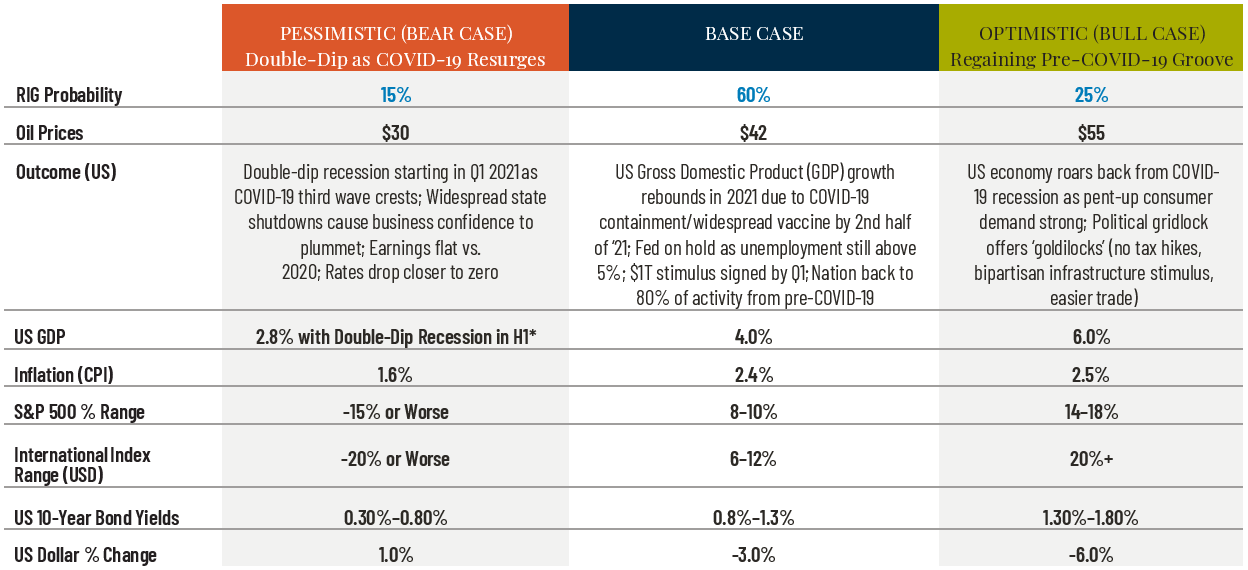

Our base case scenario sees US growth rebounding in 2021, due to widespread vaccine distribution, a Federal Reserve willing to stay accommodative, and policymakers setting aside differences long enough to come to the aid of hard-hit industries, small businesses and the unemployed. Under this scenario we believe corporate earnings will rebound strongly from 2020 levels, inflation and bond yields will gradually rise but stay range-bound, and the US dollar will likely continue its recent downtrend.

The table above depicts RiverFront’s predictions for 2021 using three scenarios (Pessimistic (Bear), Base, and Optimistic (Bull)). Our assessment of each scenario’s probability is also shown. The assessment is based on RiverFront’s Investment team’s views and opinions as of 12.15.20. Each case is hypothetical and is not based on actual investor experience. These views are subject to change and are not intended as investment recommendations. There is no representation that an investor will or is likely to achieve positive returns, avoid losses or experience returns as discussed for various market classes. See disclosures for additional definitions. *H1 = first half of a calendar year.

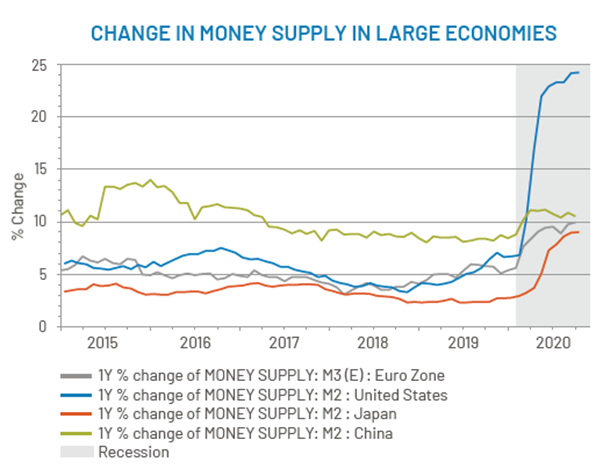

Pandemic Lockdown Forces Unprecedented Stimulus

- The US economy collapsed in Q2 of 2020, as result of the pandemic lockdown.

- This forced policymakers into the largest combined monetary and fiscal stimulus in modern history.

- Money supply is growing rapidly everywhere in the world, and particularly in the US.

- We believe this is the catalyst to usher in an economic cycle…and a very positive backdrop for the stock market

Source: Refinitiv Datastream, RiverFront; data monthly; last data release 10.01.20. Chart shown for illustrative purposes only. M2 = cash and checking deposits, savings deposits, money market securities, mutual funds, and other time deposits.

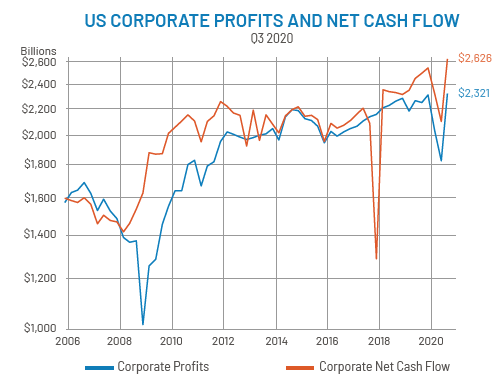

A New Economic Cycle Emerges

- While earnings on many public companies suffered, Q3 of 2020 saw record highs in broader measures of US corporate profit and net cash flow.

- Combined with strong small business and manufacturing sentiment, the data suggests to us that the US economy is in a new cyclical upturn.

- We expect the US economy to resume its pre-COVID-19 upward path by the 2nd half of 2021, but with more accommodative policy to help gird it.

Source: Refinitiv Datastream, RiverFront; data quarterly. Data as of 09.30.2020. Chart shown for illustrative purposes only. The US Corporate Profits measure—profits from current production—is the income that arises from current production, measured before income taxes, of organizations treated as corporations in the national income and product accounts (NIPAS). With several differences, this income is measured as receipts less expenses as defined in Federal tax law. Net cash flow with Industrial Value Added is equal to undistributed corporate profits with certain accounting adjustments, plus consumption of corporate fixed capital less capital transfers paid (net). It is a profits-related measure of internal funds available for investment.

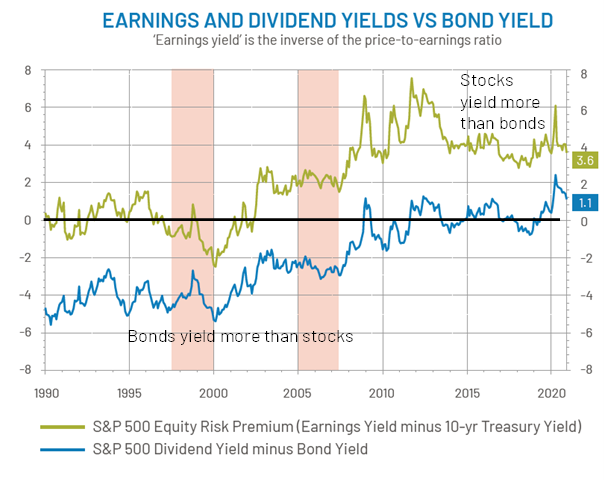

Despite Strong Run, Valuation Still Reasonable Relative to Risk-Free Rates

- The difference between the expected earnings yield on the S&P 500 on 12 month-forward earnings and the 10-year treasury is +3.6 percentage points (green line).

- Dividend yields are also greater than treasury yields (blue line), suggesting equities provide what we see as attractive income potential over ‘risk-free’ alternatives, particularly compared to the ‘peak-market’ times of the late 1990s or mid-2000s (shaded areas).

Source: Refinitiv Datastream, RiverFront; data weekly, as of 12.3.2020. Chart shown for illustrative purposes only. ‘Risk-Free’ rate is the theoretical rate of return of an investment with zero risk, which we define by using the 10-yr US Treasury Yield. Past Performance is no guarantee of future

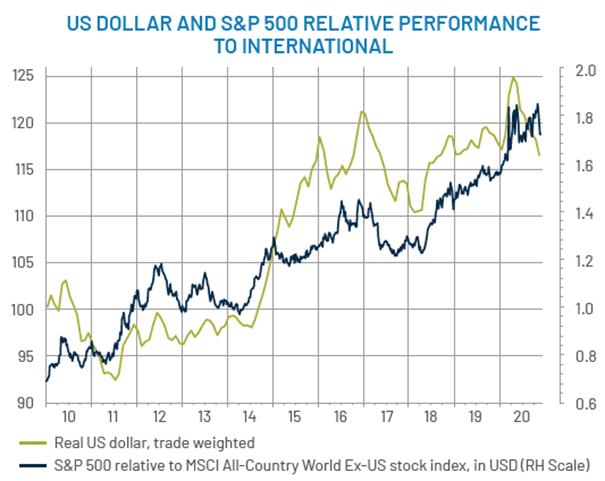

US Dollar: New Downtrend Forming?

- We expect the US dollar (USD) to remain in a weakening trend for 2021.

- There are both US-centric reasons (larger deficit and money supply), as well as international reasons (improving global growth) for this to continue.

- This is good news for US exporters, though it may create some inflation for US consumers (oil, imported goods). We also view USD weakness as generally positive for US investors in international stocks.

Source: Refinitiv Datastream, RiverFront; data monthly, as of Nov. 2020. Chart shown for illustrative purposes only. You cannot invest directly in an index. See disclosures for index definitions. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Past performance is no guarantee of future results.

Conclusion: Portfolio Positioning Reflects Our Optimism

We are optimistic on stocks despite the potential for inflation, overly optimistic investor sentiment, unsettled politics, and virus mutation currently occurring in Europe. We think these concerns will be more than offset in ’21 by the positive backdrop of unprecedented stimulus, as was the case in 2020.

In light of this view, we continue to favor stocks over bonds, and prefer a mixture of US stable earnings growers with cyclical themes. We see companies in the software and data warehousing industries as two examples of stable earnings growers. Infrastructure companies and companies servicing the US consumer are the types of companies that we anticipate benefiting from an upturn in the economic cycle. We believe international stocks remain fundamentally challenged but tactically attractive due to rebounding global growth, particularly in emerging economies, and the potential for currency tailwinds.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Gross Domestic Product (GDP) is the monetary value of all finished goods and services made within a country during a specific period. GDP provides an economic snapshot of a country, used to estimate the size of an economy and growth rate.

The Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. Changes in the CPI are used to assess price changes associated with the cost of living. The CPI is one of the most frequently used statistics for identifying periods of inflation or deflation

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

MSCI ACWI ex USA Index (International) captures large and mid cap representation across 22 of 23 developed markets (DM) countries (excluding the US) and 23 emerging markets (EM) countries.

MSCI ACWI (All Country World Index) captures all sources of equity returns in 23 developed and 23 emerging markets.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID: 1457111