Value stocks set scintillating paces in the first half of 2021. Then, some of the air came out of the value trade as 10-year Treasury yields retreated, supporting an uptick by growth stocks.

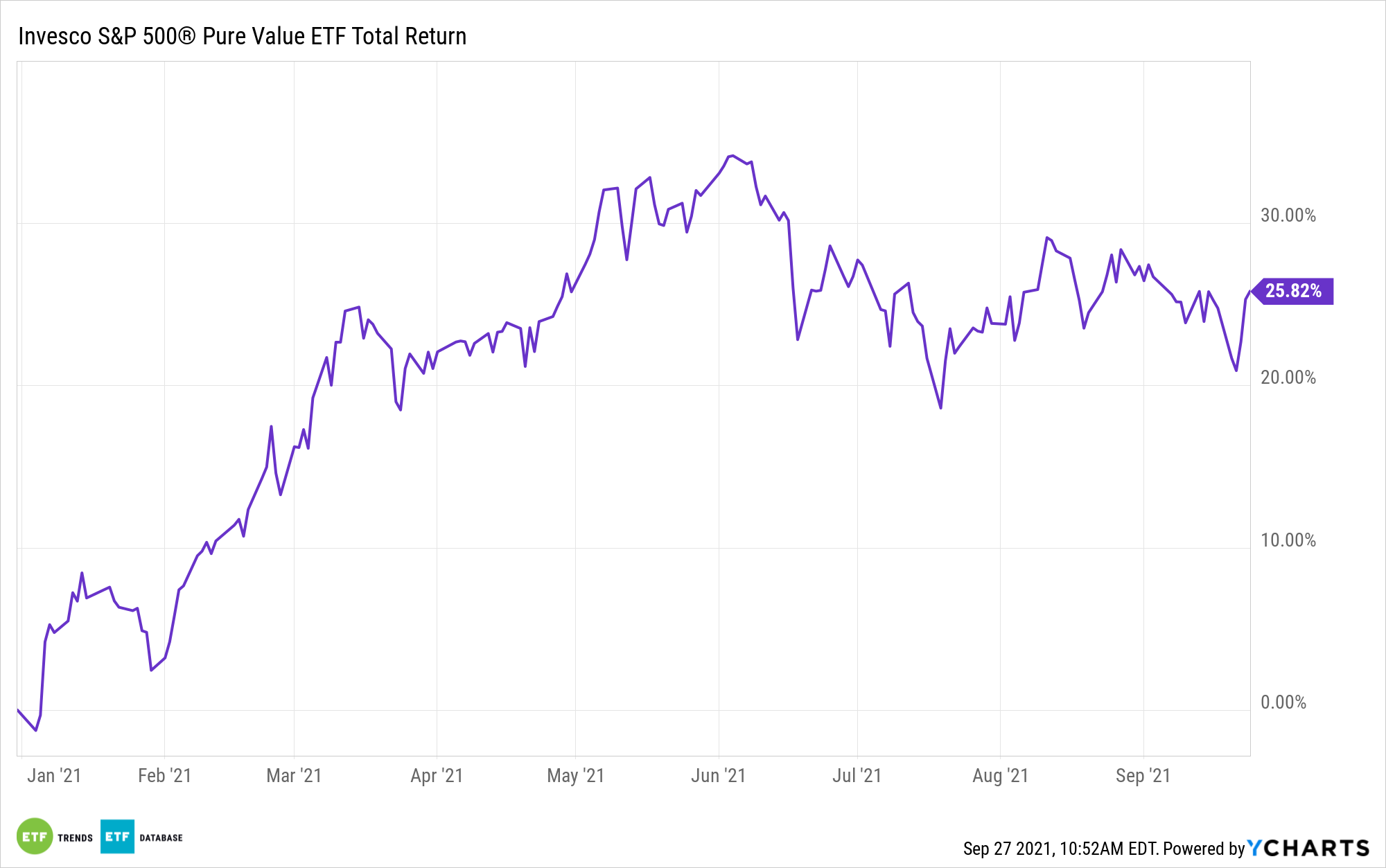

For all the talk of value names pulling back, some investors might feel as though the group is back to its laggard ways. In reality, the Invesco S&P 500 Pure Value ETF (RPV) resides just 7.39% below its 52-week high and is still higher by almost 26% year-to-date.

While RPV is trading mostly sideways over the past several months, it could be ready to rally anew, and it could have some favorable history on its side.

“History says value stocks should resume beating growth stocks from here. In the first two years of a recovery from a recession, value stocks tend to outpace growth by about 24 percentage points, according to data from Research Affiliates,” reports Jacob Sonenshine for Barron’s.

One of the primary engines of the value resurgence is the U.S. economy emerging from the effects of the coronavirus pandemic, also known as the reopening trade. Value assets, including RPV, are historically linked to economic recoveries due to deep cyclical ties. For its part, RPV allocates about 55% of its combined weight to financial services, energy, and industrial stocks — sectors that historically perform during economic recoveries.

Historical trends are nice and can be potent, but they don’t always hold true to form. Fortunately, RPV has some other tailwinds. Notably, value stocks remain inexpensive relative to growth fare.

“Value names are currently priced cheaply when compared with growth stocks. The average price-to-book ratio for the value fund is currently 28% of that for the average stock in the growth fund, according to FactSet data. Since 2011, value stocks have rarely traded much below that level and at times have hit above 50% of price-to-book ratios for growth names,” reports Barron’s.

Adding to the case for RPV is the fact that market observers, as Barron’s notes, are forecasting the same earnings growth in 2022 (9%) for growth and value stocks. Why pay up for growth when the same earnings growth is available on value? That’s a question that many investors are likely to ponder in the months ahead and that could lead them to consider RPV. And if 10-year Treasury yields climb as some market participants believe will happen, the stage could be set for RPV upside.

For more news, information, and strategy, visit the ETF Education Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.