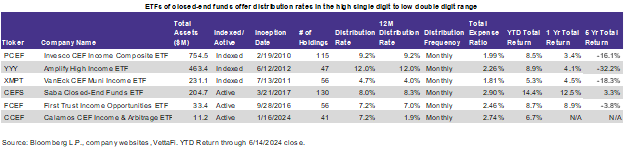

For income-seeking investors, closed-end funds (CEFs) offer relatively high distributions and the potential to buy these shares at a discount to the fund’s NAV. But these are lesser known fund structures. So many advisors and investors unfamiliar with CEFs may opt to invest in them through a familiar wrapper like ETFs.

The universe of ETFs of CEFs is small. But one ETF — the Invesco CEF Income Composite ETF (PCEF) —has significantly more assets and a longer history than the rest. This is a look at PCEF over the years and how its holdings have changed — somewhat surprisingly — along with the evolving closed-end fund landscape.

Recap: What are closed-end funds?

Most mutual funds and ETFs are open-end funds and can issue unlimited shares. Closed-end funds issue a fixed number of shares through an IPO. Post-IPO, shares can be bought on the secondary market through an exchange in the same way a stock or ETF can be bought. Like ETFs, closed-end funds are also wrappers. They can hold a portfolio of equities, fixed income, or alternatives.

While there are many similarities with ETFs, closed-end funds have a few distinct characteristics. Many CEFs aim to generate income over total return. So they typically pay higher distributions than a standard dividend ETF. Closed-end funds may also trade at wide discounts or premiums to their NAV. That may give investors an opportunity to buy ahead of distribution increases or sell ahead of distribution cuts. But because these funds are less popular, they tend to be less liquid. They may also be volatile due to the premium/discount mechanism. That makes it difficult to select individual closed-end funds.

ETFs of CEFs have diversification benefits

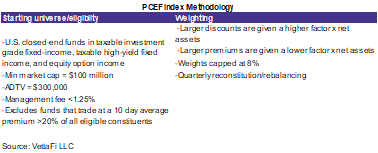

While closed-end funds lack popularity in the mainstream, ETFs of CEFs are even more niche. That’s because there only six ETFs of CEFs that focus solely on closed-end funds. Launched in February 2010, PCEF is the oldest and largest ETF of closed-end funds. It is the only fund with a primary goal of benchmarking taxable closed-end funds (i.e., mostly all funds except municipal bond funds). Many other ETFs of CEFs aim to target funds with high distributions and not necessarily provide a view of the universe. See this note for a comparison.

PCEF excludes closed-end funds with management fees greater than 1.25% (which is important since funds of funds like PCEF have an additional layer of fees). It also excludes funds that trade at a higher than average premium. Additionally, PCEF doesn’t just weigh the remaining funds by net assets, it gives a higher weight to funds that trade at wider discounts and a lower weight to funds that trade at wider premiums.

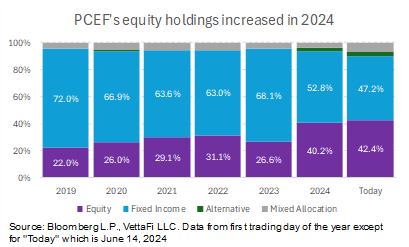

Equity opportunities have grown

When many investors think of CEFs, they think of fixed income funds that used preferred shares as leverage. But 2024 marks a departure from 2023 and previous years when equity funds were only a small portion of PCEF’s holdings.

Prior to 2024, equity was anywhere from 22% to 31% of PCEF’s weight. Fixed income was the bulk of the weight. Interestingly, from 2023 to 2024, the absolute number of equity funds in the ETF grew from only 27 to 32. The number of fixed income funds fell from 85 to 74. So the change in allocation was mostly due to weighting methodology (applying weights to funds with higher discounts) rather than the actual number of each type of fund in the ETF.

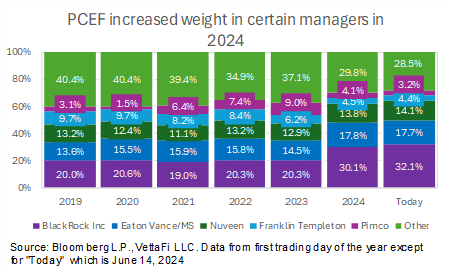

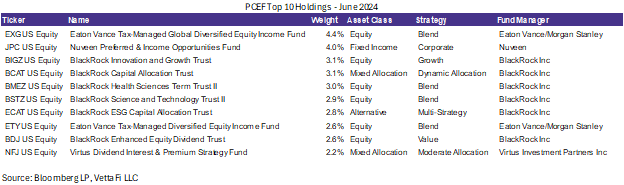

Change in top holdings reflects growth in addition to income

PCEF diversifies away some risk. But it is more concentrated among a few managers than the broader CEF universe. In 2024, PCEF had a 10%+ increase in exposure to BlackRock. And the number of BlackRock funds increased from 18 to 24 (adding BIGZ, BCAT, BMEZ, BSTZ, ECAT, and BUI). That approximately accounts for the increase of funds mentioned above. These are newer equity funds and all except BUI are in the top 10 holdings.

For instance, the BlackRock Innovation & Growth Trust (BIGZ) is currently the third largest holding in PCEF. BIGZ is a closed-end fund that focuses primarily on SMID growth companies with a large portion of tech investments. The fifth and sixth largest holdings are the BlackRock Health Sciences Trust II (BMEZ) and the BlackRock Science and Technology Trust II (BSTZ). These funds also focus on healthcare tech, science, and technology companies.

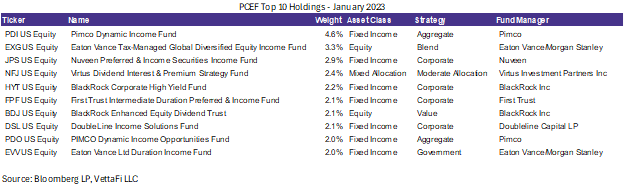

Aside from BlackRock, there was a slight increase in exposure by weight to the second and third largest managers in the fund from 2023 to 2024 — Eaton Vance and Nuveen. Allocation to “other” funds was down to less than 30%. These include other popular funds by managers like John Hancock, First Trust, Prudential Financial, Virtus, and DoubleLine. Notably, PCEF also shed its former top holding, the Pimco Dynamic Income Fund (PDI) — a global credit fund. It was 4.6% of the ETF’s weight in 2022-2023.

Bottom Line:

Indexing isn’t always perfect, but indexed products like PCEF help reduce some of the risk behind security selection while following opportunities in the broader universe in unexpected areas like healthcare tech, science, and technology.

VettaFi LLC (“VettaFi”) is the index provider for PCEF and XMPT, for which it receives an index licensing fee. However, PCEF and XMPT are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of PCEF and XMPT.

For more news, information, and strategy, visit the ETF Education Channel.