Summary

- While the Permian tends to be known for its oil output, its production mix continues to get gassier, with gas production growth outpacing that of oil.

- Midstream companies are building new pipeline takeaway capacity from the Permian.

- The Permian continues to be a hotbed for midstream M&A as well.

The Permian has long been known for its oil output. The basin in West Texas and New Mexico produces more oil than any OPEC+ member, aside from Saudi Arabia and Russia. As oil output has grown to ~6.5 million barrels per day (MMBpd), so has the volume of natural gas and natural gas liquids (NGLs) produced. Today’s note discusses expected production trends in the Permian and how midstream companies are positioning to capitalize on growing natural gas output.

The Permian is getting gassier.

Natural gas and NGLs have become a greater portion of the Permian production mix for a few reasons. First, many of the oiliest drilling locations in portions of the Permian have likely already been tapped. Additionally, oil production declines faster than natural gas. Put another way, the oil output of a well falls faster than its natural gas production. The industry broadly expects the Permian to continue becoming gassier.

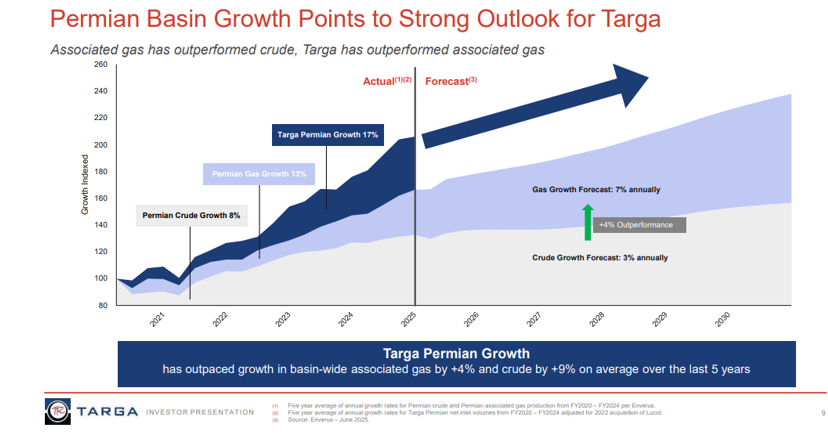

Targa Resources (TRGP) framed it well in a recent presentation. As shown below, over the last five years, oil production has grown by 8% year-over-year on average, while natural gas has grown 13% on average. (Associated gas is natural gas produced from an oil well.) All told, Permian natural gas production has increased from less than 14 billion cubic feet per day (Bcf/d) in 2019 to over 28 Bcf/d in the spring of 2025.

Source: Targa Resources August 2025 Investor Presentation

Similarly, Enterprise Products Partners (EPD) has discussed Permian gas and NGLs growing faster than crude. EPD explained in a recent presentation that each barrel of crude comes with 1.3 barrels equivalent of gas and NGLs today, up from a 1:1 ratio in 2022.

EPD forecasts oil production will grow from 6.2 MMBpd in 2024 to 7.6 MMBpd by 2030, an increase of 1.4 MMBpd (+22.6%). However, even in a scenario where Permian oil production remains flat through 2027, EPD forecasts that natural gas production would increase by 1.8 to 2.0 Bcf/d, and NGL production would also grow.

Permian gas fuels midstream growth.

For midstream, more natural gas production out of the Permian creates opportunities across the value chain. Many Permian players are adding natural gas processing plants. Before natural gas can be moved through larger pipelines or ultimately used, it must be processed to remove dirt and impurities. Processing plants also separate natural gas and NGLs.

Companies are announcing new long-haul pipeline projects from the Permian, including lines that do not end on the Gulf Coast. Last month, Energy Transfer (ET) announced the Desert Southwest Pipeline Project, which will expand its Transwestern system. The 516-mile line will have 1.5 Bcf/d of capacity, connecting the Permian to the Phoenix area. Targeted to be online by the end of 2029, the pipeline is expected to cost ~$5 billion. It could potentially be expanded pending customer interest. Privately owned Tallgrass Energy has also proposed a pipeline from the Permian to the Rockies Express System, which stretches from Colorado to Ohio.

In late August, a joint venture including ONEOK (OKE), WhiteWater, MPLX (MPLX), and Enbridge (ENB CN) announced the Eiger Express Pipeline project. The planned 450-mile pipeline will transport up to 2.5 Bcf/d of natural gas from the Permian Basin to the Gulf Coast. Backed by firm transportation agreements of 10 years or longer, the project is expected to be completed in mid-2028. Eiger Express is being developed by the same consortium of partners that recently placed the Matterhorn Express Pipeline into service, effectively creating a parallel system connecting growing associated gas production to demand centers.

Keep in mind a number of Permian natural gas pipeline projects are already under construction. Energy Transfer’s Hugh Brinson Pipeline, for instance, is expected to come online by the end of 2026, adding approximately 1.6 Bcf/d of takeaway capacity. Phase II of Hugh Brinson will boost capacity to 2.2 Bcf/d and allow for bidirectional movement. Another major project is the Blackcomb Pipeline, backed by a consortium including WhiteWater, TRGP, MPLX, and ENB. This line will transport up to 2.5 Bcf/d to the strategic Agua Dulce gas hub, a critical feeder for liquefied natural gas (LNG) export facilities. Blackcomb is also expected online in 2H26. Kinder Morgan (KMI) is expanding the Gulf Coast Express pipeline from the Permian by almost 0.6 Bcf/d with expected completion in mid-2026.

Midstream M&A continues in the Permian.

Aside from organic growth, the Permian has long been a hotbed for M&A activity. Bolt-on deals that complement existing assets tend to be particularly attractive for midstream names. Last month, MPLX announced the acquisition of Northwind Midstream, enhancing its Delaware Basin footprint and sour gas handling capabilities. EPD announced the acquisition of natural gas gathering assets from Occidental (OXY). MLP Western Midstream (WES) announced the acquisition of water gathering and processing corporation, Aris (ARIS). On the crude side, Plains (PAA/PAGP) recently announced the acquisition of an interest in EPIC Crude Holdings.

Acquisitions can complement existing assets and enhance a midstream provider’s service offering for producer customers. Gathering and processing acquisitions can also be a great way to feed more volumes to existing integrated systems, particularly in an environment where oil production growth is more moderate.

Ways to gain exposure.

Midstream MLPs and corporations will play a vital role in getting Permian natural gas out of the basin and to demand centers, including LNG facilities, data centers, and power plants. Natural gas production and demand growth creates opportunities for midstream companies to expand their fee-based services.

The Alerian MLP Infrastructure Index (AMZI) focuses on midstream MLPs, including EPD, ET, MPLX, WES, and PAA. The Alerian Midstream Energy Select Index (AMEI) includes U.S. and Canadian midstream corporations like OKE, TRGP, and ENB and is 25% weighted to MLPs. AMZI underlies the Alerian MLP ETF (AMLP), and AMEI underlies the Alerian Energy Infrastructure ETF (ENFR).

Investors with a greater appetite for commodity price exposure may consider an approach that is more focused on Permian producers compared to a broad energy index (read more). The Alerian Texas Weighted Oil & Gas Index (ATXWO) includes companies that produce oil and gas in Texas. OXY, Exxon Mobil (XOM), and ConocoPhillips (COP) are the largest constituents of ATXWO currently with weights of approximately 8%. ATXWO is the underlying index for the Texas Oil Index ETF (OILT).

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

Related Research:

Sizing Up the Next Wave of U.S. LNG Export Projects

Midstream MLPs Expand Permian Presence With M&A

Energy Transfer Announces Earnings, Arizona Pipeline

MLP/Midstream Earnings So Far: Gas, Dividends, OBBBA & More

Looking for Exposure to Oil & Gas Producers? Try Texas

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, ENFR, and OILT, for which it receives an index licensing fee. However, AMLP, ENFR, and OILT are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, ENFR, and OILT.

For more news information and analysis, visit the Energy Infrastructure Content Hub.