Summary

- Midstream/MLPs have seen strong performance this year. The Alerian MLP Infrastructure Index (AMZI) up 20.0%. Meanwhile, the Alerian Midstream Energy Select Index (AMEI) is up 28.3% on a total-return basis through the first three quarters of 2024.

- Index performance has been driven by several factors, including dividend growth, M&A activity, strong execution operationally, as well as an improved long-term outlook for US natural gas.

- Despite the strong performance recently, midstream valuations have not become expensive based on forward EV/EBITDA multiples and free cash flow yields.

Energy broadly has faced headwinds this year. This largely stems from weakness in oil and natural gas prices for much of this year. Among energy-related equities, energy infrastructure has been a bright spot in terms of performance, with broader midstream providing year-to-date returns above the S&P 500. Today’s note looks at midstream/MLP total returns by subsector, discusses some underlying trends driving performance, and examines valuations.

Midstream/MLPs: A Clear Bright Spot in a Tough Energy Tape

The energy infrastructure space has seen strong total returns in recent years with the positive momentum continuing in 2024. Midstream has been a bright spot among broader energy equities, which have struggled due to commodity price weakness and greater interest in growth sectors like technology. Energy’s weight in the S&P 500 has fallen to 3.3% as of Sept. 30, making it easy to overlook. (The energy sector has become more topical recently as geopolitical tension in the Middle East has boosted oil prices. However, the space was generally ho-hum in 2Q and 3Q).

Midstream is unique from the rest of the energy sector. Its fee-based business models provide some insulation from commodity price weakness. Midstream/MLPs transport, process, and store energy commodities including oil, natural gas, and natural gas liquids like propane. These services are often conducted for fees under long-term contracts with annual inflation adjustments. This results in stable cash flows at various commodity prices, which also support generous dividends that enhance total return. Midstream/MLP yields can become more attractive as interest rates fall, especially given strong dividend trends in this space (read more).

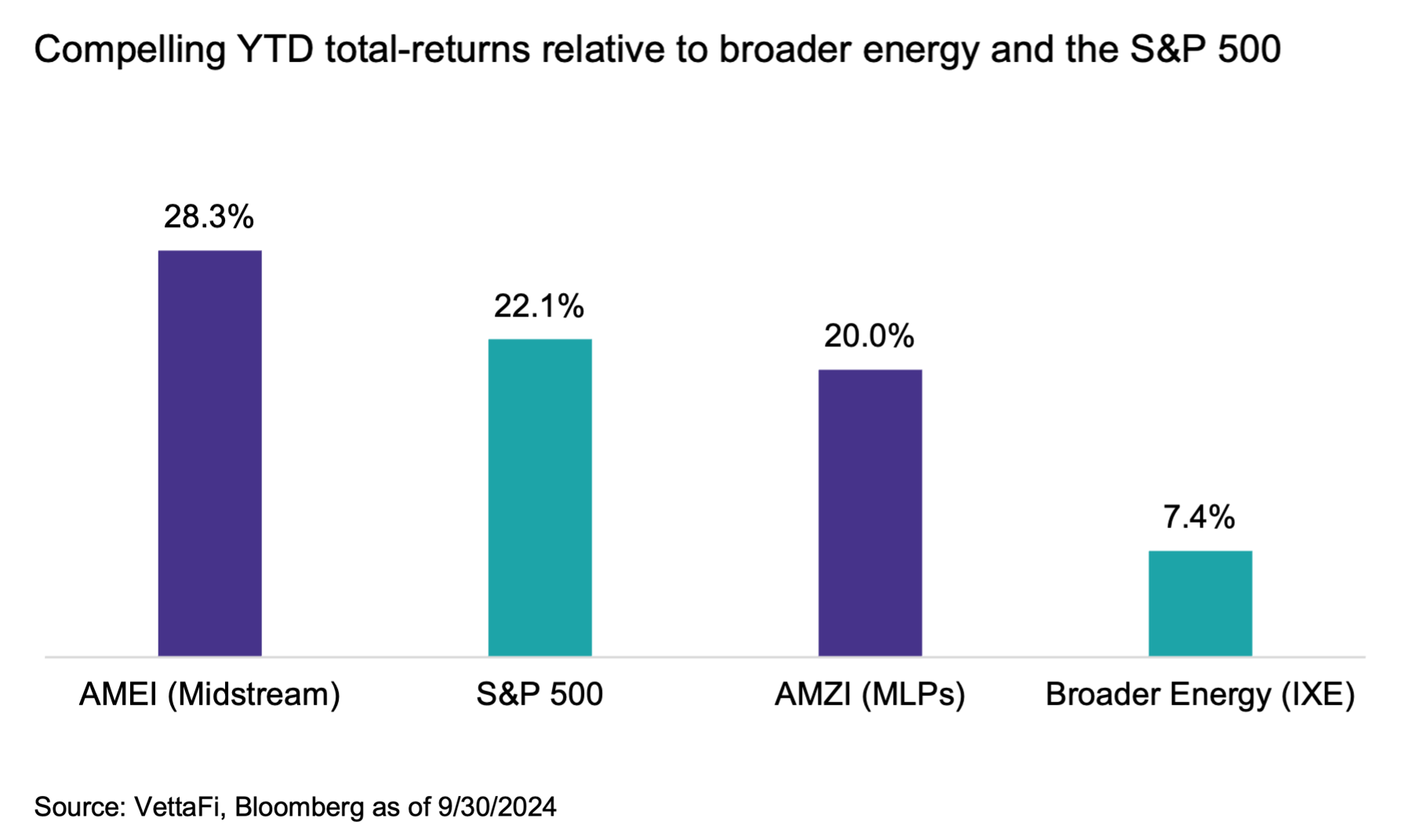

As shown in the chart below, the Alerian MLP Infrastructure Index (AMZI) is up 20.0% on a total-return basis, while the Alerian Midstream Energy Select Index (AMEI) is up 28.3% through the first three quarters of 2024. AMZI includes Master Limited Partnerships (MLPs) that earn most of their cash flow from midstream operations. AMEI is 75% US and Canadian midstream C-Corps and 25% MLPs. As of Sept. 30, AMZI was yielding 7.2%, and AMEI was yielding 5.6%. The broad Energy Select Sector Index (IXE) is up 7.4%, lagging midstream/MLPs as well as the S&P 500 which is up 22.1% year to date through Sept. 30.

Energy Infrastructure Sees Broad-Based Strength

Overall, midstream MLPs and C-Corps have seen strong performance recently that has been across multiple constituents and subsectors. Year-to-date through Sept. 30, 18 out of 27 names in AMEI have seen total returns above 20%, and only one name is down. For AMZI, five names have seen total returns above 20% so far this year. Only one name posted a negative performance. Index performance was also helped by M&A activity, with Equitrans Midstream (formerly in AMEI) acquired at a 17.9% premium and NuStar Energy (formerly in AMZI and AMEI) acquired at a 32% premium to its prior close.

Companies with notable dividend increases have also seen standout performance. Among AMEI constituents, Targa Resources (TRGP) is leading the index significantly, posting a 73.4% total return through 3Q24 having increased its May dividend by 50%. TRGP has also benefited from strong volume growth for its assets. The company raised its 2024 adjusted EBITDA guidance by 5% in August and provided a solid outlook for 2025. Similarly in AMZI, Western Midstream Partners (WES) was up 39.8% on a total-return basis through 3Q24, after increasing its May dividend by 52%.

Names with natural gas infrastructure have also seen strong performance this year. This is due to an improved long-term outlook for US natural gas demand (and production). Multiple demand drivers should provide growth opportunities for midstream. These include liquefied natural gas exports, growing demand to support power generation, including for data centers related to AI, and pipeline exports to Mexico. Coal-fired power plant retirements and industrial reshoring in the US add to the constructive demand picture.

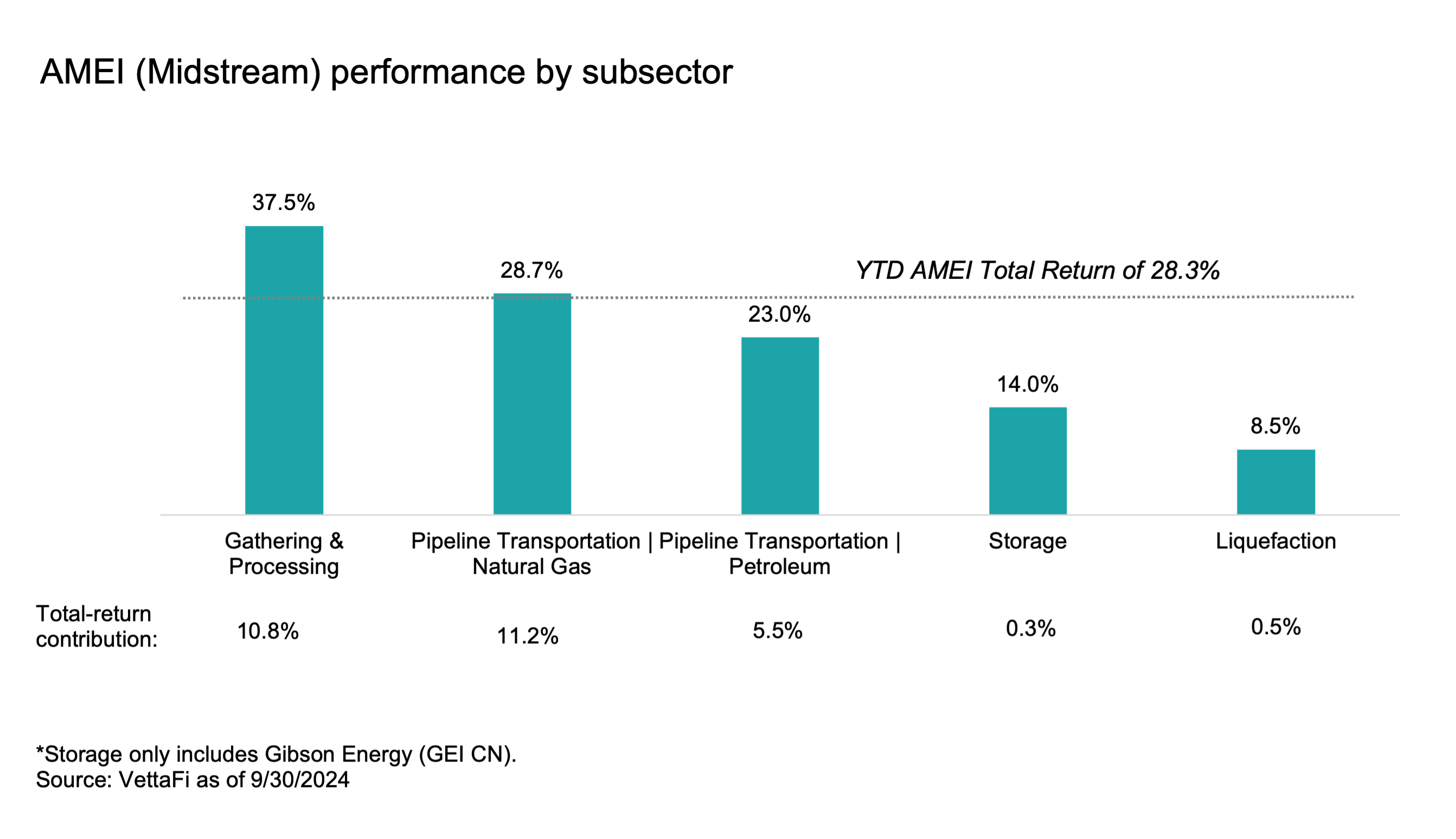

As shown in the chart below for AMEI, Gathering & Processing (G&P) companies, which collect raw natural gas from wells and process it into usable form, have seen the greatest returns this year, up 37.5% on a total-return basis. Natural gas pipeline transportation companies have also seen strong performance, up 28.7%, with names such as Kinder Morgan (KMI), Energy Transfer (ET), and DT Midstream (DTM) discussing opportunities related to natural gas demand from data centers.

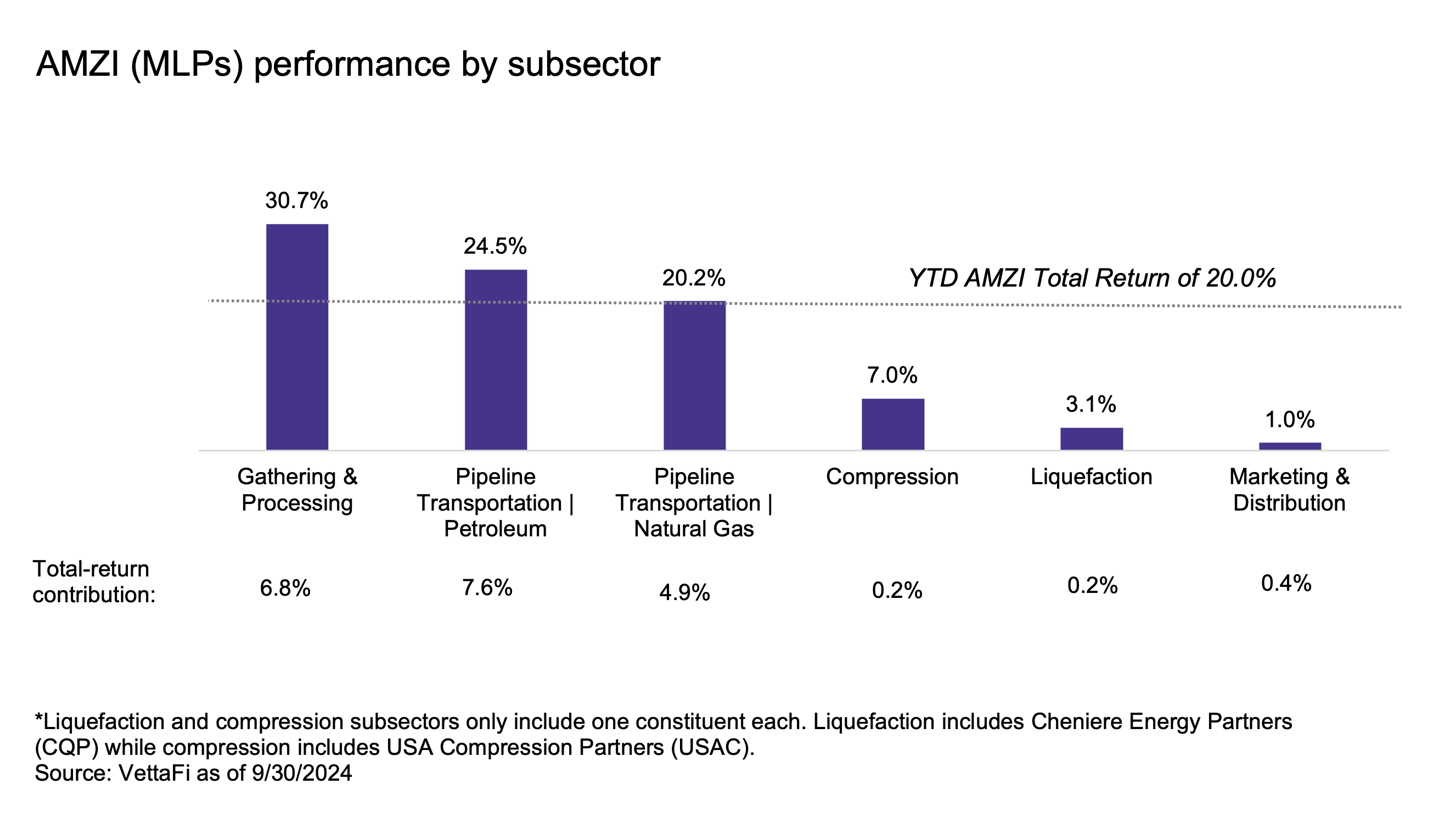

Performance trends were similar for the MLPs in AMZI, as shown in the chart below. G&P companies are leading the way with the subsector up 30.7% on a total-return basis this year. Following G&P, MLPs that predominantly operate long-haul petroleum pipelines are up 24.5% on a total-return basis, with this including the contribution from NuStar before its acquisition closed. Looking at contribution by subsector, which takes into account company weightings, petroleum pipeline operators have had the greatest contribution to AMZI’s 20.0% total return.

Despite Strong Performance, Valuations Aren’t Stretched

Given a few years of strong performance, it’s understandable for investors to wonder about valuations for this space. As of Sept. 30, AMZI had a weighted average EV/EBITDA multiple of 8.7x based on consensus estimates for 2025. This is in line with its three-year average of 8.8x and below its ten-year average of 10.0x. Meanwhile, AMEI was trading at a forward EV/EBITDA multiple of 9.8x at the end of September. Compare this to its three-year average of 9.6x and ten-year average of 11.1x. Valuations have not become stretched, particularly compared to the ten-year averages for both indexes. Of note, natural gas names have seen an uplift on expected growth beyond 2025. This is important context for metrics based on 2025 estimates.

One of the key themes in midstream since 2020 has been free cash flow generation, which has supported dividend growth and opportunistic buybacks (read more). According to Bloomberg, AMEI and AMZI have trailing 12-month free cash flow yields of 7.4% and 7.8%, respectively, as of Oct. 3, compared to just 3.0% for the S&P 500. Relative to the market, midstream/MLP FCF yields screen attractively.

Bottom Line:

Broader energy has faced a tough tape so far in 2024. However, year-to-date total returns for midstream/MLPs have been strong. Companies continue to execute well, deliver on shareholder returns, and enjoy the benefits of an improving long-term outlook for U.S. natural gas.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

2Q24 Midstream Dividend Recap: MLPs Drive Growth

AI, Natural Gas & Midstream’s Emerging Opportunities

Midstream/MLPs: AI Adds to Positive Natural Gas Outlook

LNG Tailwind for US Natural Gas Intact as Projects Progress

Midstream Connects US Gas With Growing Mexican Demand

Midstream/MLPs See Sustained Free Cash Flow

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Channel.