SUMMARY

- The natural gas liquid (NGL) value chain represents multiple touchpoints for midstream, providing fee opportunities from processing, transportation, and export terminals.

- Companies with NGL infrastructure are investing across their integrated systems as U.S. production grows.

- There are midstream companies with significant NGL infrastructure structured as corporations and MLPs.

Growth opportunities for midstream are largely concentrated around natural gas, driven by an anticipated step-change in demand over the next few years. However, investors may be less familiar with natural gas liquids (NGLs), which are another avenue for midstream growth. NGLs are a group of hydrocarbons separated out of raw natural gas and further processed into purity products. Examples include common household fuels like propane and butane, as well as ethane, which is critical for producing plastics. Today’s note looks at the NGL landscape, how it’s supporting growth for midstream companies, and how investors can gain exposure.

Understanding Midstream and NGLs

Midstream companies, typically associated with pipelines, also operate natural gas and NGL processing infrastructure. NGLs are particularly attractive for midstream because they tend to have multiple touchpoints and therefore fee opportunities. Midstream companies with integrated systems are able to collect fees along the NGL value chain. In some cases, fees can be collected from producing wells all the way to export docks.

The NGL value chain starts with raw natural gas from wells. This is transported on gathering pipelines to natural gas processing facilities. There, natural gas is cleaned and NGLs are extracted. Mixed NGLs (called Y-grade) are transported on pipelines to facilities called fractionators, which separate them into purity products. The largest NGL hub in the U.S. is Mont Belvieu, Texas, which is home to significant fractionation capacity. Nearly the entire NGL life cycle — from gathering raw natural gas to separating NGLs, transporting, and exporting them — is managed by midstream companies (read more).

Midstream Is Capitalizing on NGL Growth Opportunities

With more oil production in the Permian and natural gas production in the Marcellus, comes more NGLs. According to the Energy Information Administration, the U.S. produced around 6.9 MMBpd of NGLs in 2024. And production is expected to rise over 7% to 7.4 MMBpd by 2026.

This growth requires more natural gas processing plants and other midstream infrastructure to transport and process NGLs. For example, Enterprise Products Partners (EPD) is building the Bahia pipeline, connecting its processing facilities in the Permian to its Mont Belvieu complex. The pipeline will be capable of transporting up to 0.6 MMBpd of mixed NGLs. It is expected to be in service by 4Q25. MPLX (MPLX) is expanding the BANGL pipeline, which runs from the Permian to Sweeney on the Gulf Coast. The expansion will double the pipeline’s capacity to 250 MBpd. And there are plans to expand it to 300 MBpd in late 2026.

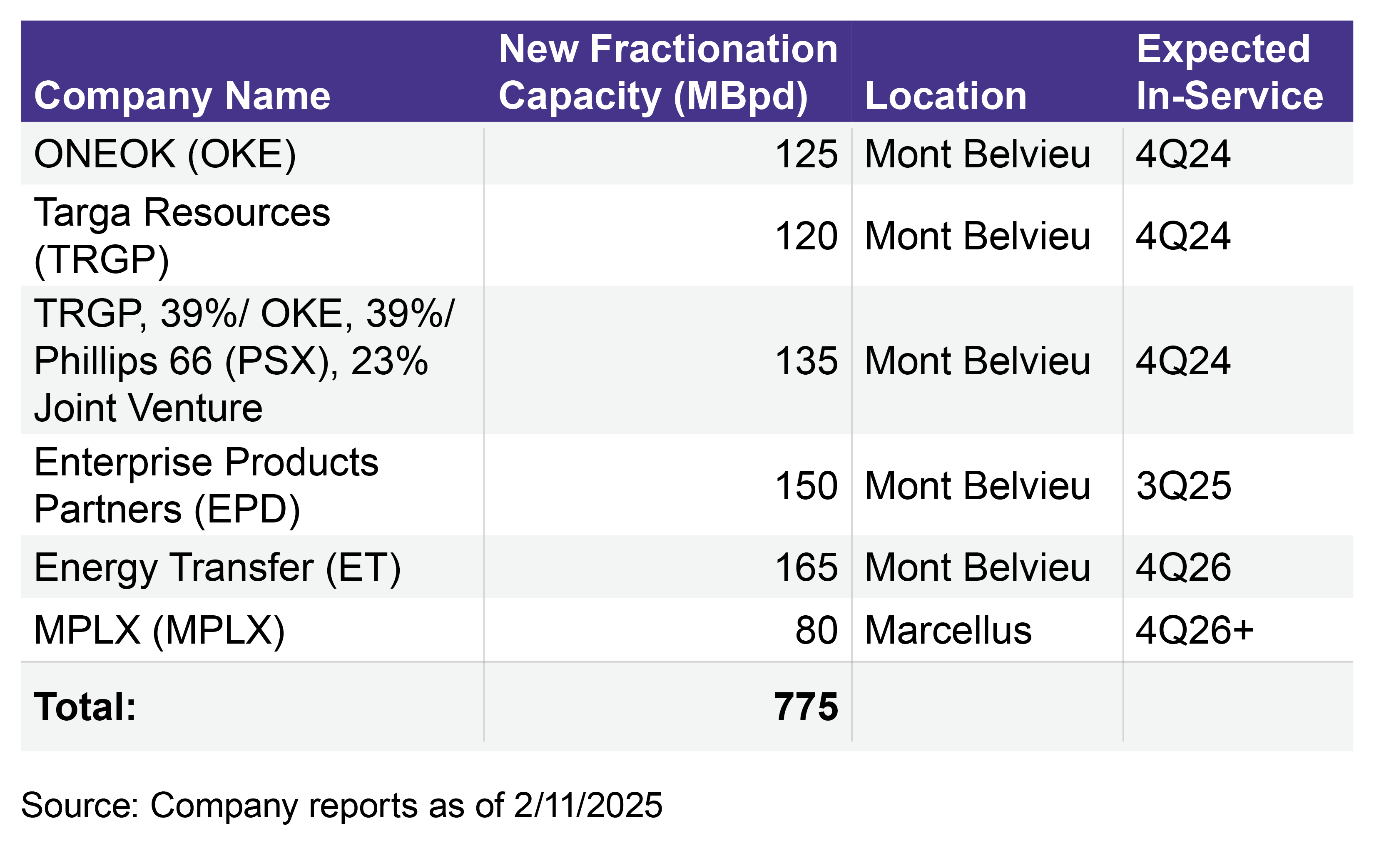

As shown in the table below, there is about 0.78 MMBpd of incremental fractionation capacity under construction or that recently came online, predominantly in Mont Belvieu. Beyond adding to its fractionation capacity in the northeast, MPLX just announced plans to build two 150 MBpd fractionators on the Gulf Coast. These are expected to start up in 2028 and 2029.

Midstream companies are also expanding export capacity to address growing international demand for NGLs. NGL export opportunities tend to focus on propane and butane, which are commonly exported together as liquefied petroleum gas (LPG). That said, ethane is expected to see the greatest growth in NGL exports to 2026. Export facilities near Houston are supplied by pipelines originating in Mont Belvieu.

Most recently, MPLX and ONEOK (OKE) agreed to form joint ventures to construct a new 0.4 MMBpd LPG export terminal near the Houston Ship Channel. The two companies are also building a pipeline from OKE’s NGL storage facility in Mont Belvieu to the new terminal. Targa Resources (TRGP) is expanding export capacity by 650,000 barrels per month at its Galena Park export terminal. The expanded export capacity is expected to be in service by the second half of 2025.

Energy Transfer (ET) and EPD are also expanding NGL export capacity on the Gulf Coast. ET is adding up to 0.25 MMBpd in capacity at its Nederland Flexport export terminal, which is expected to be in service this year. In 2024, EPD sanctioned the expansion of its export terminal on the Houston Ship Channel, with plans to add 0.3 MMBpd of LPG capacity. This is expected to be in service by 4Q26. EPD is also building a new terminal that can service both ethane and propane exports on the Neches River.

As shown in the chart below, NGL exports have been growing consistently, with 2.7 million barrels per day (MMBpd) exported in 2024 compared to just 60,000 Bpd exported in 2011. Looking ahead, NGL exports are expected to grow another 13% from 2024 levels to over 3 MMBpd in 2026. Propane accounts for the bulk of NGL exports, and the majority of propane produced in the U.S. is exported (read more). Comparatively, most of the ethane produced in the U.S. is consumed domestically, mainly as a feedstock to produce plastics and industrial products (read more).

Midstream/MLP Indexes Offer Investors Broad Exposure to NGL Growth

Midstream companies with integrated systems from producing wells all the way to export docks are able to collect fees along the NGL value chain. There are midstream companies with significant NGL infrastructure that are structured as corporations and MLPs. Among MLPs, EPD, ET, and MPLX stand out for their NGL footprints in the U.S. OKE and TRGP are corporations with sizable NGL businesses. Many more midstream names are focused on natural gas gathering and processing.

The MLPs and corporations mentioned above are all in the Alerian Midstream Energy Select Index (AMEI), which is 25% MLPs and 75% U.S. and Canadian midstream C-Corps. EPD, ET, and MPLX are among the largest constituents by weighting in the Alerian MLP Infrastructure Index (AMZI).

Bottom Line:

Ongoing U.S. energy production growth requires more infrastructure for processing, transporting, and exporting NGLs. Midstream companies with integrated NGL systems are benefiting from this growth and the associated fee opportunities.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Midstream Investing in NGLs Amid Record Exports

Propane Helps Fuel Midstream/MLP Growth

MLPs and the Fastest-Growing Hydrocarbon You’ve Not Heard Of

LNG Tailwind for US Natural Gas Intact as Projects Progress

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.

For more news information and analysis, visit the Energy Infrastructure Channel.